01

MethodologyHow they did it

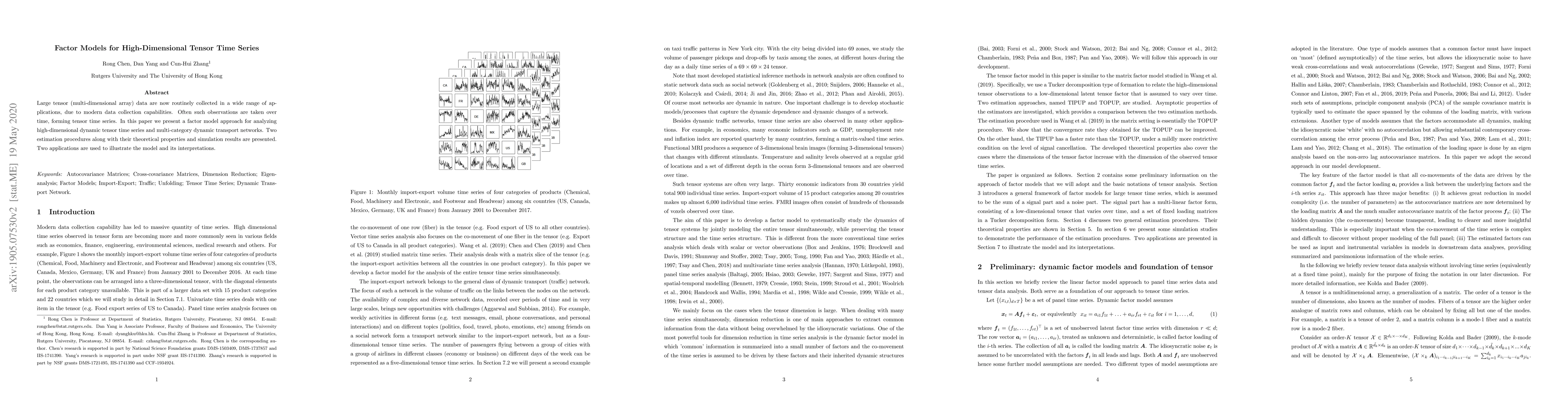

The paper presents a factor model approach for analyzing high-dimensional dynamic tensor time series and multi-category dynamic transport networks, providing two estimation procedures with theoretical properties and simulation results.

Discussion 0