Academic Profile

Statistics

Similar Authors

Papers on arXiv

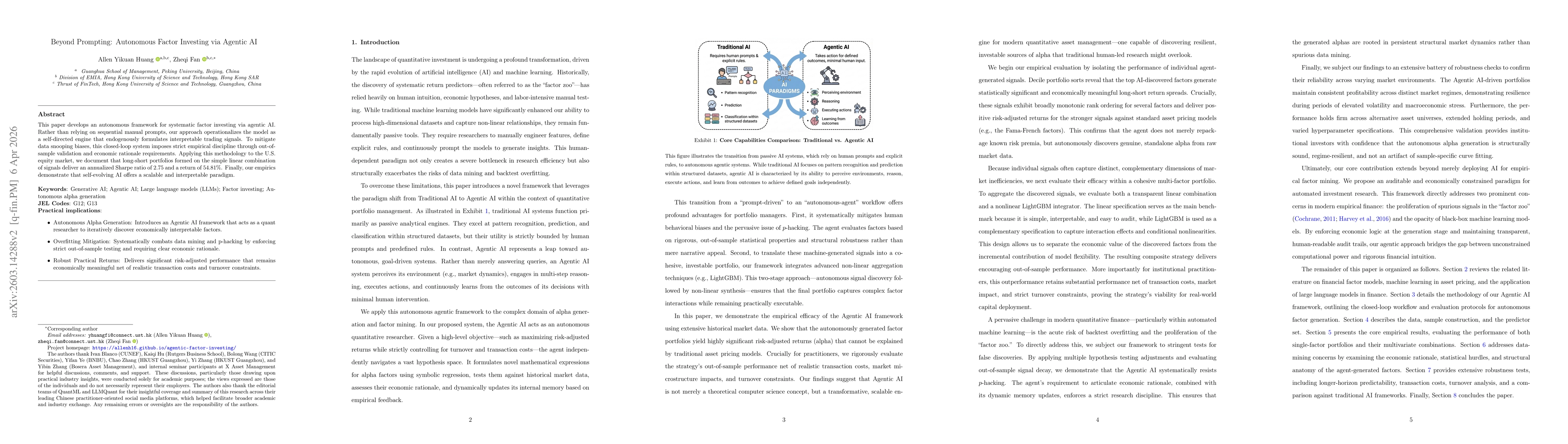

This paper develops an autonomous framework for systematic factor investing via agentic AI. Rather than relying on sequential manual prompts, our approach operationalizes the model as a self-directed ...

We examine whether model-based spot volatility estimators extracted from traded options data enhance the predictive power of the Heterogeneous Autoregressive (HAR) model for realized volatility. Speci...

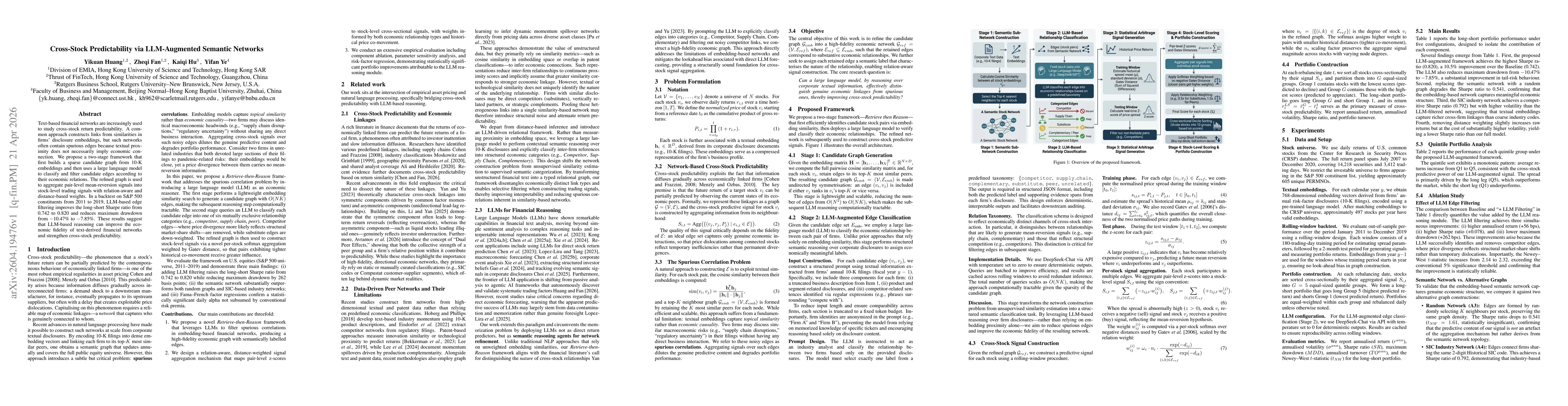

Text-based financial networks are increasingly used to study cross-stock return predictability. A common approach constructs links from similarities in firms' disclosure embeddings, but such networks ...

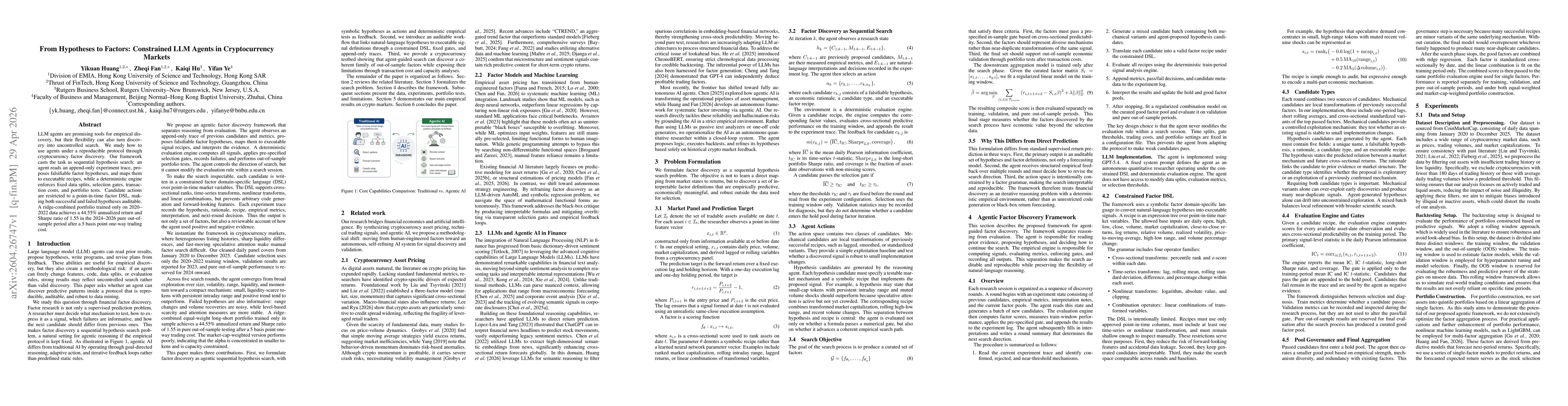

LLM agents are promising tools for empirical discovery, but their flexibility can also turn discovery into uncontrolled search. We study how to use agents under a reproducible protocol through cryptoc...