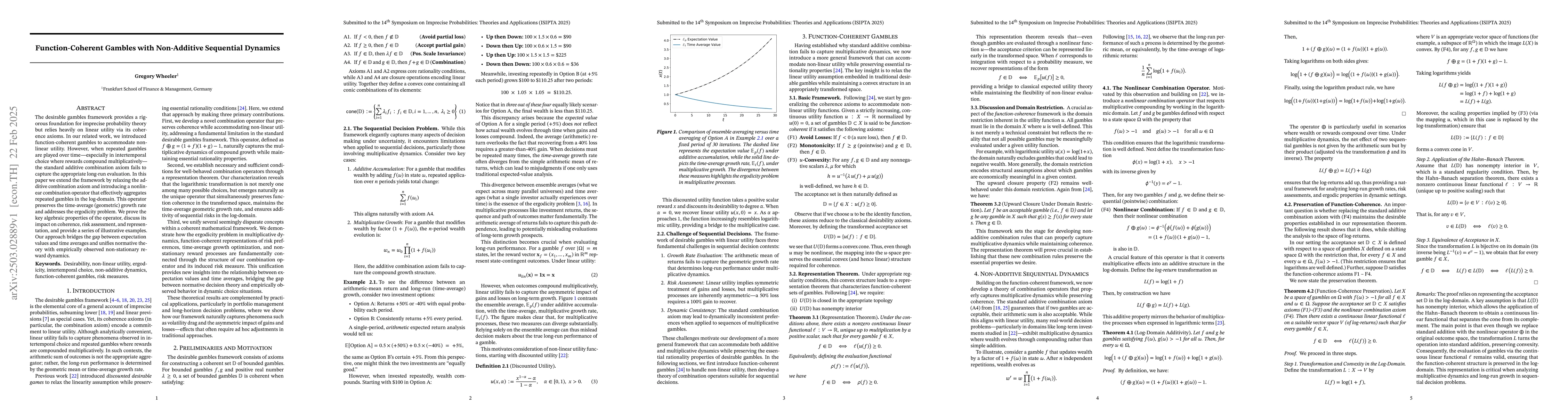

The desirable gambles framework provides a rigorous foundation for imprecise

probability theory but relies heavily on linear utility via its coherence

axioms. In our related work, we introduced function-coherent gambles to

accommodate non-linear utility. However, when repeated gambles are played over

time -- especially in intertemporal choice where rewards compound

multiplicatively -- the standard additive combination axiom fails to capture

the appropriate long-run evaluation. In this paper we extend the framework by

relaxing the additive combination axiom and introducing a nonlinear combination

operator that effectively aggregates repeated gambles in the log-domain. This

operator preserves the time-average (geometric) growth rate and addresses the

ergodicity problem. We prove the key algebraic properties of the operator,

discuss its impact on coherence, risk assessment, and representation, and

provide a series of illustrative examples. Our approach bridges the gap between

expectation values and time averages and unifies normative theory with

empirically observed non-stationary reward dynamics.

Discussion 0