Publication

Metrics

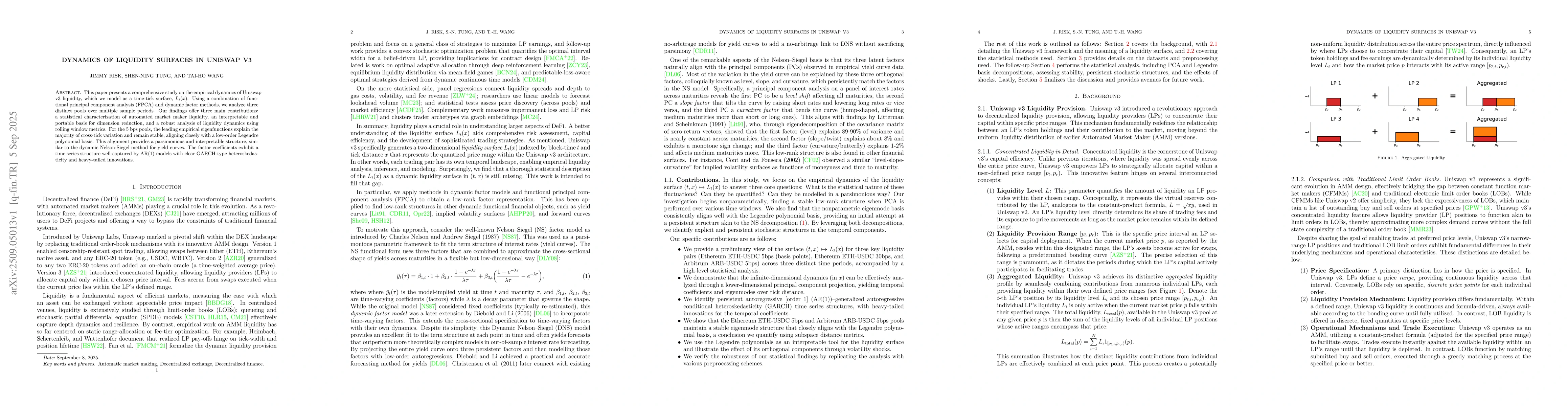

Paper Preview

Abstract

This paper presents a comprehensive study on the empirical dynamics of Uniswap v3 liquidity, which we model as a time-tick surface, $L_t(x)$. Using a combination of functional principal component analysis (FPCA) and dynamic factor methods, we analyze three distinct pools over multiple sample periods. Our findings offer three main contributions: a statistical characterization of automated market maker liquidity, an interpretable and portable basis for dimension reduction, and a robust analysis of liquidity dynamics using rolling window metrics. For the 5 bps pools, the leading empirical eigenfunctions explain the majority of cross-tick variation and remain stable, aligning closely with a low-order Legendre polynomial basis. This alignment provides a parsimonious and interpretable structure, similar to the dynamic Nelson-Siegel method for yield curves. The factor coefficients exhibit a time series structure well-captured by AR(1) models with clear GARCH-type heteroskedasticity and heavy-tailed innovations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0