Financial sentiment analysis (FSA) has attracted significant attention, and

recent studies increasingly explore large language models (LLMs) for this

field. Yet most work evaluates only classification metrics, leaving unclear

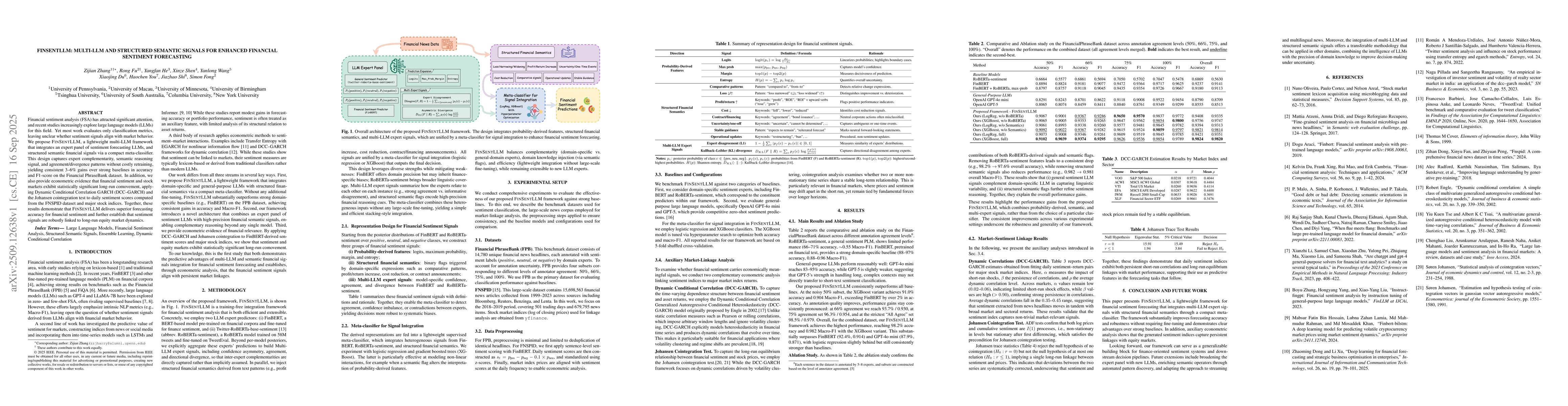

whether sentiment signals align with market behavior. We propose FinSentLLM, a

lightweight multi-LLM framework that integrates an expert panel of sentiment

forecasting LLMs, and structured semantic financial signals via a compact

meta-classifier. This design captures expert complementarity, semantic

reasoning signal, and agreement/divergence patterns without costly retraining,

yielding consistent 3-6% gains over strong baselines in accuracy and F1-score

on the Financial PhraseBank dataset. In addition, we also provide econometric

evidence that financial sentiment and stock markets exhibit statistically

significant long-run comovement, applying Dynamic Conditional Correlation GARCH

(DCC-GARCH) and the Johansen cointegration test to daily sentiment scores

computed from the FNSPID dataset and major stock indices. Together, these

results demonstrate that FinSentLLM delivers superior forecasting accuracy for

financial sentiment and further establish that sentiment signals are robustly

linked to long-run equity market dynamics.

Discussion 0