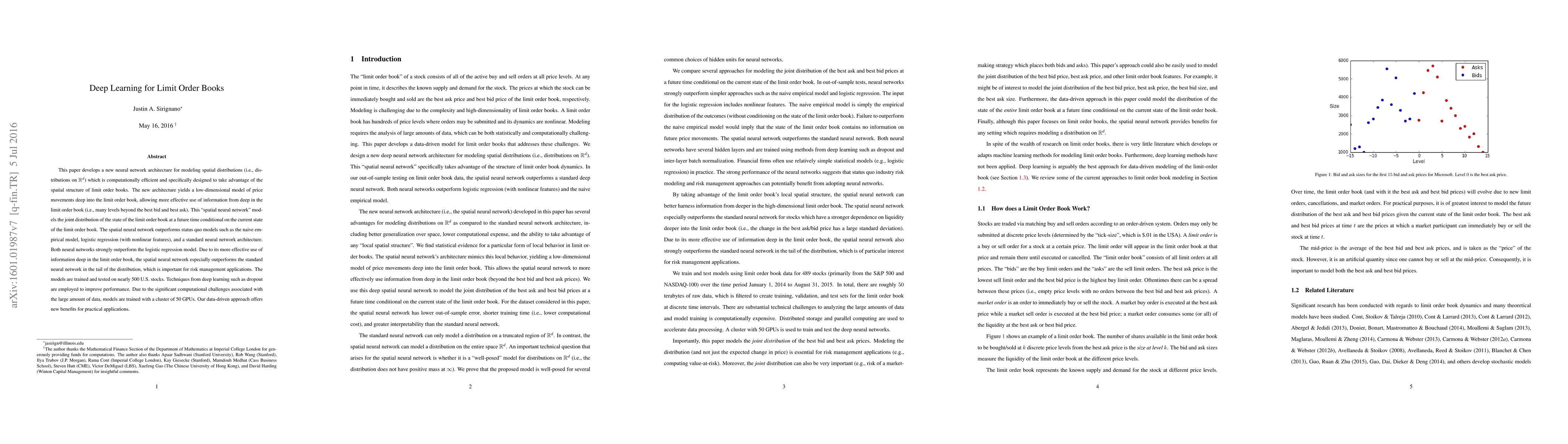

This paper develops a new neural network architecture for modeling spatial

distributions (i.e., distributions on R^d) which is computationally efficient

and specifically designed to take advantage of the spatial structure of limit

order books. The new architecture yields a low-dimensional model of price

movements deep into the limit order book, allowing more effective use of

information from deep in the limit order book (i.e., many levels beyond the

best bid and best ask). This "spatial neural network" models the joint

distribution of the state of the limit order book at a future time conditional

on the current state of the limit order book. The spatial neural network

outperforms other models such as the naive empirical model, logistic regression

(with nonlinear features), and a standard neural network architecture. Both

neural networks strongly outperform the logistic regression model. Due to its

more effective use of information deep in the limit order book, the spatial

neural network especially outperforms the standard neural network in the tail

of the distribution, which is important for risk management applications. The

models are trained and tested on nearly 500 stocks. Techniques from deep

learning such as dropout are employed to improve performance. Due to the

significant computational challenges associated with the large amount of data,

models are trained with a cluster of 50 GPUs.

Discussion 0