Deep Stock Trading: A Hierarchical Reinforcement Learning Framework for Portfolio Optimization and Order Execution

Publication

Metrics

AI Quick Summary

This paper proposes a hierarchical reinforcement learning framework (HRPM) for portfolio optimization and order execution, addressing the issue of price slippage in trading costs. The system decomposes trading into high-level portfolio management and low-level trade execution policies, achieving significant improvement over state-of-the-art methods in U.S. and China markets.

Paper Preview

Abstract

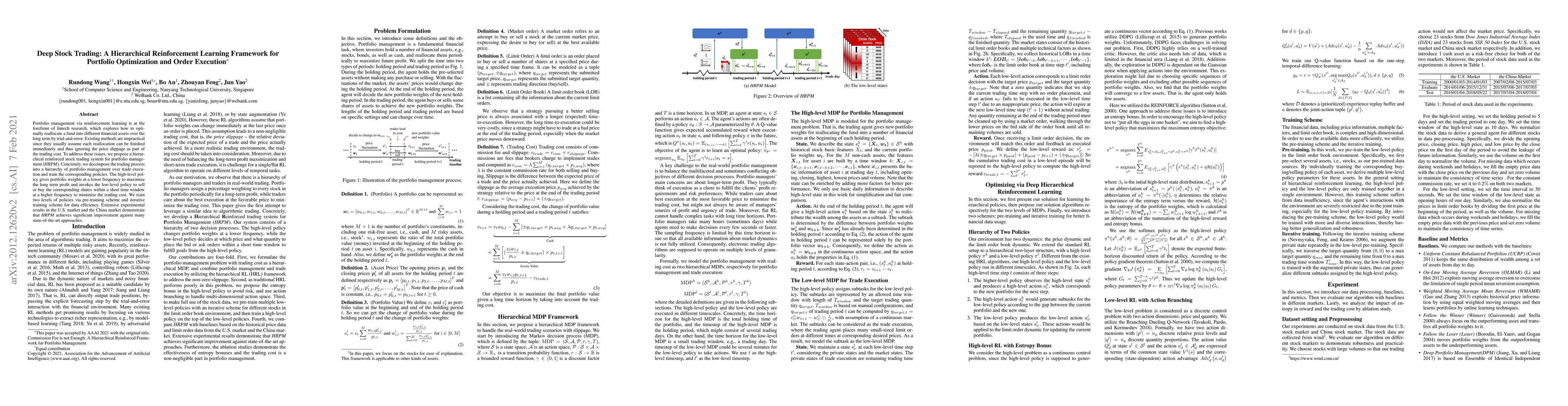

Portfolio management via reinforcement learning is at the forefront of fintech research, which explores how to optimally reallocate a fund into different financial assets over the long term by trial-and-error. Existing methods are impractical since they usually assume each reallocation can be finished immediately and thus ignoring the price slippage as part of the trading cost. To address these issues, we propose a hierarchical reinforced stock trading system for portfolio management (HRPM). Concretely, we decompose the trading process into a hierarchy of portfolio management over trade execution and train the corresponding policies. The high-level policy gives portfolio weights at a lower frequency to maximize the long term profit and invokes the low-level policy to sell or buy the corresponding shares within a short time window at a higher frequency to minimize the trading cost. We train two levels of policies via pre-training scheme and iterative training scheme for data efficiency. Extensive experimental results in the U.S. market and the China market demonstrate that HRPM achieves significant improvement against many state-of-the-art approaches.

AI Key Findings — Failed

Key findings generation failed. Failed to start generation process

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0