01

MethodologyHow they did it

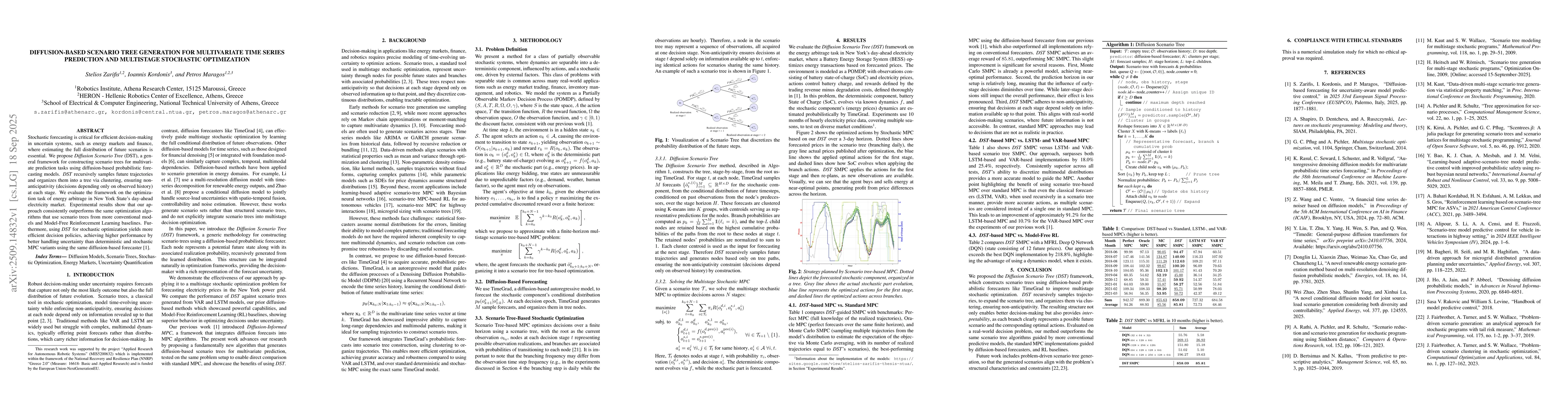

The research proposes the Diffusion Scenario Tree (DST) framework, which combines diffusion-based probabilistic forecasting models (like TimeGrad) with scenario tree generation for multivariate time series prediction. It recursively samples future trajectories using diffusion models and clusters them into scenario tree nodes, ensuring non-anticipativity by organizing forecasts into a tree structure for multistage stochastic optimization.

Discussion 0