The exceptional potential of large language models (LLMs) in handling text

information has garnered significant attention in the field of financial

trading. However, current trading agents primarily focus on single-step trading

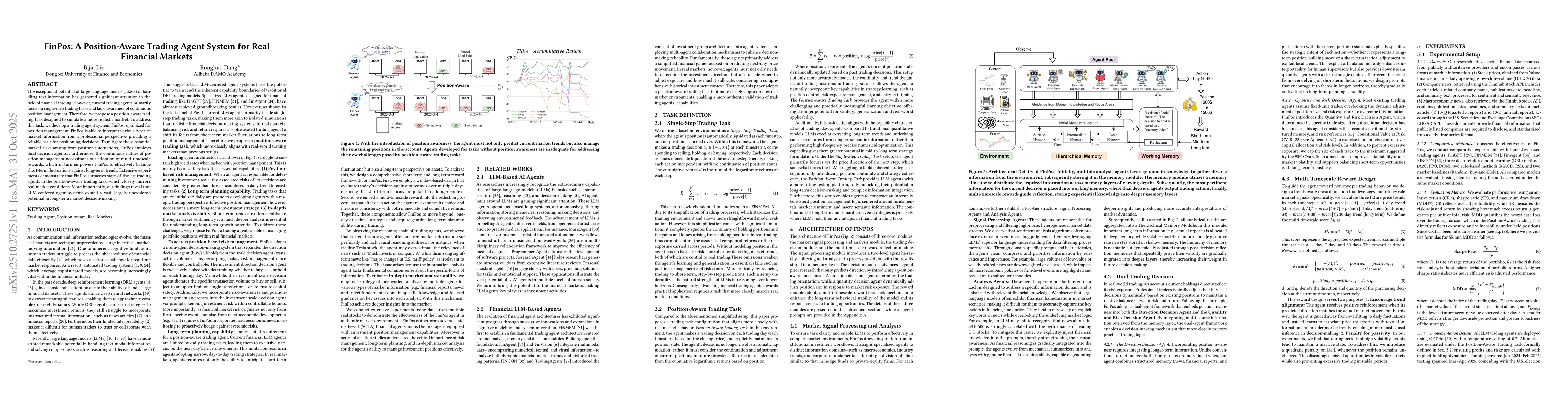

tasks and lack awareness of continuous position management. Therefore, we

propose a position-aware trading task designed to simulate a more realistic

market. To address this task, we develop a trading agent system, FinPos,

optimized for position management. FinPos is able to interpret various types of

market information from a professional perspective, providing a reliable basis

for positioning decisions. To mitigate the substantial market risks arising

from position fluctuations, FinPos employs dual decision agents. Furthermore,

the continuous nature of position management necessitates our adoption of

multi-timescale rewards, which in turn empowers FinPos to effectively balance

short-term fluctuations against long-term trends. Extensive experiments

demonstrate that FinPos surpasses state-of-the-art trading agents in the

position-aware trading task, which closely mirrors real market conditions. More

importantly, our findings reveal that LLM-centered agent systems exhibit a

vast, largely unexplored potential in long-term market decision-making.

Discussion 0