Publication

Metrics

AI Quick Summary

This paper introduces the Dynamic Graph Representation with Contrastive Learning (DGRCL) framework to improve stock market prediction by integrating dynamic temporal changes and static relational structures of stocks. The framework's Embedding Enhancement and Contrastive Constrained Training modules enable comprehensive market dynamic understanding, significantly outperforming existing methods on NASDAQ and NYSE datasets.

Paper Preview

Abstract

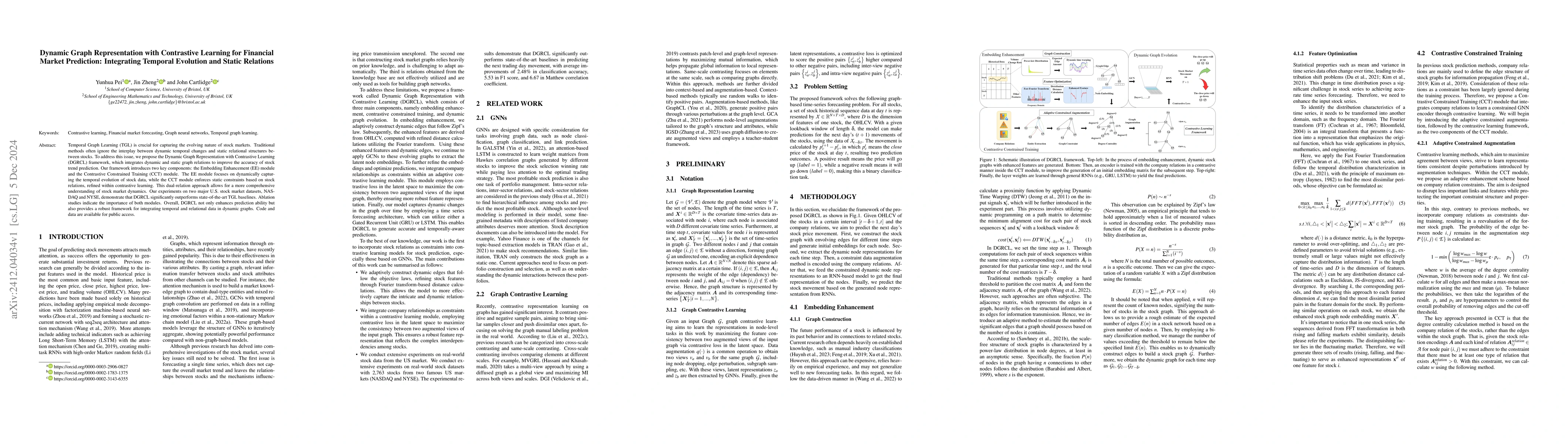

Temporal Graph Learning (TGL) is crucial for capturing the evolving nature of stock markets. Traditional methods often ignore the interplay between dynamic temporal changes and static relational structures between stocks. To address this issue, we propose the Dynamic Graph Representation with Contrastive Learning (DGRCL) framework, which integrates dynamic and static graph relations to improve the accuracy of stock trend prediction. Our framework introduces two key components: the Embedding Enhancement (EE) module and the Contrastive Constrained Training (CCT) module. The EE module focuses on dynamically capturing the temporal evolution of stock data, while the CCT module enforces static constraints based on stock relations, refined within contrastive learning. This dual-relation approach allows for a more comprehensive understanding of stock market dynamics. Our experiments on two major U.S. stock market datasets, NASDAQ and NYSE, demonstrate that DGRCL significantly outperforms state-of-the-art TGL baselines. Ablation studies indicate the importance of both modules. Overall, DGRCL not only enhances prediction ability but also provides a robust framework for integrating temporal and relational data in dynamic graphs. Code and data are available for public access.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Paper Details

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0