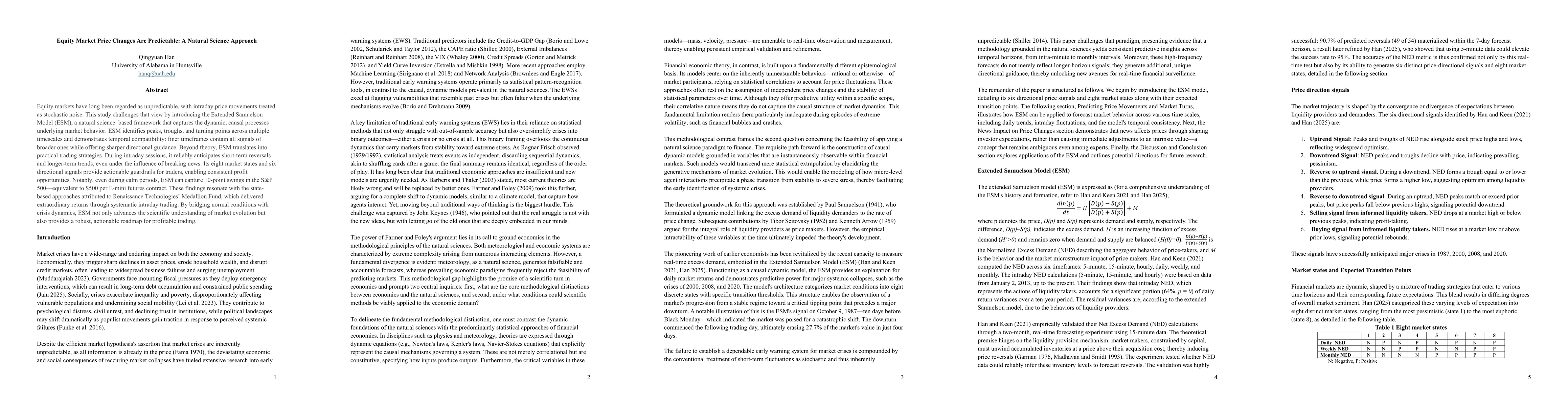

Equity markets have long been regarded as unpredictable, with intraday price

movements treated as stochastic noise. This study challenges that view by

introducing the Extended Samuelson Model (ESM), a natural science-based

framework that captures the dynamic, causal processes underlying market

behavior. ESM identifies peaks, troughs, and turning points across multiple

timescales and demonstrates temporal compatibility: finer timeframes contain

all signals of broader ones while offering sharper directional guidance. Beyond

theory, ESM translates into practical trading strategies. During intraday

sessions, it reliably anticipates short-term reversals and longer-term trends,

even under the influence of breaking news. Its eight market states and six

directional signals provide actionable guardrails for traders, enabling

consistent profit opportunities. Notably, even during calm periods, ESM can

capture 10-point swings in the S&P 500, equivalent to $500 per E-mini futures

contract. These findings resonate with the state-based approaches attributed to

Renaissance Technologies' Medallion Fund, which delivered extraordinary returns

through systematic intraday trading. By bridging normal conditions with crisis

dynamics, ESM not only advances the scientific understanding of market

evolution but also provides a robust, actionable roadmap for profitable

trading.

Discussion 0