Generalized Linear Model for Gamma Distributed Variables via Elastic Net Regularization

Publication

Metrics

AI Quick Summary

This paper develops an elastic net regularization method for Generalized Linear Models (GLM) for Gamma distributed variables, introducing an efficient algorithm to address the computational challenges of model selection. The proposed glmGammaNet model is implemented in an R package and evaluated through simulation studies.

Paper Preview

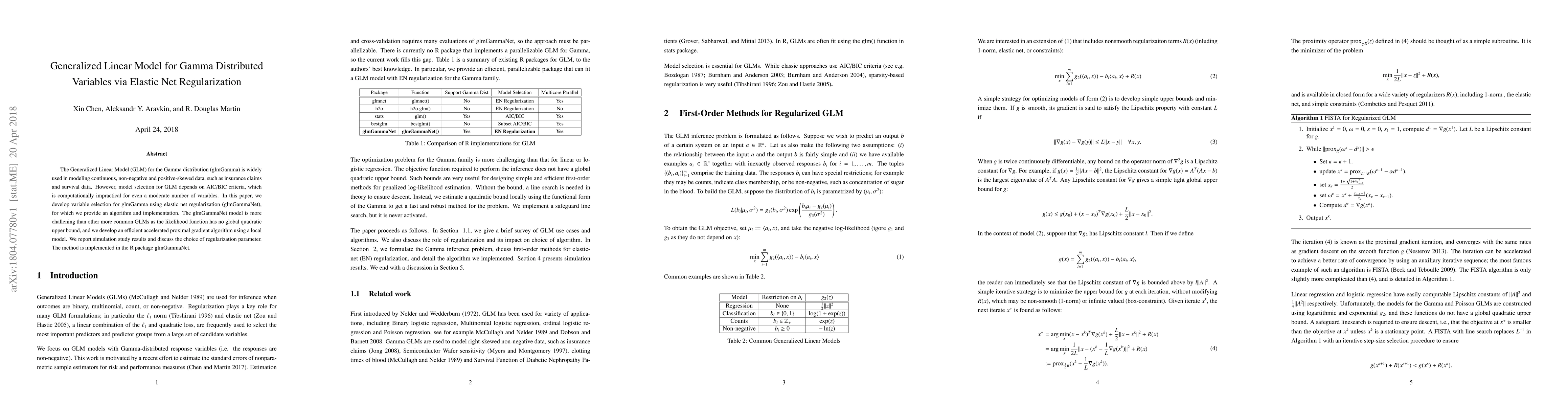

Abstract

The Generalized Linear Model (GLM) for the Gamma distribution (glmGamma) is widely used in modeling continuous, non-negative and positive-skewed data, such as insurance claims and survival data. However, model selection for GLM depends on AIC/BIC criteria, which is computationally impractical for even a moderate number of variables. In this paper, we develop variable selection for glmGamma using elastic net regularization (glmGammaNet), for which we provide an algorithm and implementation. The glmGammaNet model is more challening than other more common GLMs as the likelihood function has no global quadratic upper bound, and we develop an efficient accelerated proximal gradient algorithm using a local model. We report simulation study results and discuss the choice of regularization parameter. The method is implemented in the R package glmGammaNet.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0