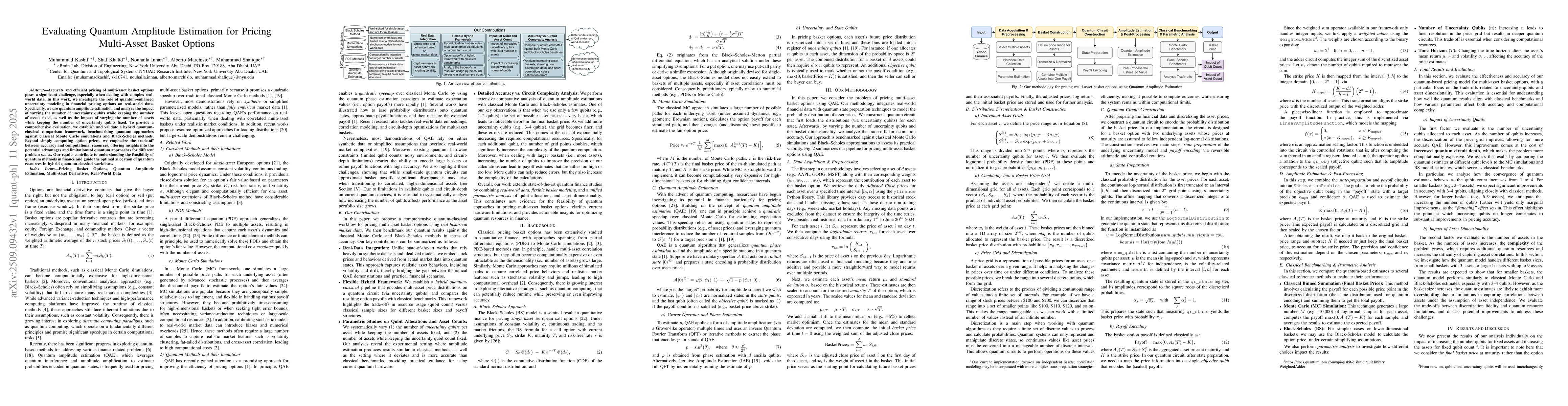

Accurate and efficient pricing of multi-asset basket options poses a

significant challenge, especially when dealing with complex real-world data. In

this work, we investigate the role of quantum-enhanced uncertainty modeling in

financial pricing options on real-world data. Specifically, we use quantum

amplitude estimation and analyze the impact of varying the number of

uncertainty qubits while keeping the number of assets fixed, as well as the

impact of varying the number of assets while keeping the number of uncertainty

qubits fixed. To provide a comprehensive evaluation, we establish and validate

a hybrid quantum-classical comparison framework, benchmarking quantum

approaches against classical Monte Carlo simulations and Black-Scholes methods.

Beyond simply computing option prices, we emphasize the trade-off between

accuracy and computational resources, offering insights into the potential

advantages and limitations of quantum approaches for different problem scales.

Our results contribute to understanding the feasibility of quantum methods in

finance and guide the optimal allocation of quantum resources in hybrid

quantum-classical workflows.

Discussion 0