Existing portfolio management approaches are often black-box models due to

safety and commercial issues in the industry. However, their performance can

vary considerably whenever market conditions or internal trading strategies

change. Furthermore, evaluating these non-transparent systems is expensive,

where certain budgets limit observations of the systems. Therefore, optimizing

performance while controlling the potential risk of these financial systems has

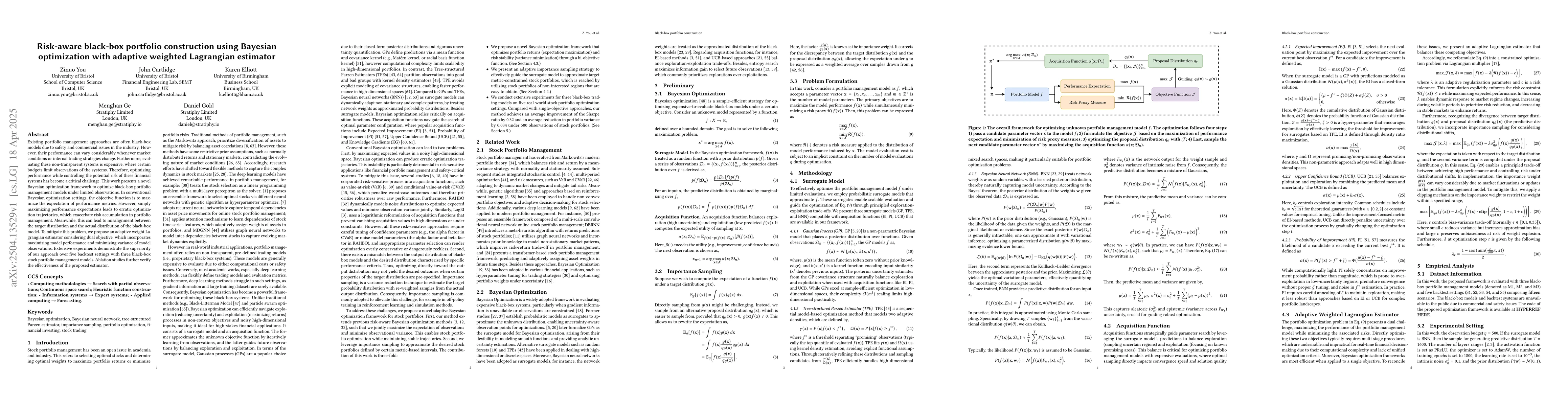

become a critical challenge. This work presents a novel Bayesian optimization

framework to optimize black-box portfolio management models under limited

observations. In conventional Bayesian optimization settings, the objective

function is to maximize the expectation of performance metrics. However, simply

maximizing performance expectations leads to erratic optimization trajectories,

which exacerbate risk accumulation in portfolio management. Meanwhile, this can

lead to misalignment between the target distribution and the actual

distribution of the black-box model. To mitigate this problem, we propose an

adaptive weight Lagrangian estimator considering dual objective, which

incorporates maximizing model performance and minimizing variance of model

observations. Extensive experiments demonstrate the superiority of our approach

over five backtest settings with three black-box stock portfolio management

models. Ablation studies further verify the effectiveness of the proposed

estimator.

Discussion 0