Machine learning models have demonstrated remarkable efficacy and efficiency

in a wide range of stock forecasting tasks. However, the inherent challenges of

data scarcity, including low signal-to-noise ratio (SNR) and data homogeneity,

pose significant obstacles to accurate forecasting. To address this issue, we

propose a novel approach that utilizes artificial intelligence-generated

samples (AIGS) to enhance the training procedures. In our work, we introduce

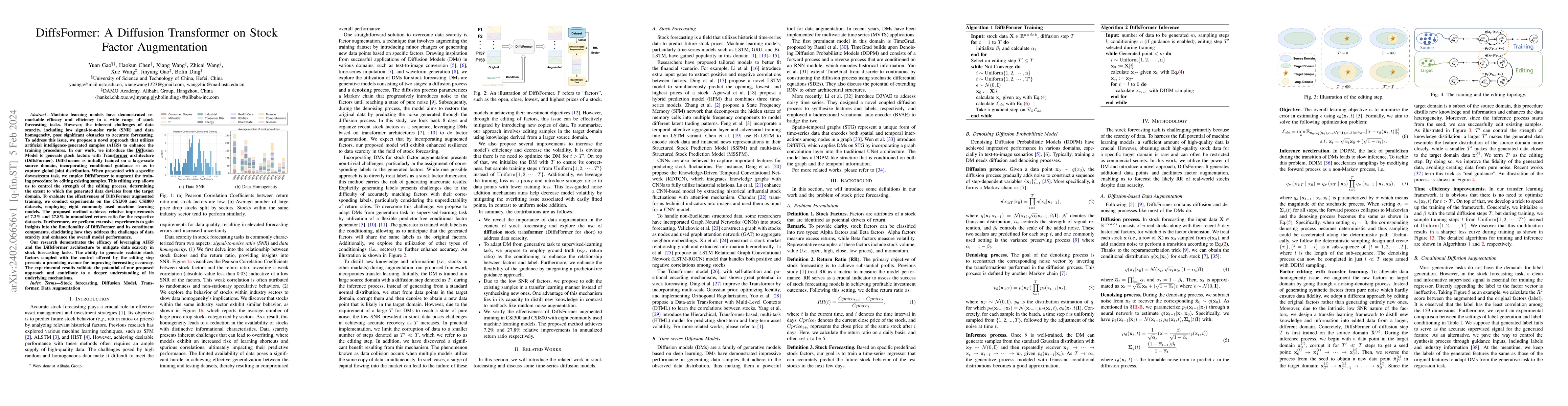

the Diffusion Model to generate stock factors with Transformer architecture

(DiffsFormer). DiffsFormer is initially trained on a large-scale source domain,

incorporating conditional guidance so as to capture global joint distribution.

When presented with a specific downstream task, we employ DiffsFormer to

augment the training procedure by editing existing samples. This editing step

allows us to control the strength of the editing process, determining the

extent to which the generated data deviates from the target domain. To evaluate

the effectiveness of DiffsFormer augmented training, we conduct experiments on

the CSI300 and CSI800 datasets, employing eight commonly used machine learning

models. The proposed method achieves relative improvements of 7.2% and 27.8% in

annualized return ratio for the respective datasets. Furthermore, we perform

extensive experiments to gain insights into the functionality of DiffsFormer

and its constituent components, elucidating how they address the challenges of

data scarcity and enhance the overall model performance. Our research

demonstrates the efficacy of leveraging AIGS and the DiffsFormer architecture

to mitigate data scarcity in stock forecasting tasks.

Discussion 0