Publication

Metrics

AI Quick Summary

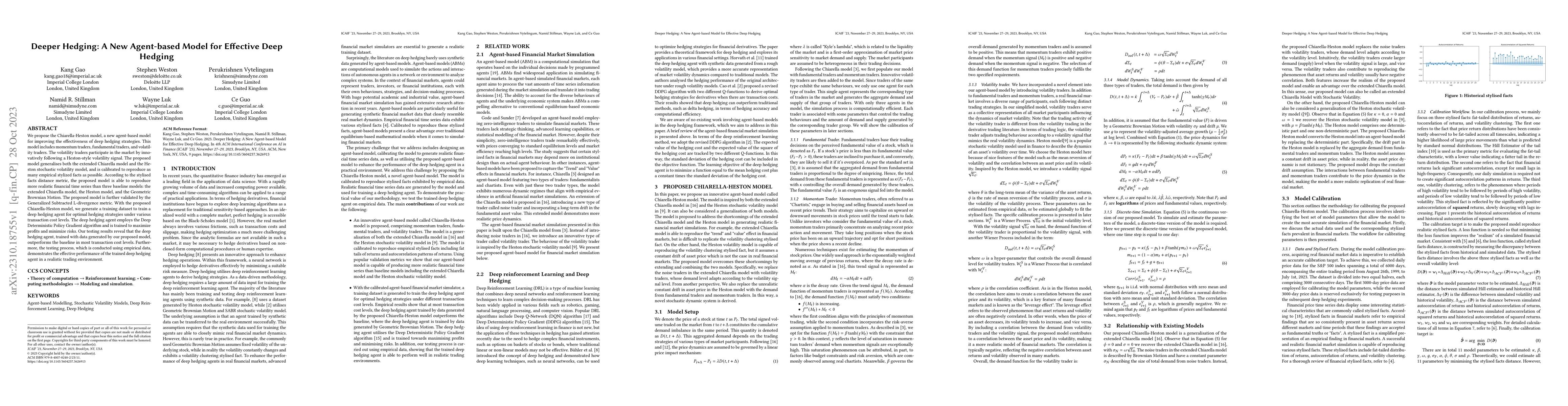

The paper introduces the Chiarella-Heston model, an agent-based framework that enhances deep hedging strategies by incorporating momentum, fundamental, and volatility traders. The model outperforms baseline models in reproducing financial time series and is used to train a deep hedging agent that effectively maximizes profits and minimizes risks in various transaction cost scenarios.

Paper Preview

Abstract

We propose the Chiarella-Heston model, a new agent-based model for improving the effectiveness of deep hedging strategies. This model includes momentum traders, fundamental traders, and volatility traders. The volatility traders participate in the market by innovatively following a Heston-style volatility signal. The proposed model generalises both the extended Chiarella model and the Heston stochastic volatility model, and is calibrated to reproduce as many empirical stylized facts as possible. According to the stylised facts distance metric, the proposed model is able to reproduce more realistic financial time series than three baseline models: the extended Chiarella model, the Heston model, and the Geometric Brownian Motion. The proposed model is further validated by the Generalized Subtracted L-divergence metric. With the proposed Chiarella-Heston model, we generate a training dataset to train a deep hedging agent for optimal hedging strategies under various transaction cost levels. The deep hedging agent employs the Deep Deterministic Policy Gradient algorithm and is trained to maximize profits and minimize risks. Our testing results reveal that the deep hedging agent, trained with data generated by our proposed model, outperforms the baseline in most transaction cost levels. Furthermore, the testing process, which is conducted using empirical data, demonstrates the effective performance of the trained deep hedging agent in a realistic trading environment.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0