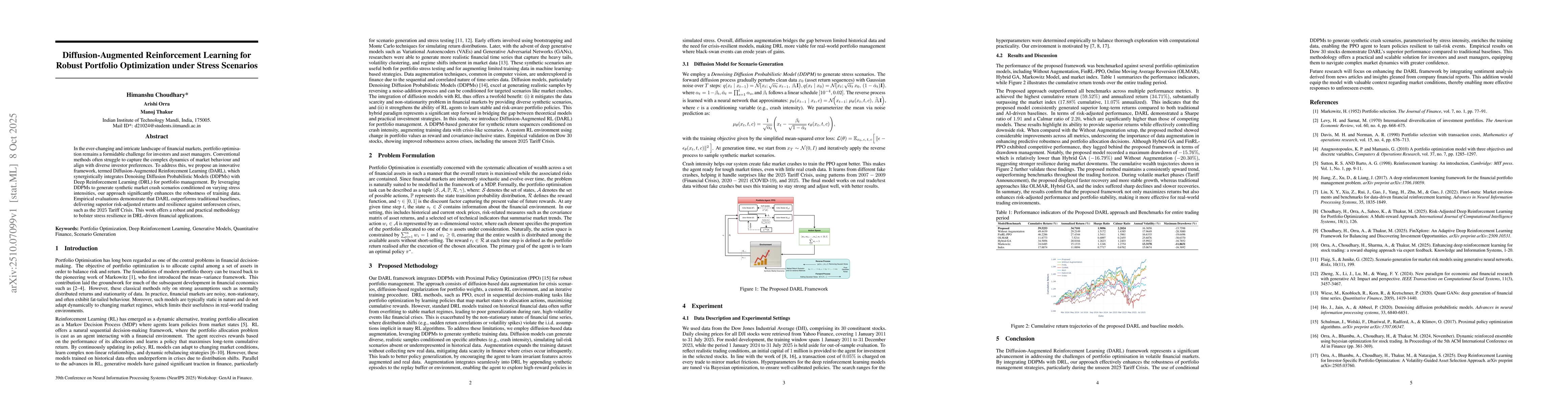

In the ever-changing and intricate landscape of financial markets, portfolio

optimisation remains a formidable challenge for investors and asset managers.

Conventional methods often struggle to capture the complex dynamics of market

behaviour and align with diverse investor preferences. To address this, we

propose an innovative framework, termed Diffusion-Augmented Reinforcement

Learning (DARL), which synergistically integrates Denoising Diffusion

Probabilistic Models (DDPMs) with Deep Reinforcement Learning (DRL) for

portfolio management. By leveraging DDPMs to generate synthetic market crash

scenarios conditioned on varying stress intensities, our approach significantly

enhances the robustness of training data. Empirical evaluations demonstrate

that DARL outperforms traditional baselines, delivering superior risk-adjusted

returns and resilience against unforeseen crises, such as the 2025 Tariff

Crisis. This work offers a robust and practical methodology to bolster stress

resilience in DRL-driven financial applications.

Discussion 0