Academic Profile

Statistics

Similar Authors

Papers on arXiv

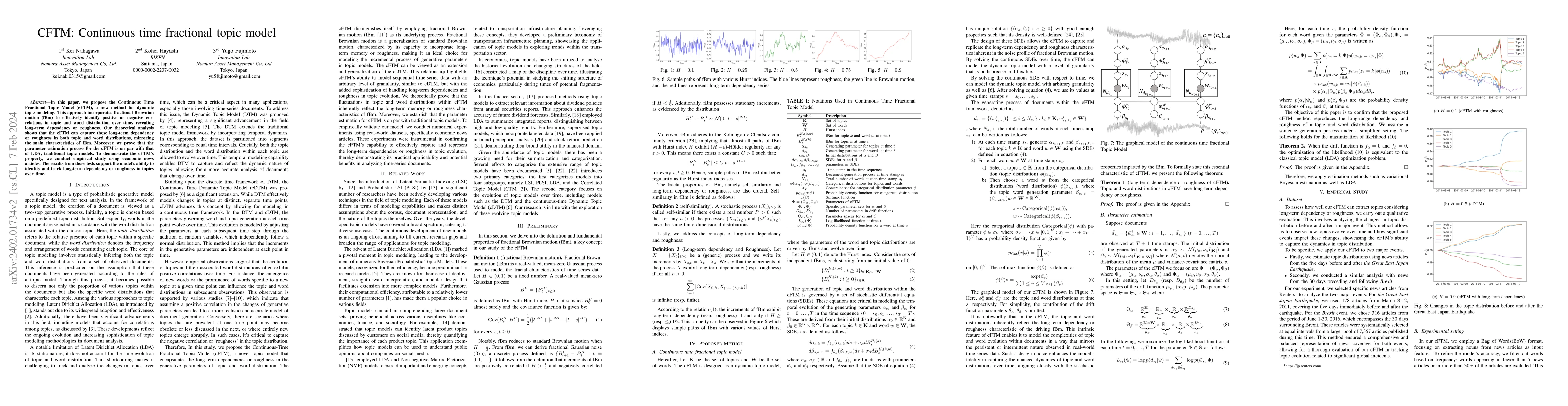

In this paper, we propose the Continuous Time Fractional Topic Model (cFTM), a new method for dynamic topic modeling. This approach incorporates fractional Brownian motion~(fBm) to effectively ident...

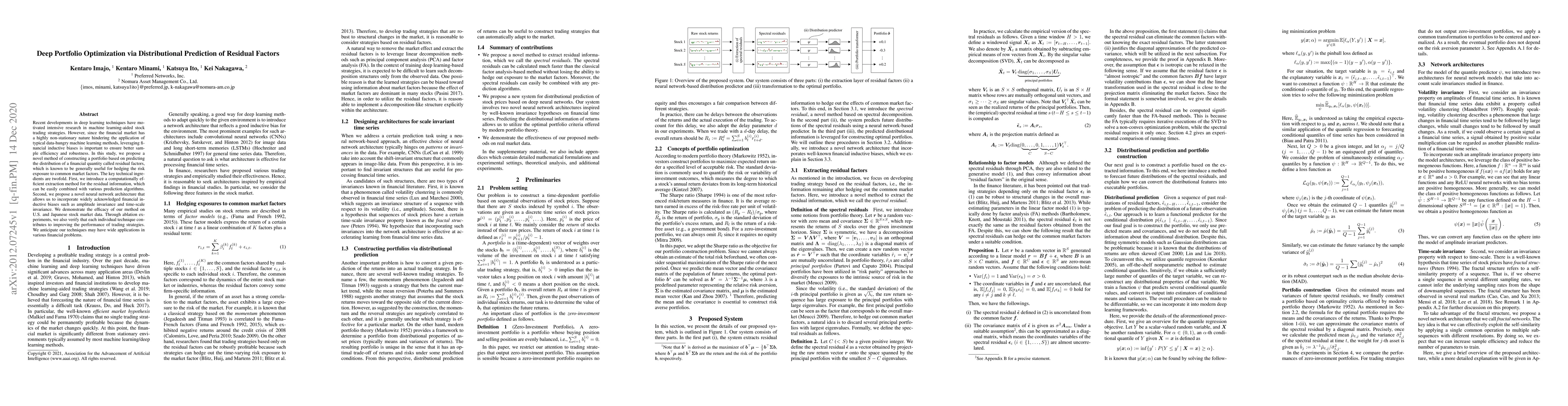

In this study, we address the challenge of portfolio optimization, a critical aspect of managing investment risks and maximizing returns. The mean-CVaR portfolio is considered a promising method due...

Quantum computers are gaining attention for their ability to solve certain problems faster than classical computers, and one example is the quantum expectation estimation algorithm that accelerates ...

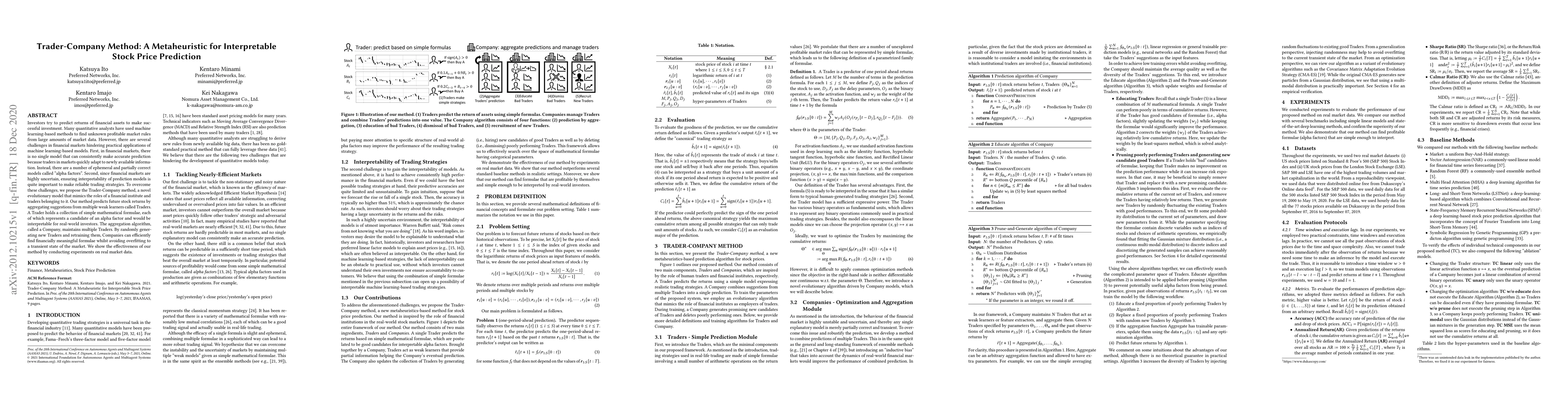

Machine learning is an increasingly popular tool with some success in predicting stock prices. One promising method is the Trader-Company~(TC) method, which takes into account the dynamism of the st...

The mean-variance portfolio that considers the trade-off between expected return and risk has been widely used in the problem of asset allocation for multi-asset portfolios. However, since it is dif...

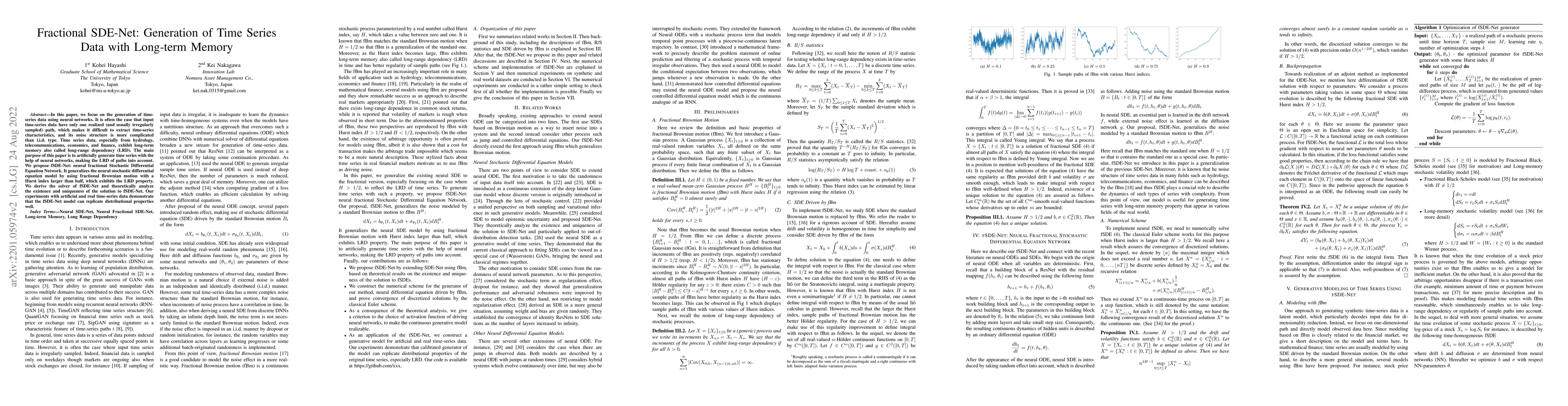

In this paper, we focus on the generation of time-series data using neural networks. It is often the case that input time-series data have only one realized (and usually irregularly sampled) path, w...

For supervised classification problems, this paper considers estimating the query's label probability through local regression using observed covariates. Well-known nonparametric kernel smoother and...

Deep hedging (Buehler et al. 2019) is a versatile framework to compute the optimal hedging strategy of derivatives in incomplete markets. However, this optimal strategy is hard to train due to actio...

We consider controlling the false discovery rate for testing many time series with an unknown cross-sectional correlation structure. Given a large number of hypotheses, false and missing discoveries...

Investors try to predict returns of financial assets to make successful investment. Many quantitative analysts have used machine learning-based methods to find unknown profitable market rules from l...

Recent developments in deep learning techniques have motivated intensive research in machine learning-aided stock trading strategies. However, since the financial market has a highly non-stationary ...

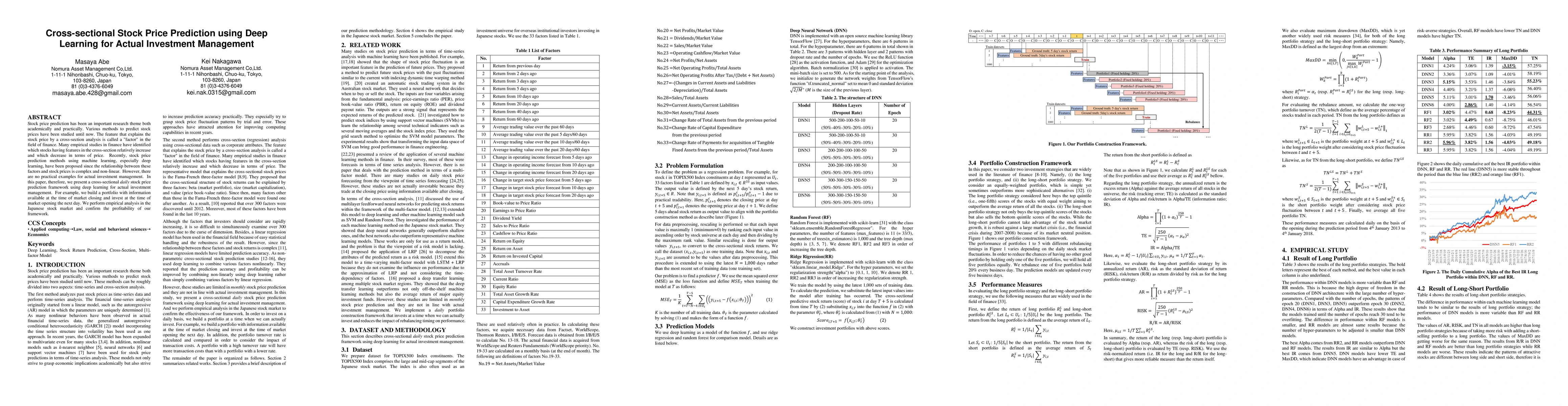

Stock price prediction has been an important research theme both academically and practically. Various methods to predict stock prices have been studied until now. The feature that explains the stoc...

Optimal asset allocation is a key topic in modern finance theory. To realize the optimal asset allocation on investor's risk aversion, various portfolio construction methods have been proposed. Rece...

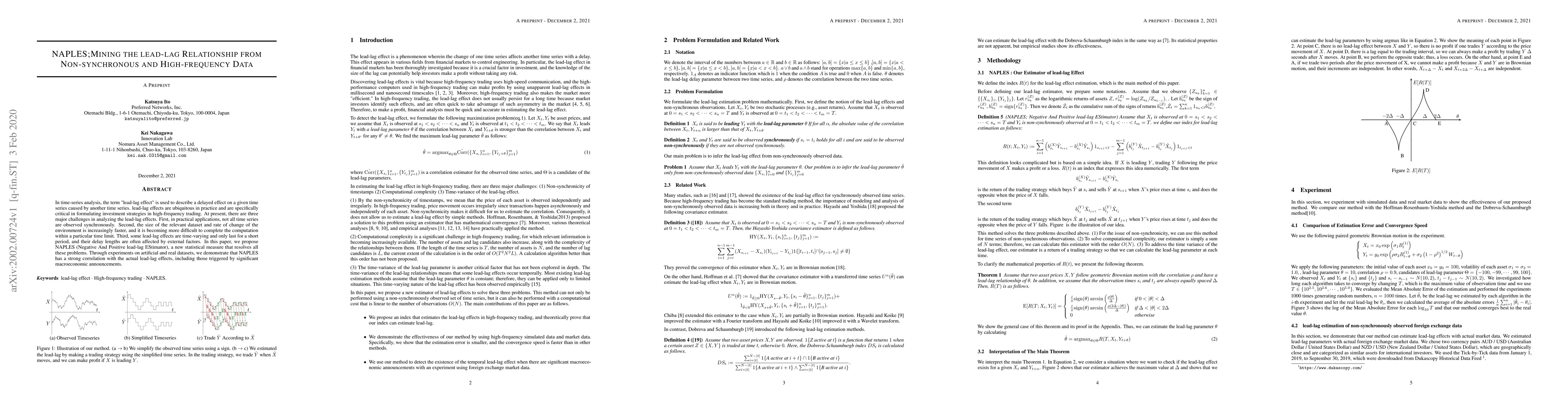

In time-series analysis, the term "lead-lag effect" is used to describe a delayed effect on a given time series caused by another time series. lead-lag effects are ubiquitous in practice and are spe...

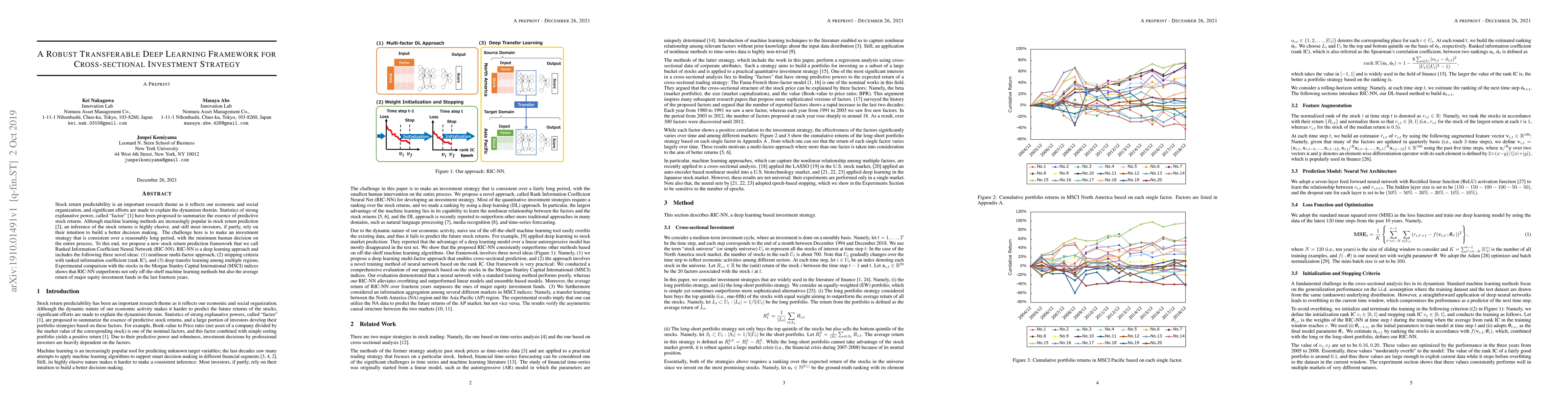

Stock return predictability is an important research theme as it reflects our economic and social organization, and significant efforts are made to explain the dynamism therein. Statistics of strong...

We propose to represent a return model and risk model in a unified manner with deep learning, which is a representative model that can express a nonlinear relationship. Although deep learning perfor...

The AI traders in financial markets have sparked significant interest in their effects on price formation mechanisms and market volatility, raising important questions for market stability and regulat...

This study aims to evaluate the sentiment of financial texts using large language models~(LLMs) and to empirically determine whether LLMs exhibit company-specific biases in sentiment analysis. Specifi...

Accurately forecasting central bank policy decisions, particularly those of the Federal Open Market Committee(FOMC) has become increasingly important amid heightened economic uncertainty. While prior ...

Modeling time series with long- or short-memory characteristics is a fundamental challenge in many scientific and engineering domains. While fractional Brownian motion has been widely used as a noise ...

Financial statement auditing is conducted under a risk-based evidence approach to obtain reasonable assurance. In practice, auditors often perform additional sampling or related procedures when an ini...

Financial decision-making tasks such as stock recommendation and portfolio allocation typically estimate future return and risk and then select trades or allocations for an investor, and the chosen op...