Generation of synthetic financial time series by diffusion models

Publication

Metrics

AI Quick Summary

The paper proposes using denoising diffusion probabilistic models (DDPMs) to generate synthetic financial time series, addressing challenges posed by stylized facts. It utilizes wavelet transformation to convert time series data into images, allowing DDPMs to generate realistic synthetic time series that retain these statistical properties.

Paper Preview

Abstract

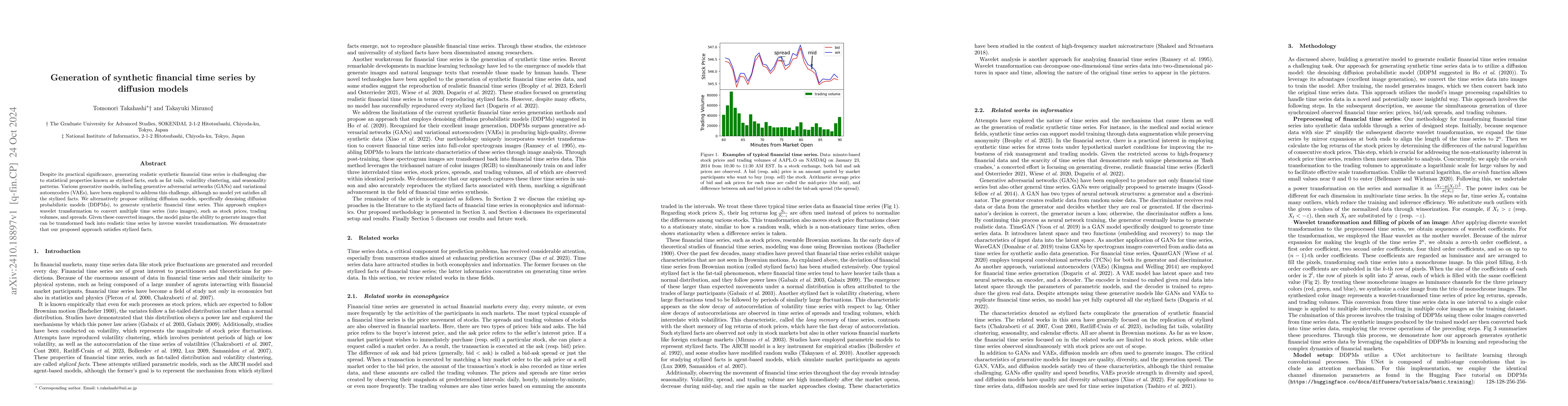

Despite its practical significance, generating realistic synthetic financial time series is challenging due to statistical properties known as stylized facts, such as fat tails, volatility clustering, and seasonality patterns. Various generative models, including generative adversarial networks (GANs) and variational autoencoders (VAEs), have been employed to address this challenge, although no model yet satisfies all the stylized facts. We alternatively propose utilizing diffusion models, specifically denoising diffusion probabilistic models (DDPMs), to generate synthetic financial time series. This approach employs wavelet transformation to convert multiple time series (into images), such as stock prices, trading volumes, and spreads. Given these converted images, the model gains the ability to generate images that can be transformed back into realistic time series by inverse wavelet transformation. We demonstrate that our proposed approach satisfies stylized facts.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0