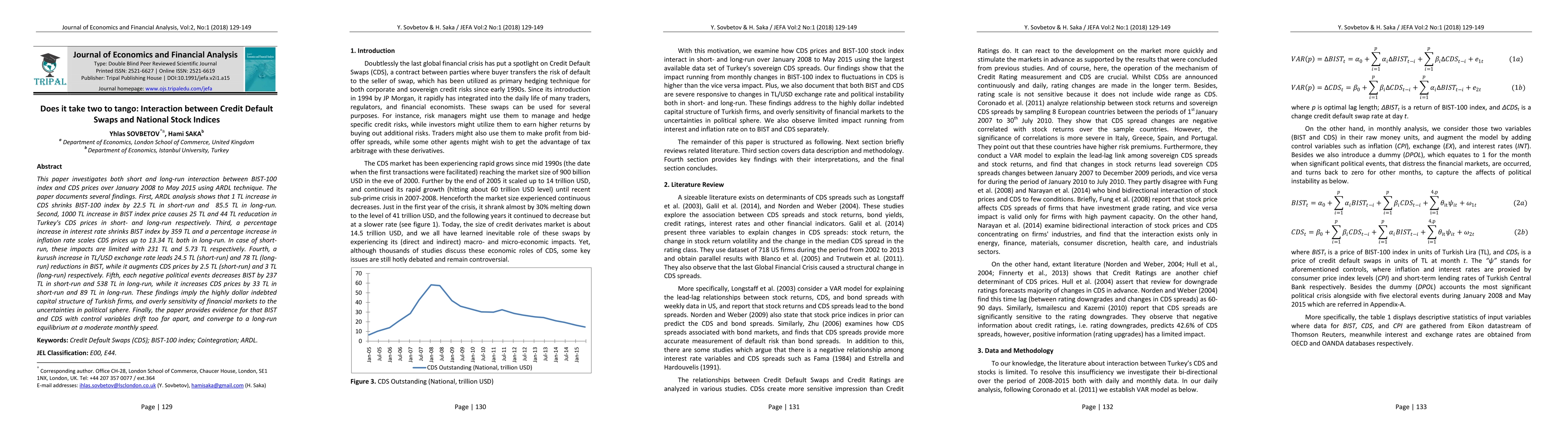

Does it take two to tango: Interaction between Credit Default Swaps and National Stock Indices

Publication

Metrics

Paper Preview

Abstract

This paper investigates both short and long-run interaction between BIST-100 index and CDS prices over January 2008 to May 2015 using ARDL technique. The paper documents several findings. First, ARDL analysis shows that 1 TL increase in CDS shrinks BIST-100 index by 22.5 TL in short-run and 85.5 TL in long-run. Second, 1000 TL increase in BIST index price causes 25 TL and 44 TL reducation in Turkey's CDS prices in short- and long-run respectively. Third, a percentage increase in interest rate shrinks BIST index by 359 TL and a percentage increase in inflation rate scales CDS prices up to 13.34 TL both in long-run. In case of short-run, these impacts are limited with 231 TL and 5.73 TL respectively. Fourth, a kurush increase in TL/USD exchange rate leads 24.5 TL (short-run) and 78 TL (long-run) reductions in BIST, while it augments CDS prices by 2.5 TL (short-run) and 3 TL (long-run) respectively. Fifth, each negative political events decreases BIST by 237 TL in short-run and 538 TL in long-run, while it increases CDS prices by 33 TL in short-run and 89 TL in long-run. These findings imply the highly dollar indebted capital structure of Turkish firms, and overly sensitivity of financial markets to the uncertainties in political sphere. Finally, the paper provides evidence for that BIST and CDS with control variables drift too far apart, and converge to a long-run equilibrium at a moderate monthly speed.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0