Cross-Stock Predictability via LLM-Augmented Semantic Networks

Publication

Metrics

Paper Preview

Abstract

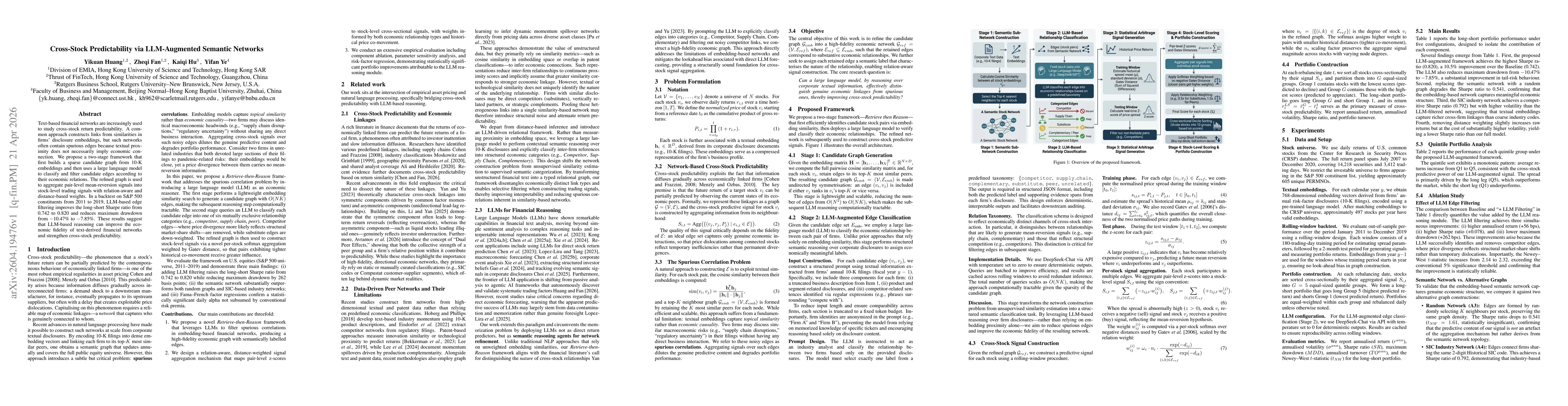

Text-based financial networks are increasingly used to study cross-stock return predictability. A common approach constructs links from similarities in firms' disclosure embeddings, but such networks often contain spurious edges because textual proximity does not necessarily imply economic connection. We propose a two-stage framework that first builds a sparse candidate graph from 10-K embeddings and then uses a large language model to classify and filter candidate edges according to their economic relations. The refined graph is used to aggregate pair-level mean-reversion signals into stock-level trading signals with relation-aware and distance-based weights. In a backtest on S&P 500 constituents from 2011 to 2019, LLM-based edge filtering improves the long-short Sharpe ratio from 0.742 to 0.820 and reduces maximum drawdown from $-$10.47% to $-$7.85%. These results suggest that LLM-based reasoning can improve the economic fidelity of text-derived financial networks and strengthen cross-stock predictability.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0