01

MethodologyHow they did it

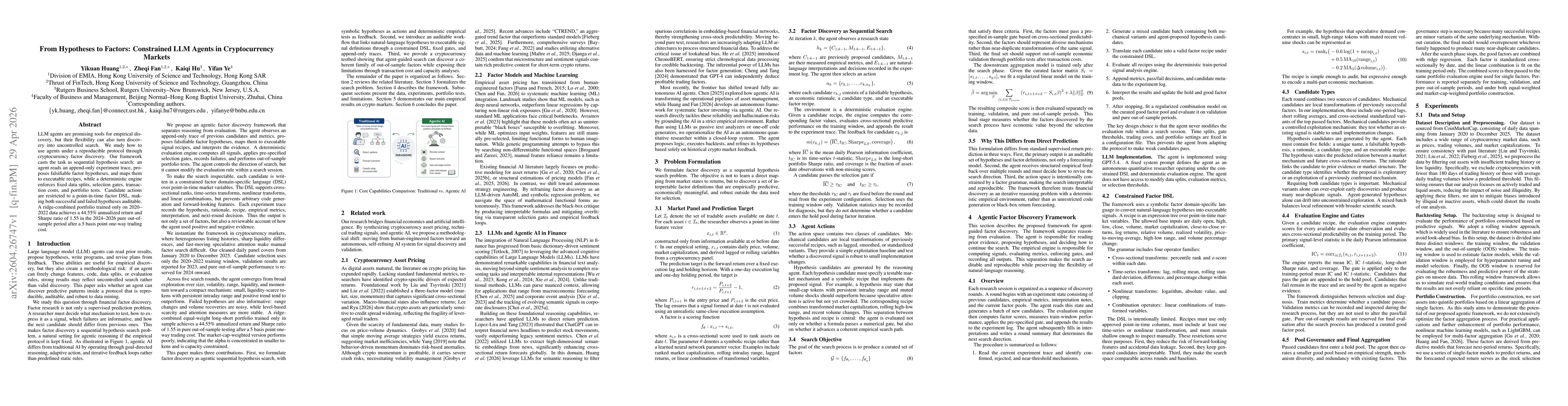

We formalize factor discovery as a constrained, agentic sequential hypothesis search where an LLM reads an append-only experiment trace, proposes falsifiable factor hypotheses, and maps them to executable, point-in-time factor DSL recipes evaluated by a deterministic, fixed-data-splits engine with auditable evaluation.

Discussion 0