Academic Profile

Statistics

Similar Authors

Papers on arXiv

Geometric mean market makers (G3Ms), such as Uniswap and Balancer, represent a widely used class of automated market makers (AMMs). These G3Ms are characterized by the following rule: the reserves o...

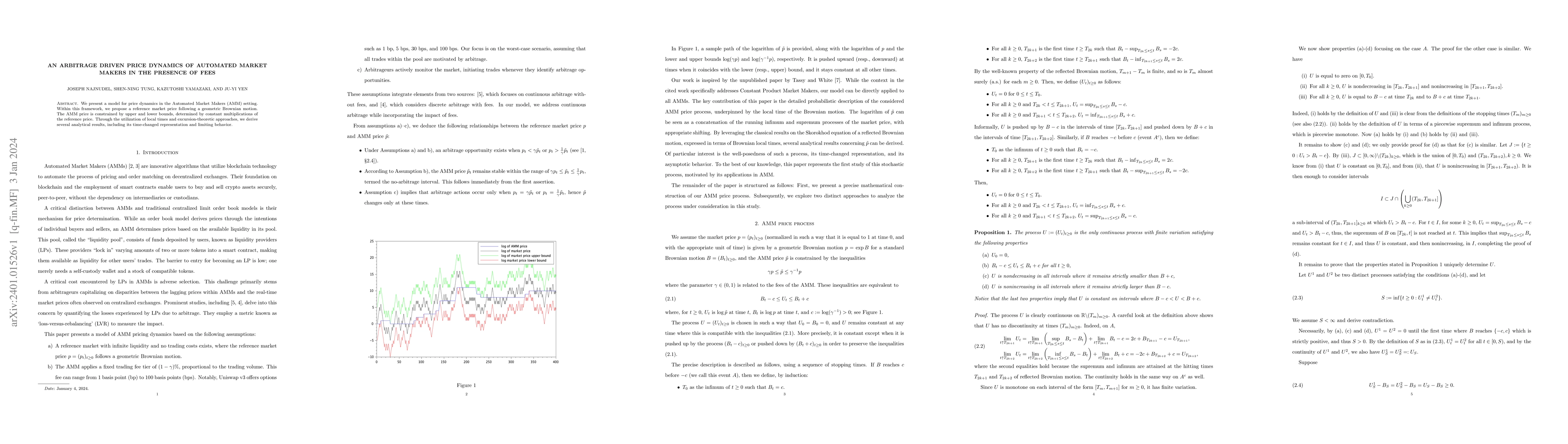

We present a model for price dynamics in the Automated Market Makers (AMM) setting. Within this framework, we propose a reference market price following a geometric Brownian motion. The AMM price is...

We establish Bernstein-centre type of results for the category of mod $p$ representations of $\mathrm{GL}_2(\mathbb{Q}_p)$. We treat all the remaining open cases, which occur when $p$ is $2$ or $3$....

Using $p$-adic local Langlands correspondence for $\operatorname{GL}_2(\mathbb{Q}_2)$ and an ordinary $R = \mathbb{T}$ theorem, we prove that the support of patched modules for quaternionic forms me...

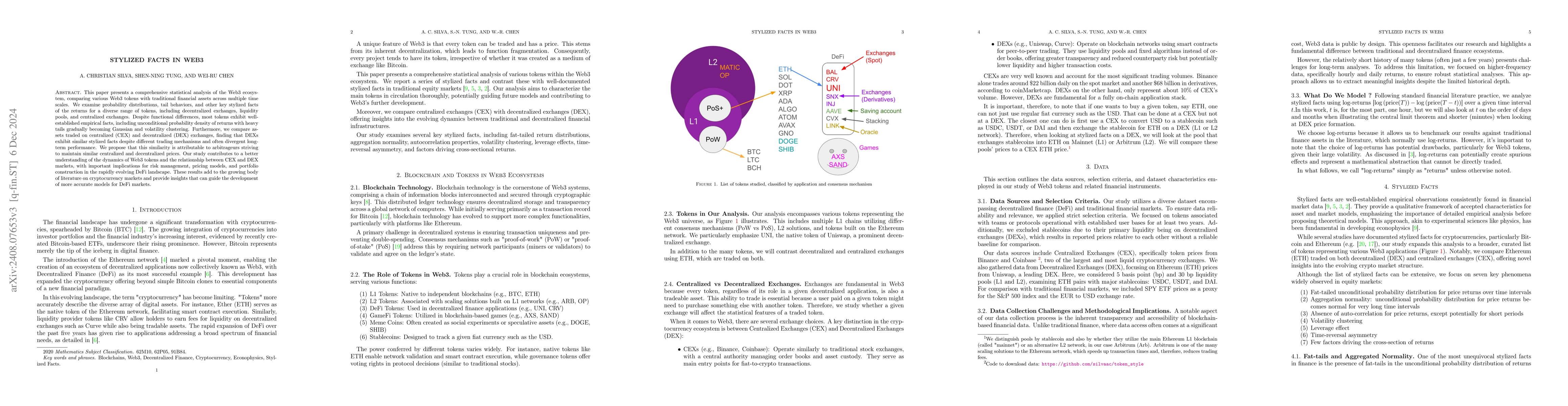

This paper presents a comprehensive statistical analysis of the Web3 ecosystem, comparing various Web3 tokens with traditional financial assets across multiple time scales. We examine probability dist...

This paper develops a rigorous mathematical framework for analyzing Concentrated Liquidity Market Makers (CLMMs) in Decentralized Finance (DeFi) within a continuous-time setting. We model the evolutio...

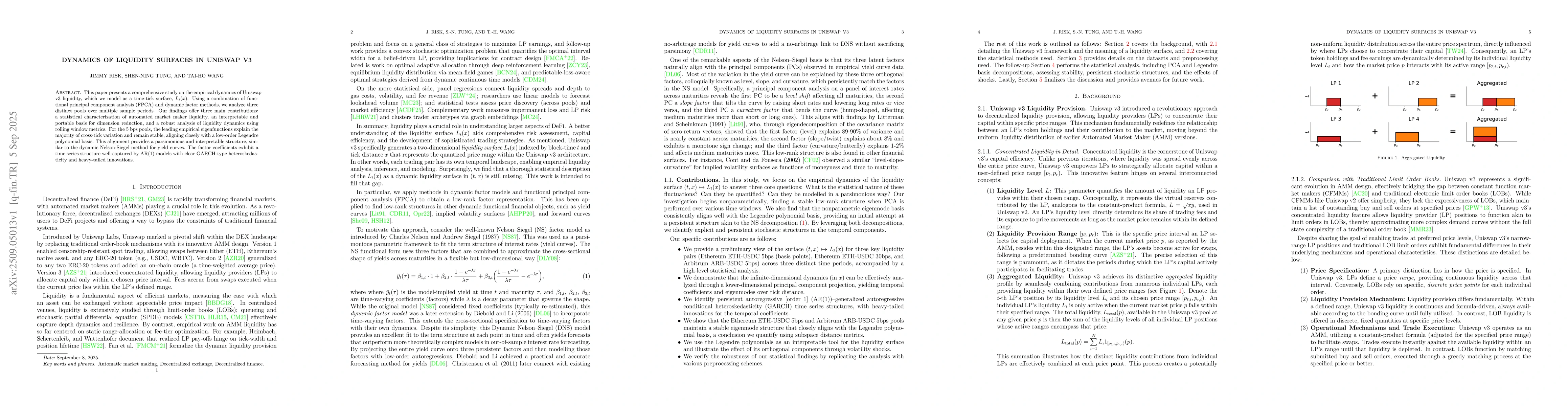

This paper presents a comprehensive study on the empirical dynamics of Uniswap v3 liquidity, which we model as a time-tick surface, $L_t(x)$. Using a combination of functional principal component anal...

This paper develops a robust mathematical framework for Constant Function Market Makers (CFMMs) by transitioning from traditional token reserve analyses to a coordinate system defined by price and int...