Publication

Metrics

AI Quick Summary

This paper presents a novel deep learning model using causal convolutions and masked self-attention for predicting price movements from limit order books, outperforming traditional methods like CNN and LSTM on the FI-2010 dataset.

Paper Preview

Abstract

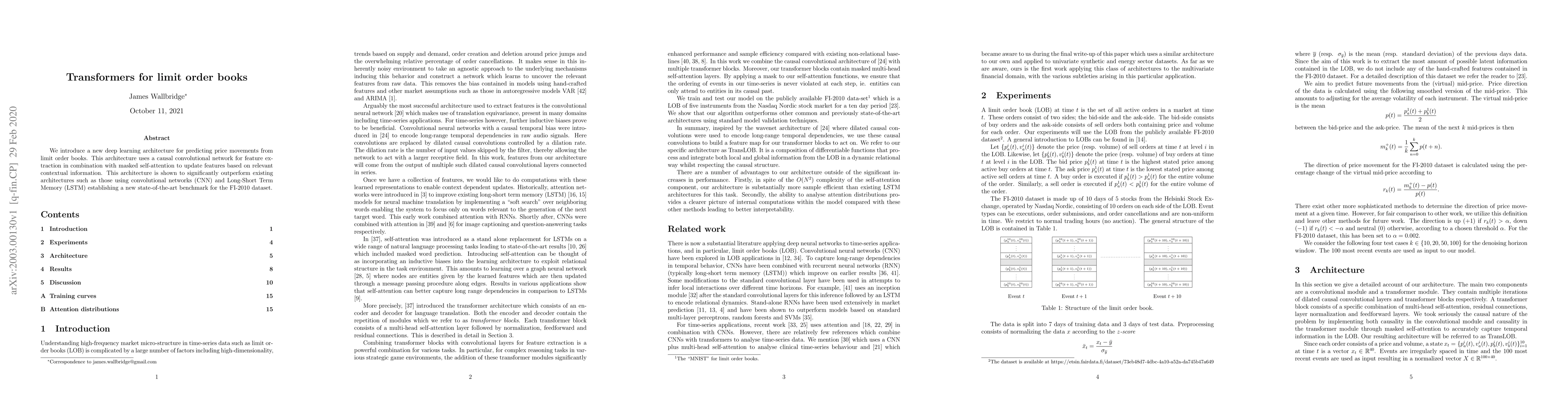

We introduce a new deep learning architecture for predicting price movements from limit order books. This architecture uses a causal convolutional network for feature extraction in combination with masked self-attention to update features based on relevant contextual information. This architecture is shown to significantly outperform existing architectures such as those using convolutional networks (CNN) and Long-Short Term Memory (LSTM) establishing a new state-of-the-art benchmark for the FI-2010 dataset.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0