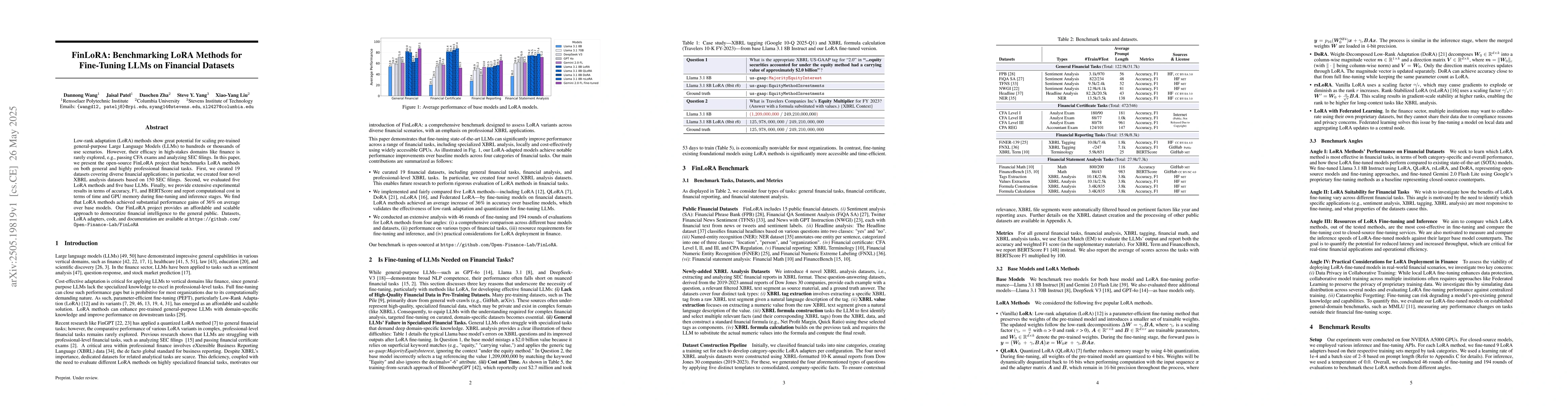

Low-rank adaptation (LoRA) methods show great potential for scaling

pre-trained general-purpose Large Language Models (LLMs) to hundreds or

thousands of use scenarios. However, their efficacy in high-stakes domains like

finance is rarely explored, e.g., passing CFA exams and analyzing SEC filings.

In this paper, we present the open-source FinLoRA project that benchmarks LoRA

methods on both general and highly professional financial tasks. First, we

curated 19 datasets covering diverse financial applications; in particular, we

created four novel XBRL analysis datasets based on 150 SEC filings. Second, we

evaluated five LoRA methods and five base LLMs. Finally, we provide extensive

experimental results in terms of accuracy, F1, and BERTScore and report

computational cost in terms of time and GPU memory during fine-tuning and

inference stages. We find that LoRA methods achieved substantial performance

gains of 36\% on average over base models. Our FinLoRA project provides an

affordable and scalable approach to democratize financial intelligence to the

general public. Datasets, LoRA adapters, code, and documentation are available

at https://github.com/Open-Finance-Lab/FinLoRA

Discussion 0