Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present a replication and correction of a recent article (Ramirez, P., Reade, J.J., Singleton, C., Betting on a buzz: Mispricing and inefficiency in online sportsbooks, International Journal of For...

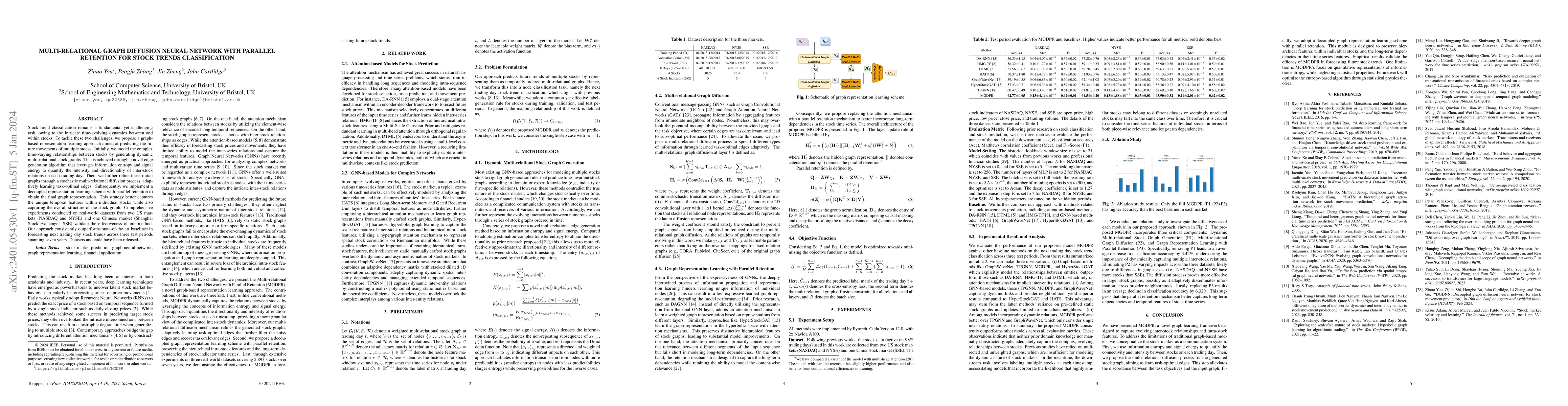

Stock trend classification remains a fundamental yet challenging task, owing to the intricate time-evolving dynamics between and within stocks. To tackle these two challenges, we propose a graph-bas...

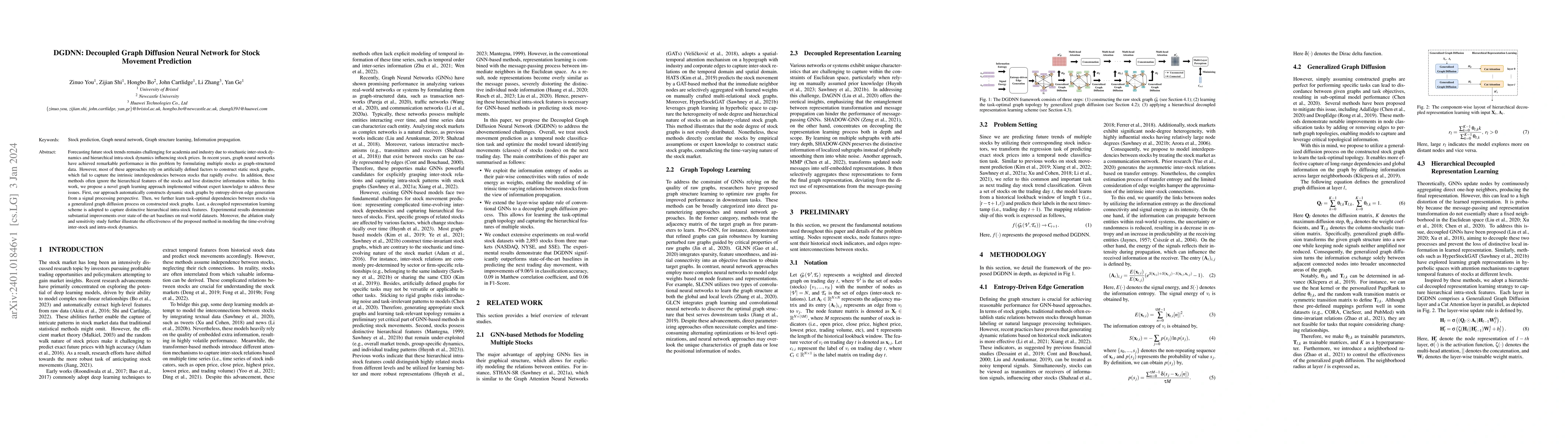

Forecasting future stock trends remains challenging for academia and industry due to stochastic inter-stock dynamics and hierarchical intra-stock dynamics influencing stock prices. In recent years, ...

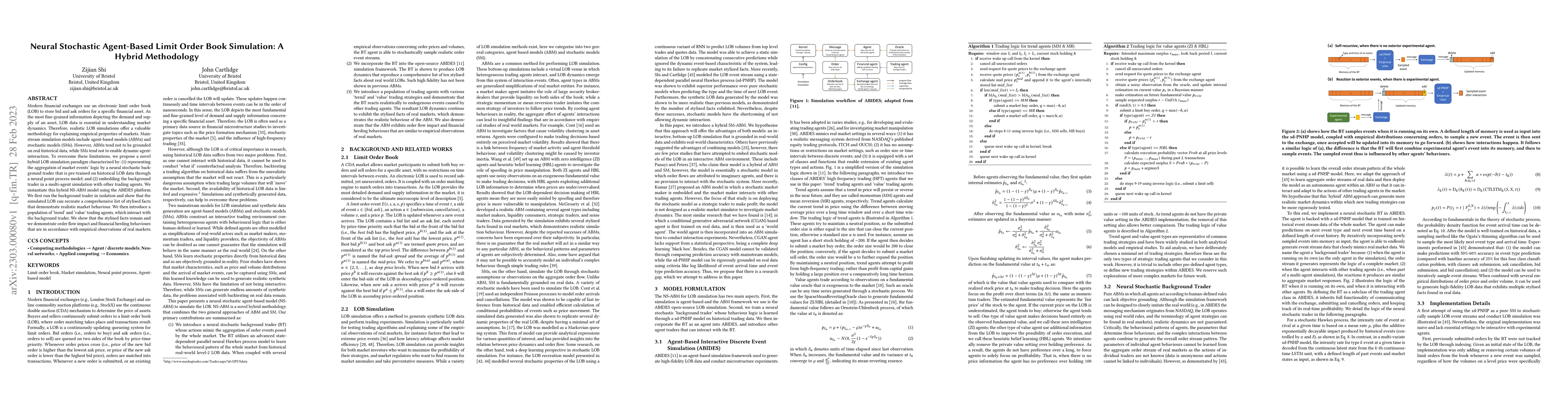

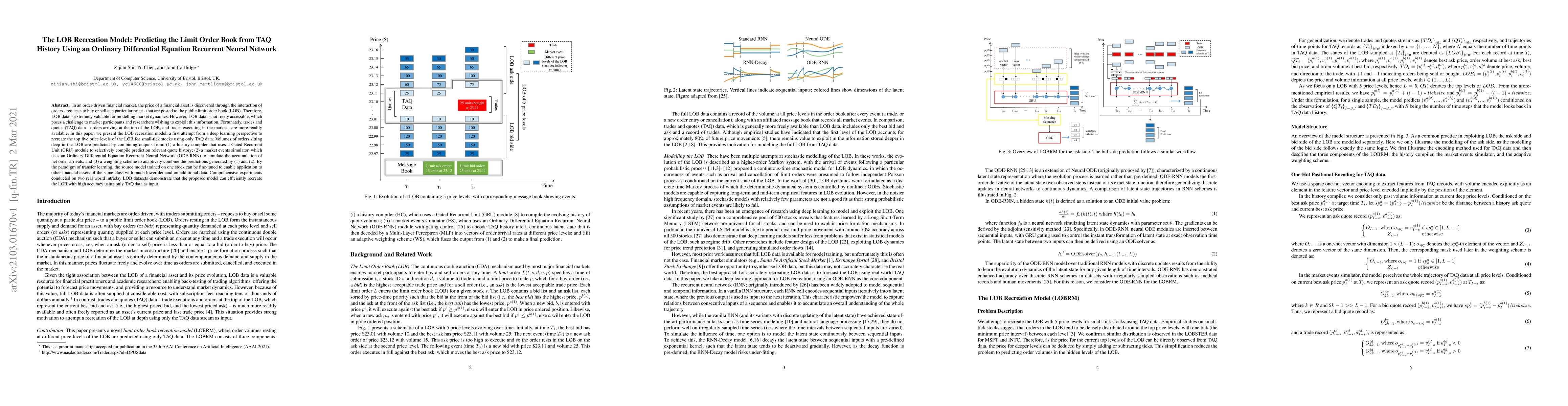

Modern financial exchanges use an electronic limit order book (LOB) to store bid and ask orders for a specific financial asset. As the most fine-grained information depicting the demand and supply o...

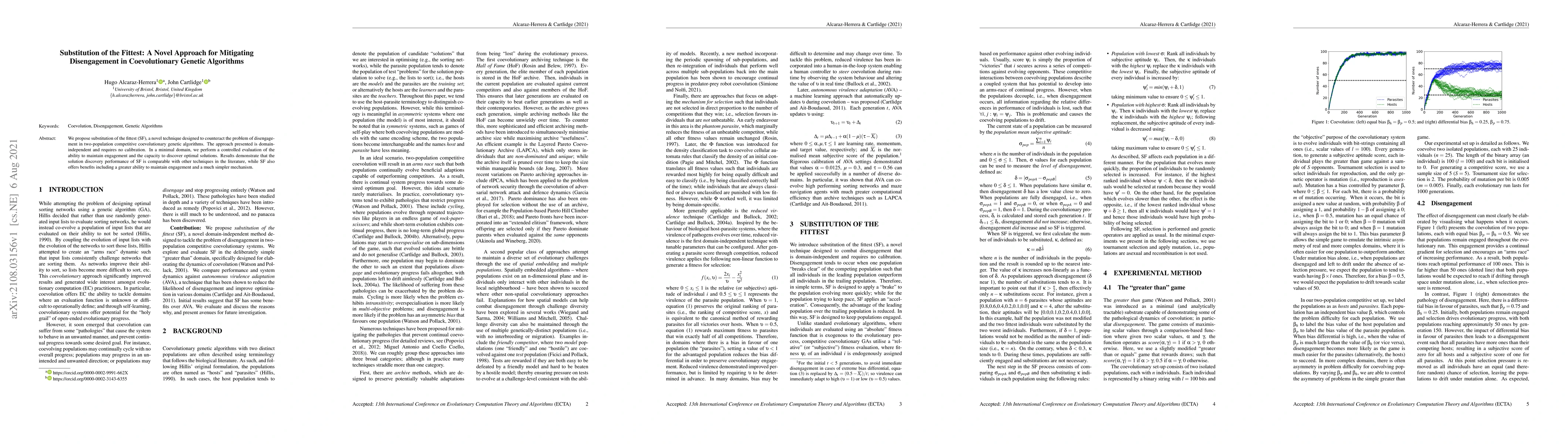

This research explores substitution of the fittest (SF), a technique designed to counteract the problem of disengagement in two-population competitive coevolutionary genetic algorithms. SF is domain...

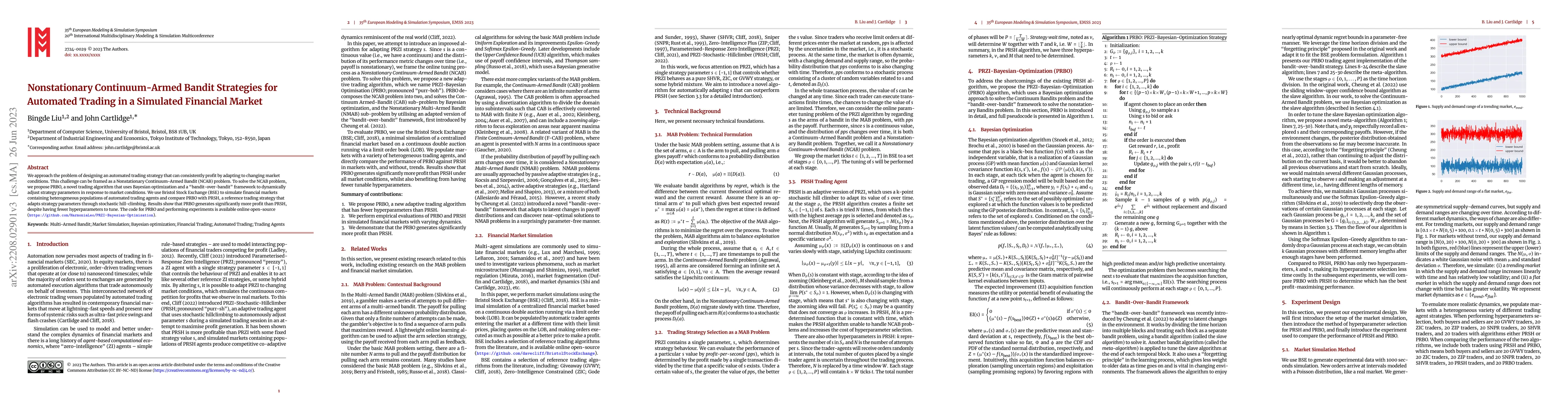

We approach the problem of designing an automated trading strategy that can consistently profit by adapting to changing market conditions. This challenge can be framed as a Nonstationary Continuum-A...

We propose substitution of the fittest (SF), a novel technique designed to counteract the problem of disengagement in two-population competitive coevolutionary genetic algorithms. The approach prese...

The limit order book (LOB) depicts the fine-grained demand and supply relationship for financial assets and is widely used in market microstructure studies. Nevertheless, the availability and high c...

In an order-driven financial market, the price of a financial asset is discovered through the interaction of orders - requests to buy or sell at a particular price - that are posted to the public li...

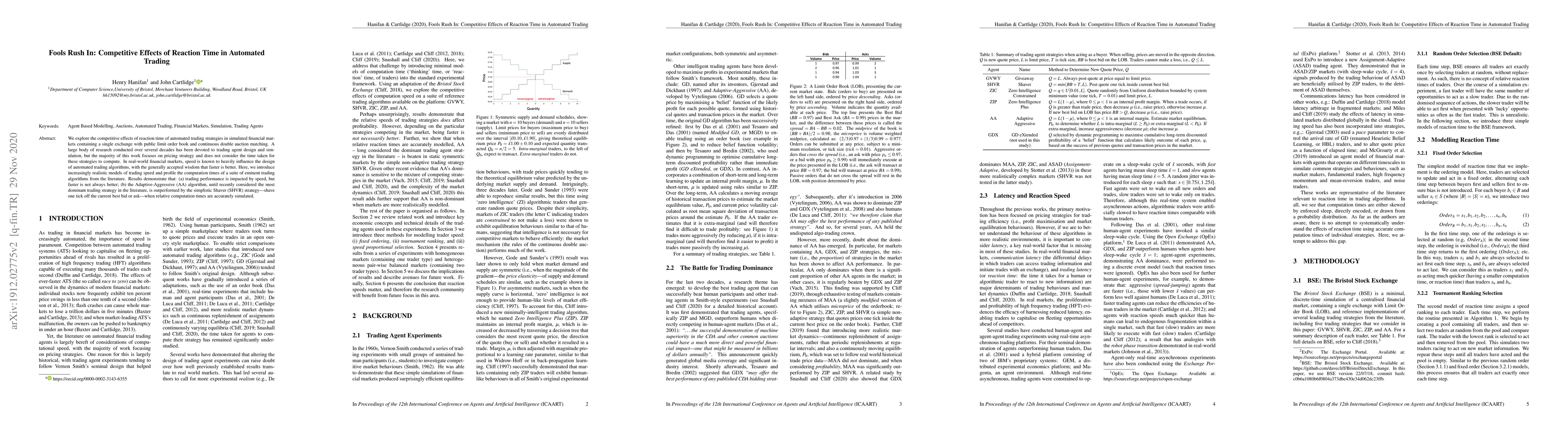

We consider issues of time in automated trading strategies in simulated financial markets containing a single exchange with public limit order book and continuous double auction matching. In particu...

We explore the competitive effects of reaction time of automated trading strategies in simulated financial markets containing a single exchange with public limit order book and continuous double auc...

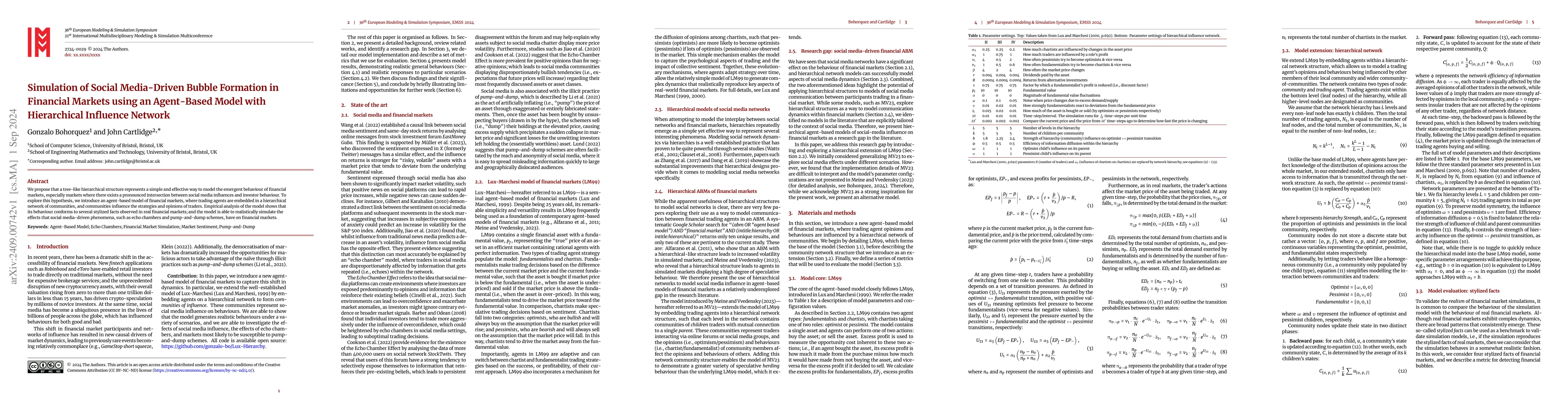

We propose that a tree-like hierarchical structure represents a simple and effective way to model the emergent behaviour of financial markets, especially markets where there exists a pronounced inters...

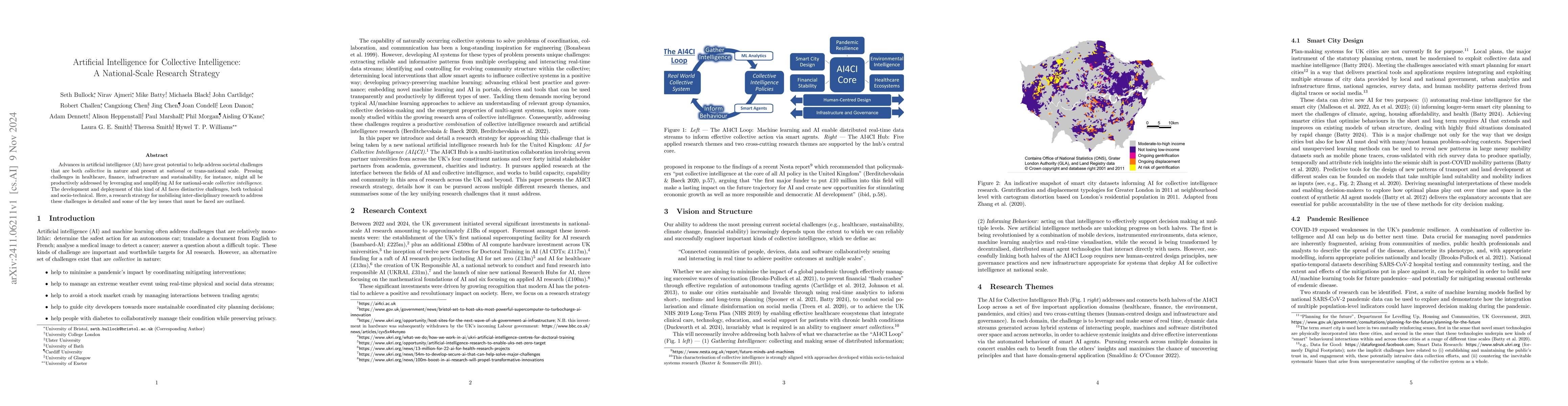

Advances in artificial intelligence (AI) have great potential to help address societal challenges that are both collective in nature and present at national or trans-national scale. Pressing challenge...

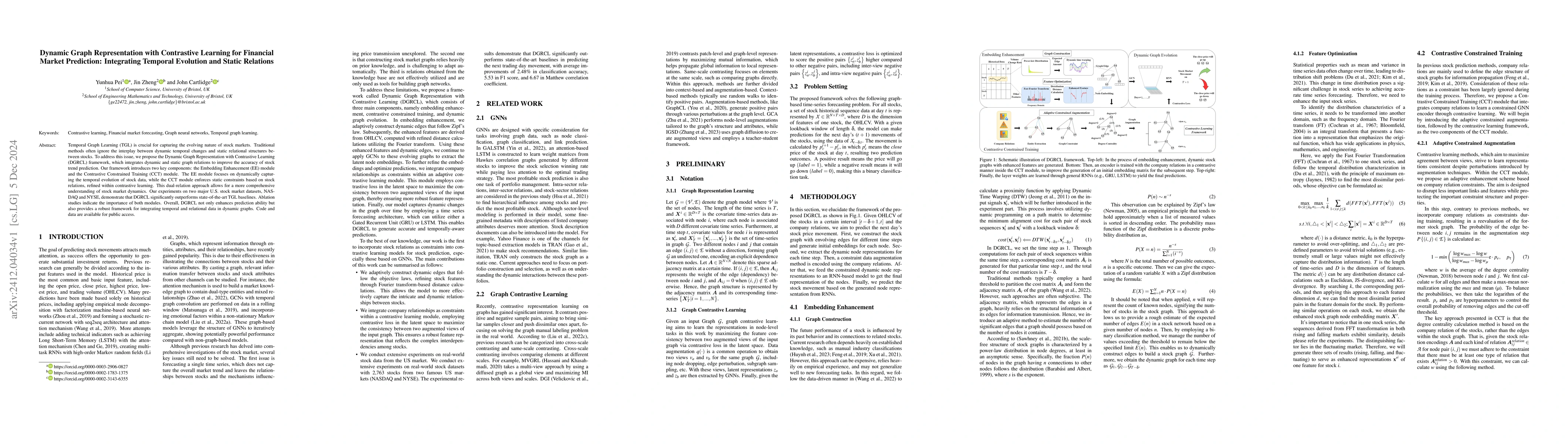

Temporal Graph Learning (TGL) is crucial for capturing the evolving nature of stock markets. Traditional methods often ignore the interplay between dynamic temporal changes and static relational struc...

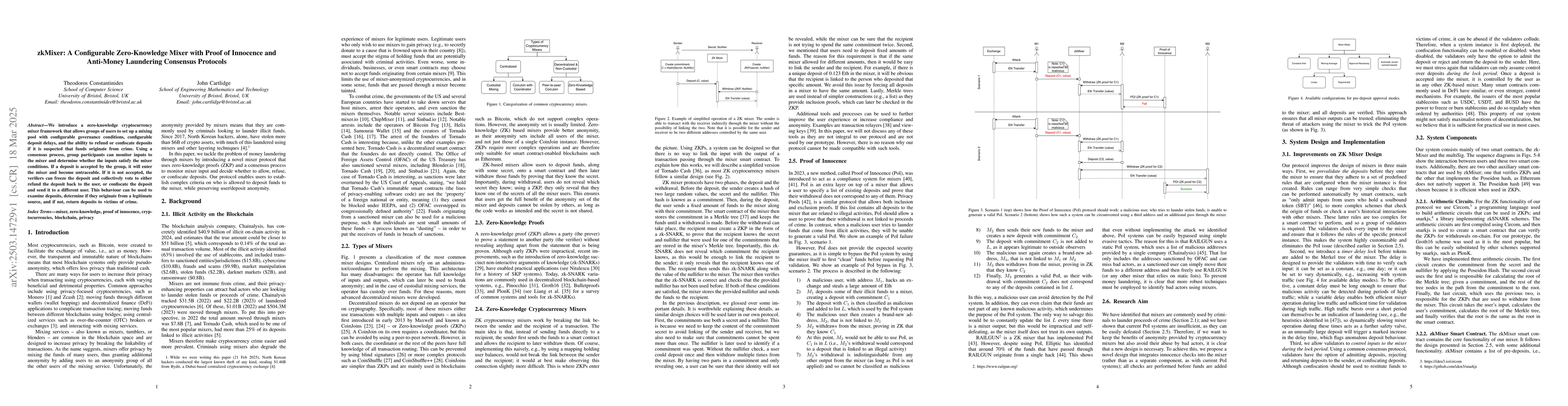

We introduce a zero-knowledge cryptocurrency mixer framework that allows groups of users to set up a mixing pool with configurable governance conditions, configurable deposit delays, and the ability t...

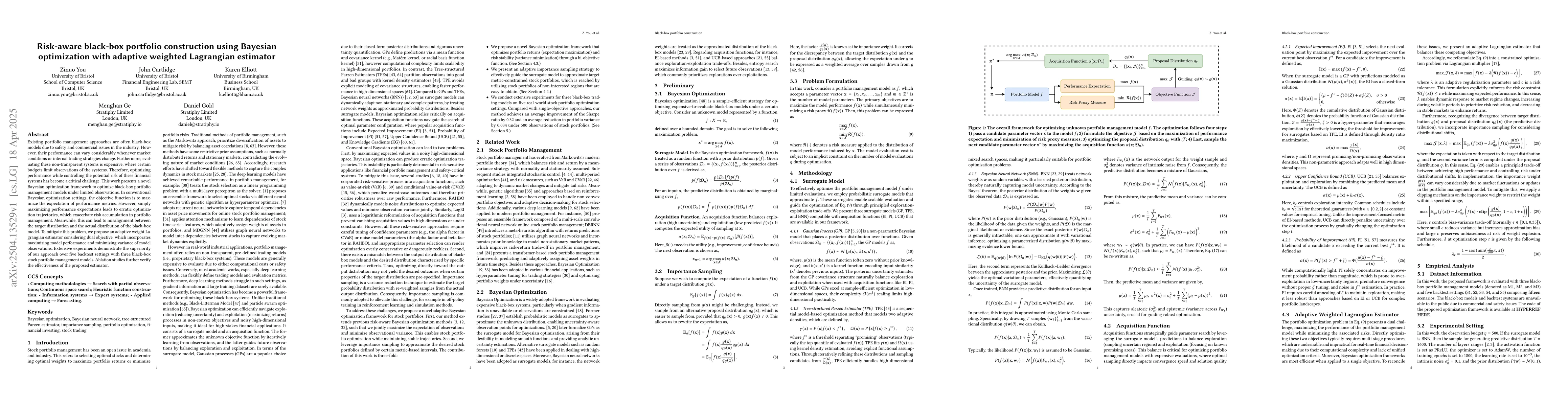

Existing portfolio management approaches are often black-box models due to safety and commercial issues in the industry. However, their performance can vary considerably whenever market conditions or ...

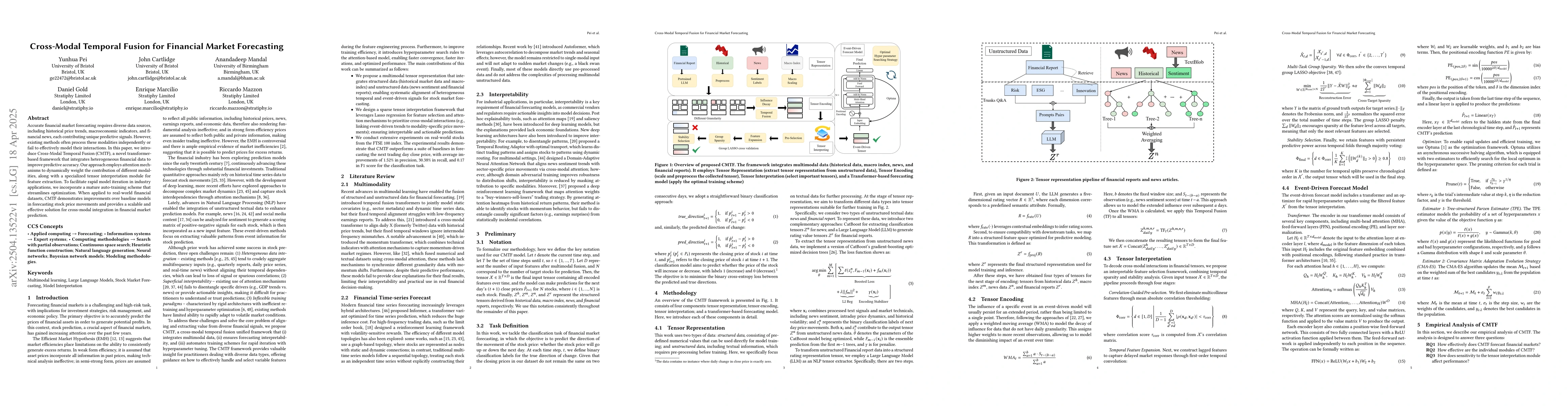

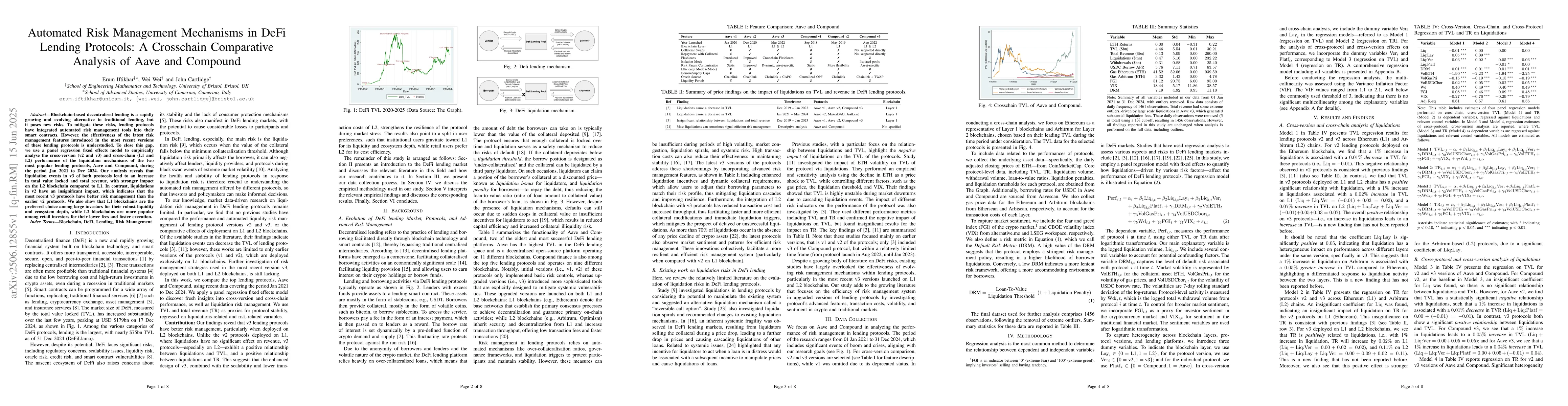

Accurate financial market forecasting requires diverse data sources, including historical price trends, macroeconomic indicators, and financial news, each contributing unique predictive signals. Howev...

Blockchain-based decentralised lending is a rapidly growing and evolving alternative to traditional lending, but it poses new risks. To mitigate these risks, lending protocols have integrated automate...

The optimal asset allocation between risky and risk-free assets is a persistent challenge due to the inherent volatility in financial markets. Conventional methods rely on strict distributional assump...

In time series forecasting, capturing recurrent temporal patterns is essential; decomposition techniques make such structure explicit and thereby improve predictive performance. Variational Mode Decom...

Intransitive player dominance, where player A beats B, B beats C, but C beats A, is common in competitive tennis. Yet, there are few known attempts to incorporate it within forecasting methods. We add...

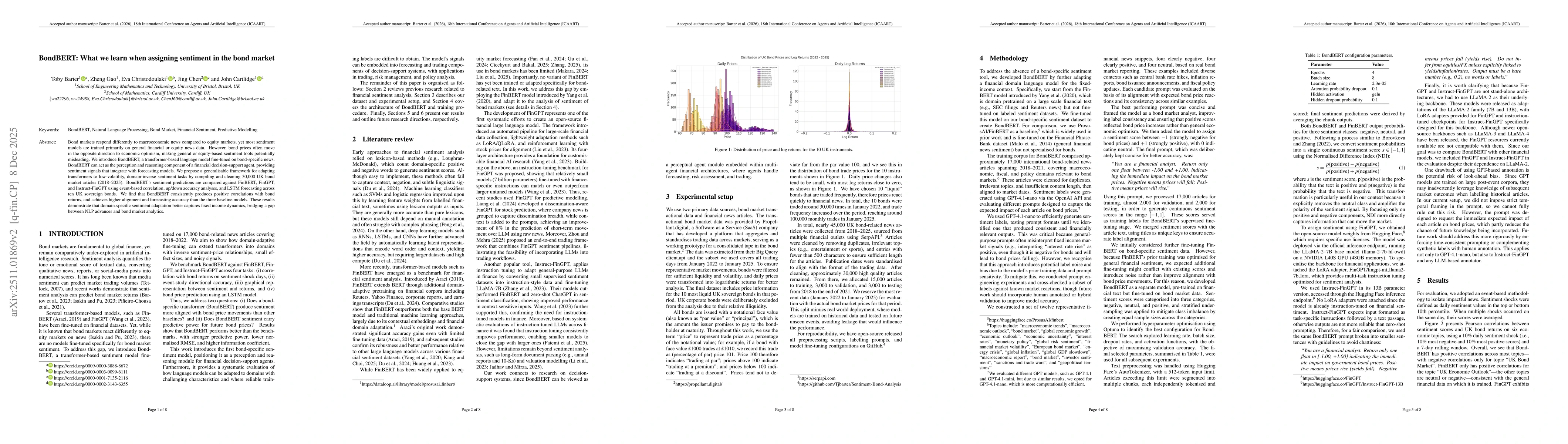

Bond markets respond differently to macroeconomic news compared to equity markets, yet most sentiment models, including FinBERT, are trained primarily on general financial or equity news data. This mi...

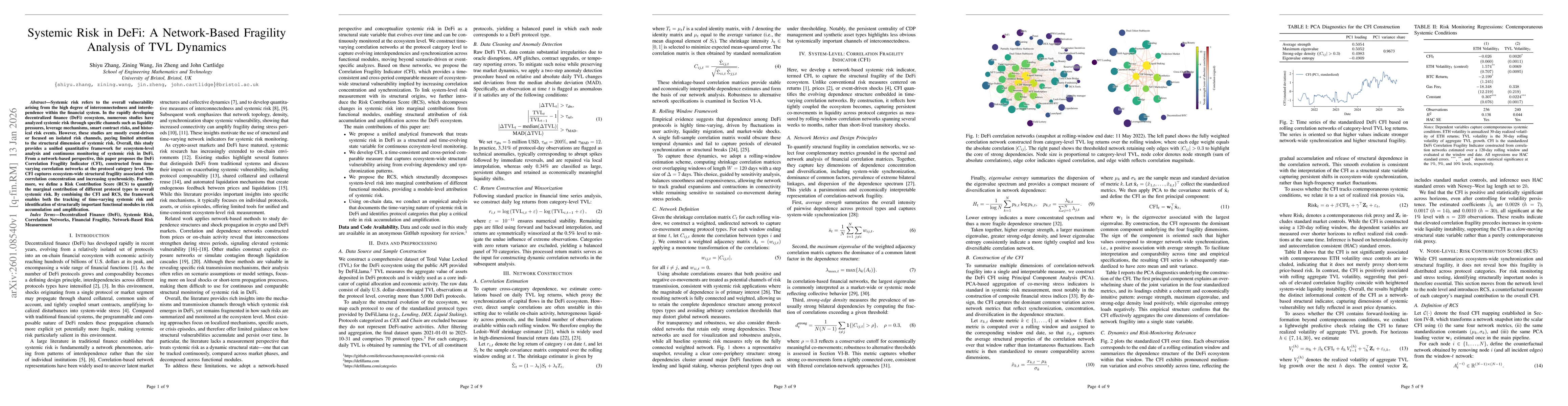

Systemic risk refers to the overall vulnerability arising from the high degree of interconnectedness and interdependence within the financial system. In the rapidly developing decentralized finance (D...

In-play football forecasting models have struggled to match the accuracy of betting exchange prices, which aggregate information from many market participants. We close this gap by combining two exten...

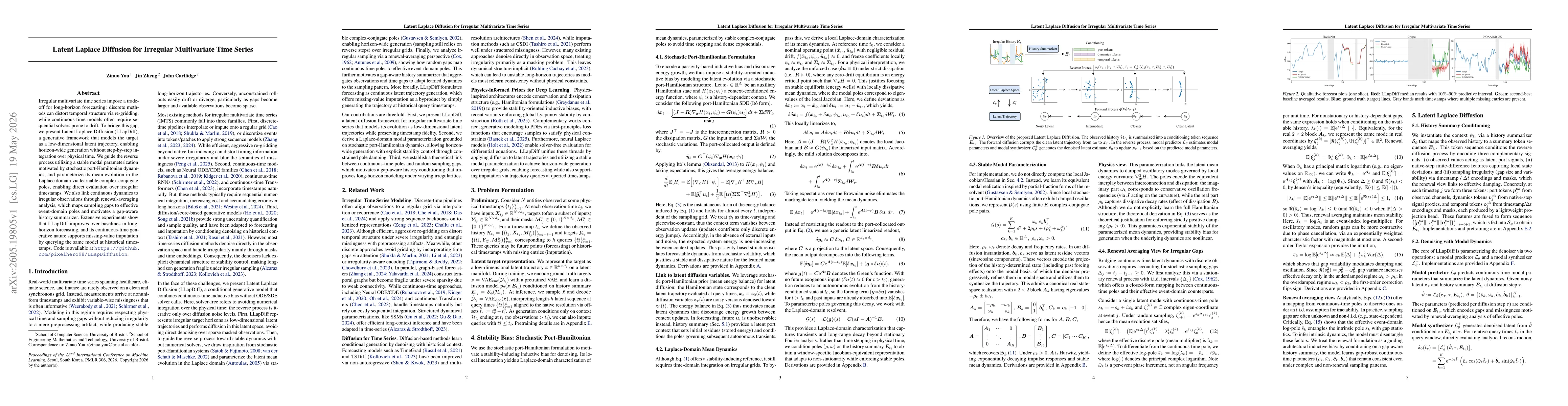

Irregular multivariate time series impose a trade-off for long-horizon forecasting: discrete methods can distort temporal structure via re-gridding, while continuous-time models often require sequenti...

Existing financial NLP benchmarks often rely on labels supplied by outside observers, measuring how language is perceived rather than what speakers have committed to in the market. We introduce StakeB...

Multi-agent LLM decision systems for portfolio management still lack a principled way to assign credit across specialist agents, remain vulnerable to cold-start dominance under regime shifts, and offe...

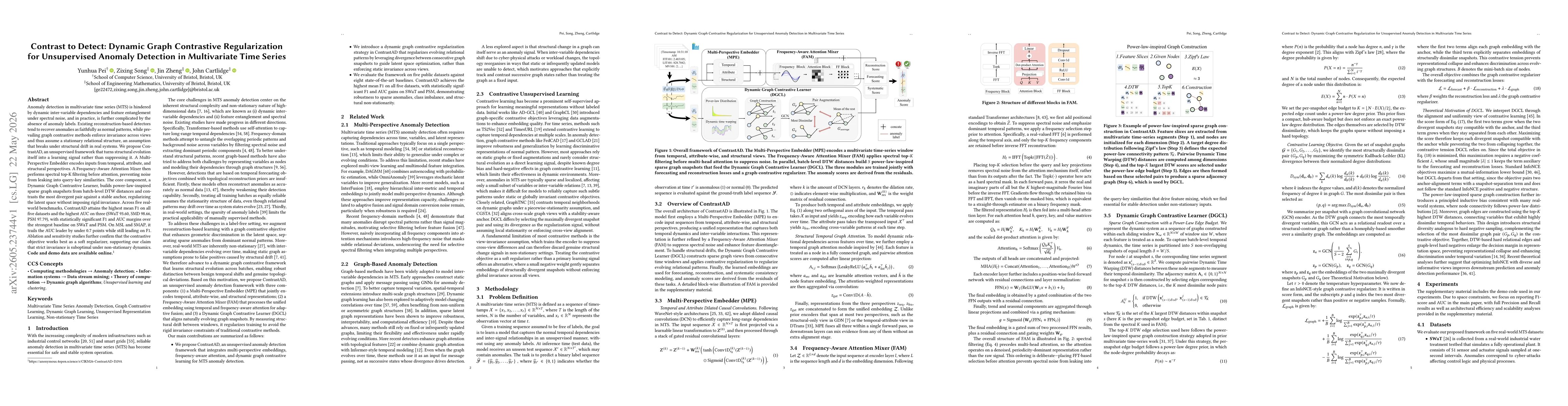

Anomaly detection in multivariate time series (MTS) is hindered by dynamic inter-variable dependencies and feature entanglement under spectral noise, and in practice, is further complicated by the abs...

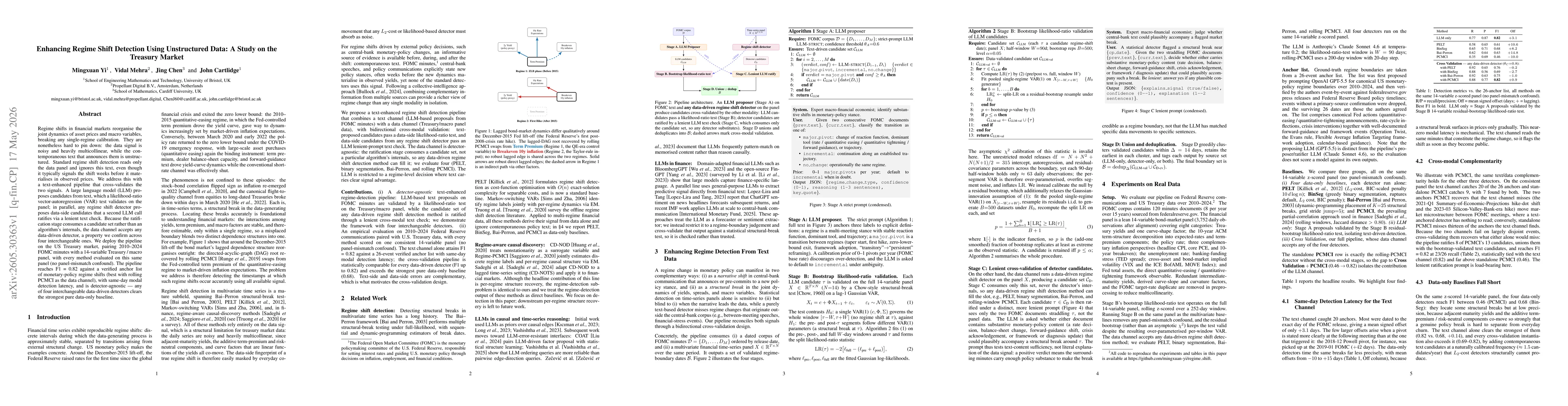

Regime shifts in financial markets reorganise the joint dynamics of asset prices and macro variables, breaking any single-regime calibration. They are nonetheless difficult to detect reliably because ...