Fractional SDE-Net: Generation of Time Series Data with Long-term Memory

Publication

Metrics

AI Quick Summary

This paper proposes fSDE-Net, a neural fractional Stochastic Differential Equation Network, to generate time series data with long-term memory. The model uses fractional Brownian motion to replicate the long-range dependency properties observed in real-world time series data from various fields.

Paper Preview

Abstract

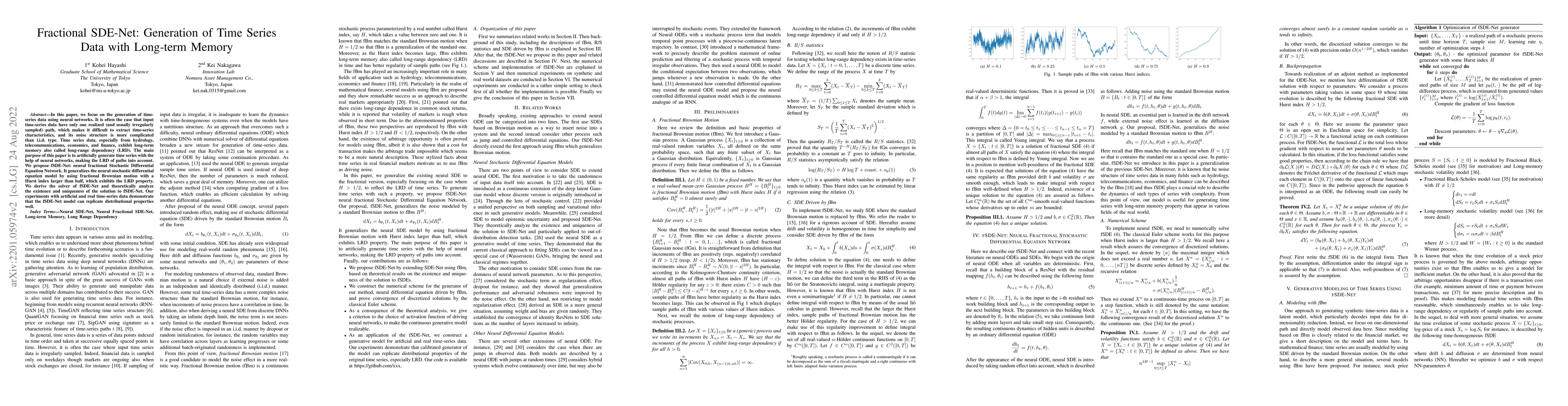

In this paper, we focus on the generation of time-series data using neural networks. It is often the case that input time-series data have only one realized (and usually irregularly sampled) path, which makes it difficult to extract time-series characteristics, and its noise structure is more complicated than i.i.d. type. Time series data, especially from hydrology, telecommunications, economics, and finance, exhibit long-term memory also called long-range dependency (LRD). The main purpose of this paper is to artificially generate time series with the help of neural networks, making the LRD of paths into account. We propose fSDE-Net: neural fractional Stochastic Differential Equation Network. It generalizes the neural stochastic differential equation model by using fractional Brownian motion with a Hurst index larger than half, which exhibits the LRD property. We derive the solver of fSDE-Net and theoretically analyze the existence and uniqueness of the solution to fSDE-Net. Our experiments with artificial and real time-series data demonstrate that the fSDE-Net model can replicate distributional properties well.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0