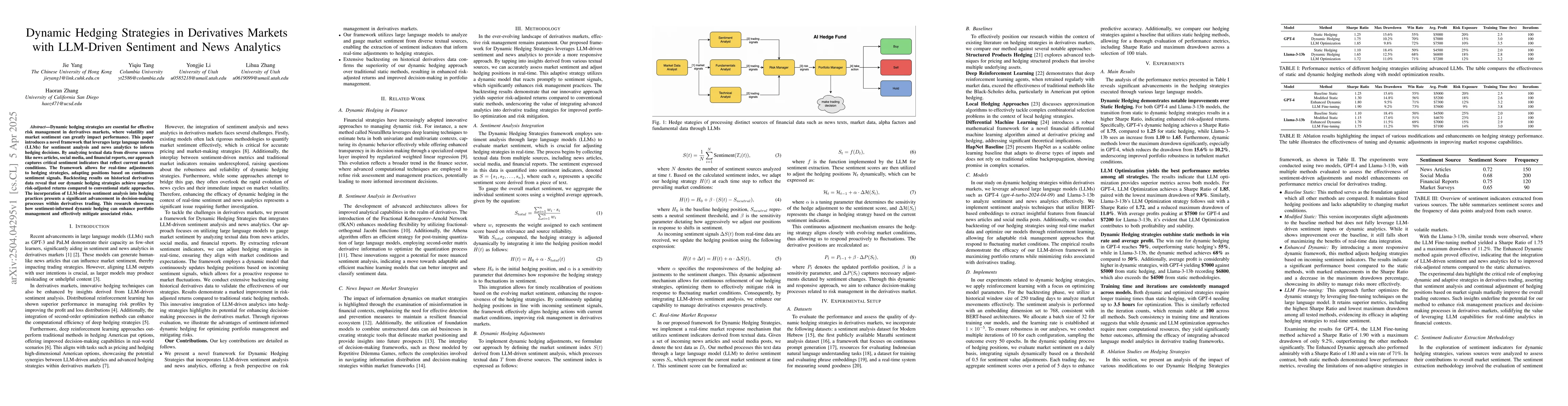

Dynamic hedging strategies are essential for effective risk management in

derivatives markets, where volatility and market sentiment can greatly impact

performance. This paper introduces a novel framework that leverages large

language models (LLMs) for sentiment analysis and news analytics to inform

hedging decisions. By analyzing textual data from diverse sources like news

articles, social media, and financial reports, our approach captures critical

sentiment indicators that reflect current market conditions. The framework

allows for real-time adjustments to hedging strategies, adapting positions

based on continuous sentiment signals. Backtesting results on historical

derivatives data reveal that our dynamic hedging strategies achieve superior

risk-adjusted returns compared to conventional static approaches. The

incorporation of LLM-driven sentiment analysis into hedging practices presents

a significant advancement in decision-making processes within derivatives

trading. This research showcases how sentiment-informed dynamic hedging can

enhance portfolio management and effectively mitigate associated risks.

Discussion 0