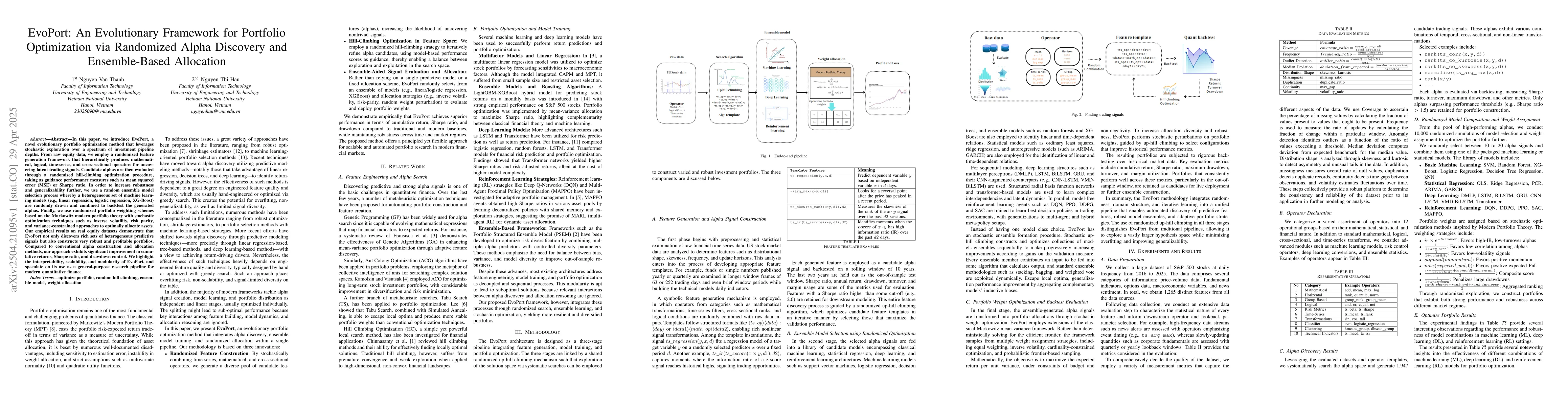

In this paper, we introduce EvoPort, a novel evolutionary portfolio

optimization method that leverages stochastic exploration over a spectrum of

investment pipeline depths. From raw equity data, we employ a randomized

feature generation framework that hierarchically produces mathematical,

logical, time-series, and cross-sectional operators for uncovering latent

trading signals. Candidate alphas are then evaluated through a randomized

hill-climbing optimization procedure, taking as guidance performance measures

such as mean squared error (MSE) or Sharpe ratio. In order to increase

robustness and generalizability further, we use a random ensemble model

selection process whereby a heterogeneous set of machine learning models (e.g.,

linear regression, logistic regression, XG-Boost) are randomly drawn and

combined to backtest the generated alphas. Finally, we use randomized portfolio

weighting schemes based on the Markowitz modern portfolio theory with

stochastic optimization techniques such as inverse volatility, risk parity, and

variance-constrained approaches to optimally allocate assets. Our empirical

results on real equity datasets demonstrate that EvoPort not only discovers

rich sets of heterogeneous predictive signals but also constructs very robust

and profitable portfolios. Compared to conventional alpha construction and

allocation methods, our approach exhibits significant improvement in cumulative

returns, Sharpe ratio, and drawdown control. We highlight the interpretability,

scalability, and modularity of EvoPort, and speculate on its use as a

general-purpose research pipeline for modern quantitative finance.

Discussion 0