Perukrishnen Vytelingum

5 papers on arXiv

Academic Profile

Statistics

Papers on arXiv

Deep Calibration of Market Simulations using Neural Density Estimators and Embedding Networks

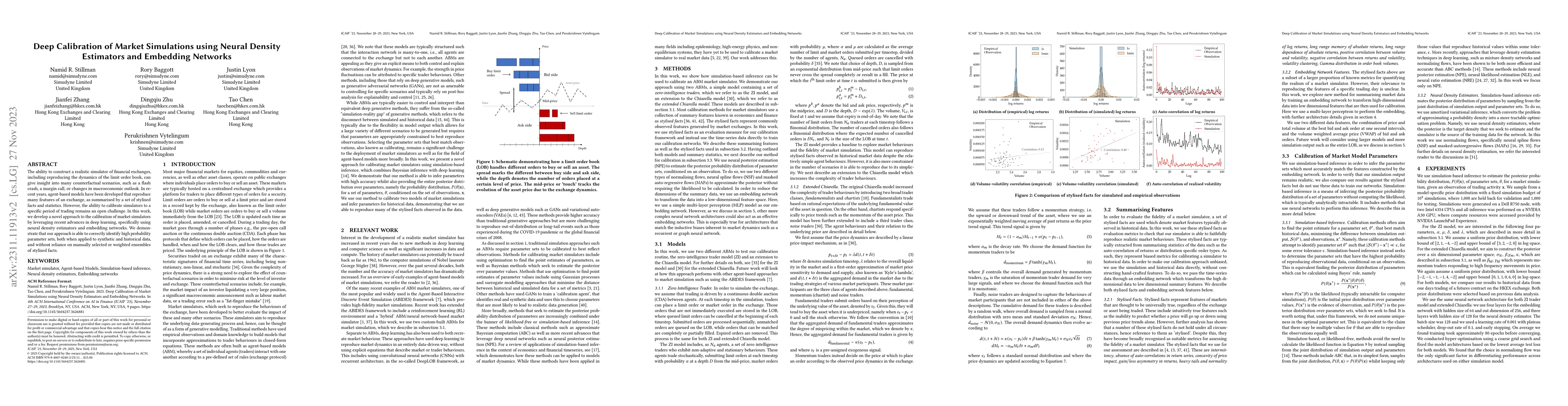

The ability to construct a realistic simulator of financial exchanges, including reproducing the dynamics of the limit order book, can give insight into many counterfactual scenarios, such as a flas...

Deeper Hedging: A New Agent-based Model for Effective Deep Hedging

We propose the Chiarella-Heston model, a new agent-based model for improving the effectiveness of deep hedging strategies. This model includes momentum traders, fundamental traders, and volatility t...

Understanding intra-day price formation process by agent-based financial market simulation: calibrating the extended chiarella model

This article presents XGB-Chiarella, a powerful new approach for deploying agent-based models to generate realistic intra-day artificial financial price data. This approach is based on agent-based m...

High-frequency financial market simulation and flash crash scenarios analysis: an agent-based modelling approach

This paper describes simulations and analysis of flash crash scenarios in an agent-based modelling framework. We design, implement, and assess a novel high-frequency agent-based financial market sim...

Agent-based Liquidity Risk Modelling for Financial Markets

In this paper, we describe a novel agent-based approach for modelling the transaction cost of buying or selling an asset in financial markets, e.g., to liquidate a large position as a result of a marg...