Academic Profile

Statistics

Similar Authors

Papers on arXiv

Financial large language models (FinLLMs) have been applied to various tasks in business, finance, accounting, and auditing. Complex financial regulations and standards are critical to financial servi...

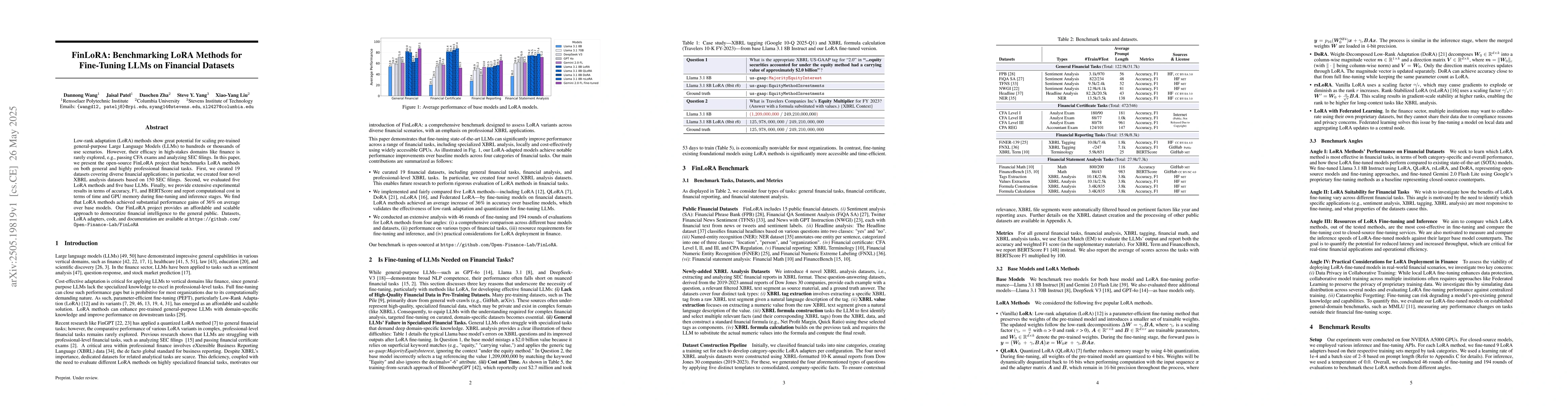

Low-rank adaptation (LoRA) methods show great potential for scaling pre-trained general-purpose Large Language Models (LLMs) to hundreds or thousands of use scenarios. However, their efficacy in high-...

The complexity of the Generally Accepted Accounting Principles (GAAP) and the hierarchical structure of eXtensible Business Reporting Language (XBRL) filings make financial auditing increasingly diffi...

Previous research has reported that large language models (LLMs) demonstrate poor performance on the Chartered Financial Analyst (CFA) exams. However, recent reasoning models have achieved strong resu...

Over the past three years, the financial services industry has witnessed Large Language Models (LLMs) and agents transitioning from the exploration stage to readiness and governance stages. Financial ...

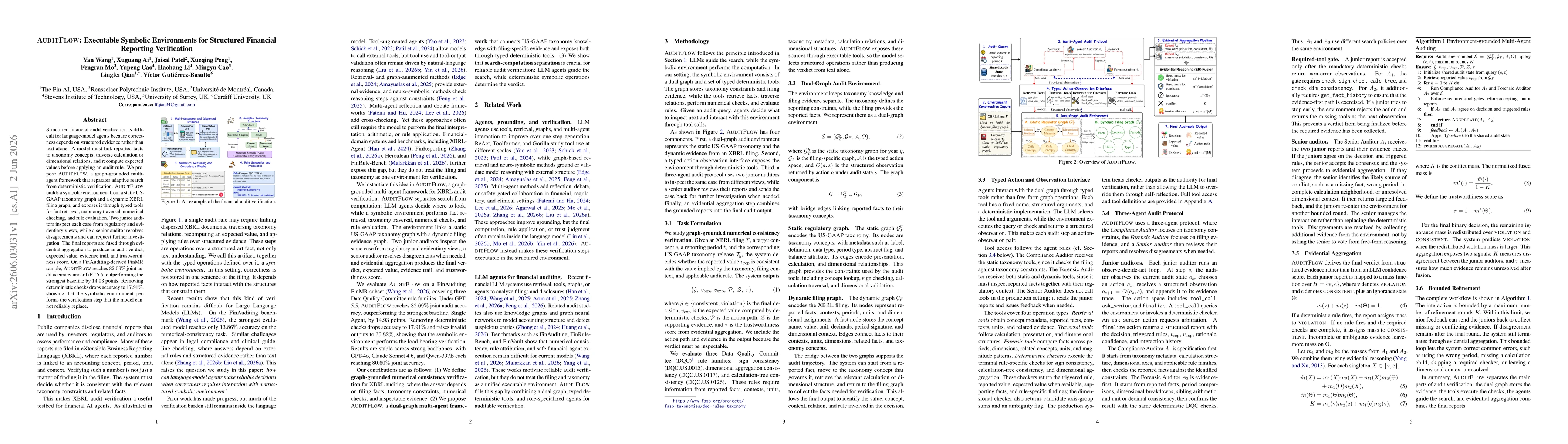

Structured financial audit verification is difficult for language-model agents because correctness depends on structured evidence rather than text alone. A model must link reported facts to taxonomy c...

Structured financial audit verification is difficult for language-model agents because correctness depends on structured evidence rather than text alone. A model must link reported facts to taxonomy c...