The chain-ladder (CL) method is the most widely used claims reserving technique in non-life insurance. This manuscript introduces a novel approach to computing the CL reserves based on a fundamental restructuring of the data utilization for the CL prediction procedure. Instead of rolling forward the cumulative claims with estimated CL factors, we estimate multi-period factors that project the latest observations directly to the ultimate claims. This alternative perspective on CL reserving creates a natural pathway for the application of machine learning techniques to individual claims reserving. As a proof of concept, we present a small-scale real data application employing neural networks for individual claims reserving.

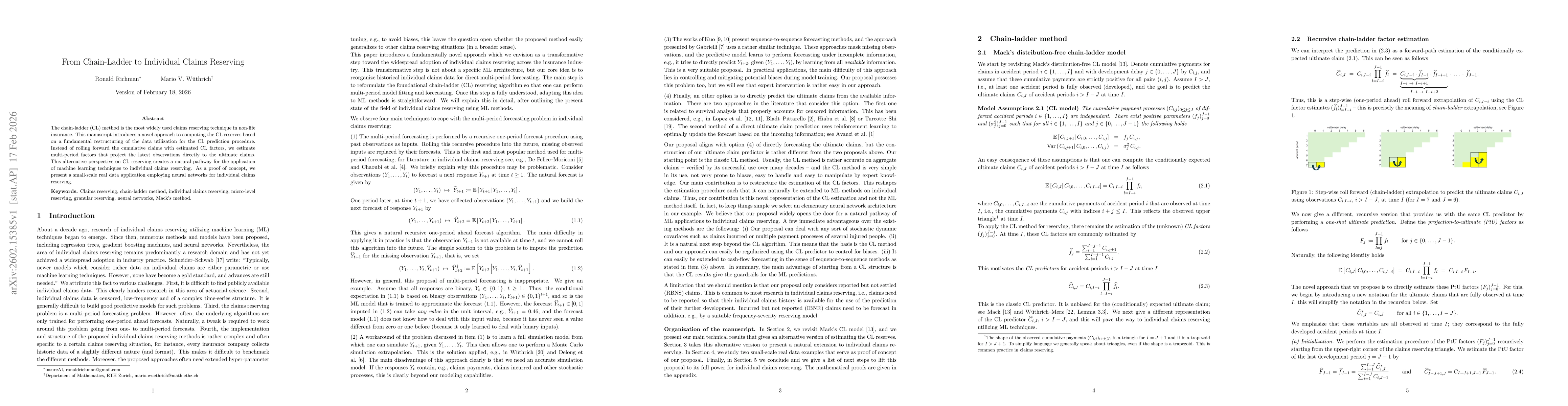

Discussion 0