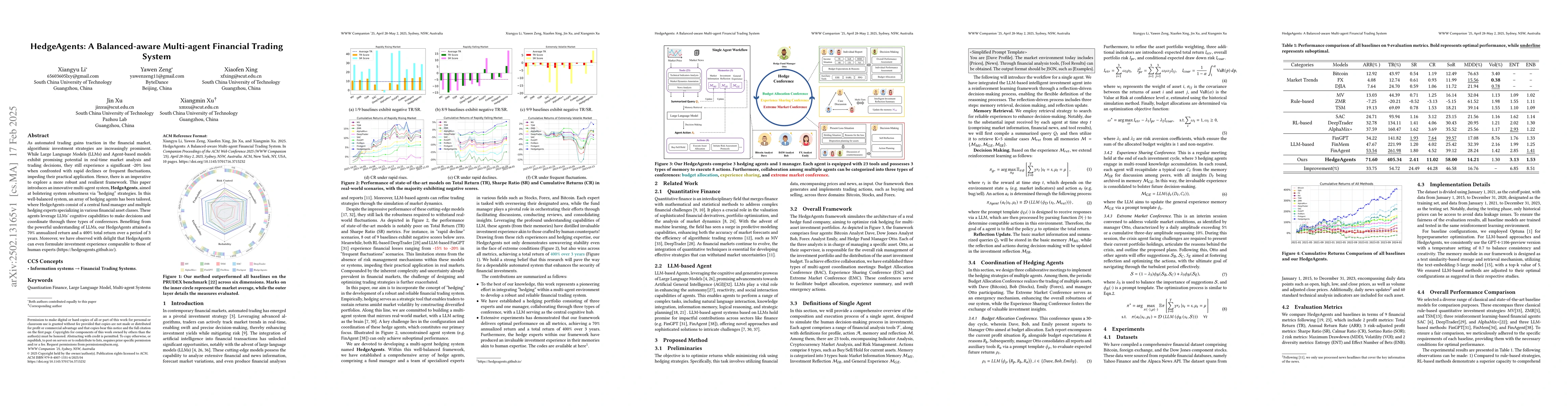

As automated trading gains traction in the financial market, algorithmic

investment strategies are increasingly prominent. While Large Language Models

(LLMs) and Agent-based models exhibit promising potential in real-time market

analysis and trading decisions, they still experience a significant -20% loss

when confronted with rapid declines or frequent fluctuations, impeding their

practical application. Hence, there is an imperative to explore a more robust

and resilient framework. This paper introduces an innovative multi-agent

system, HedgeAgents, aimed at bolstering system robustness via ``hedging''

strategies. In this well-balanced system, an array of hedging agents has been

tailored, where HedgeAgents consist of a central fund manager and multiple

hedging experts specializing in various financial asset classes. These agents

leverage LLMs' cognitive capabilities to make decisions and coordinate through

three types of conferences. Benefiting from the powerful understanding of LLMs,

our HedgeAgents attained a 70% annualized return and a 400% total return over a

period of 3 years. Moreover, we have observed with delight that HedgeAgents can

even formulate investment experience comparable to those of human experts

(https://hedgeagents.github.io/).

Discussion 0