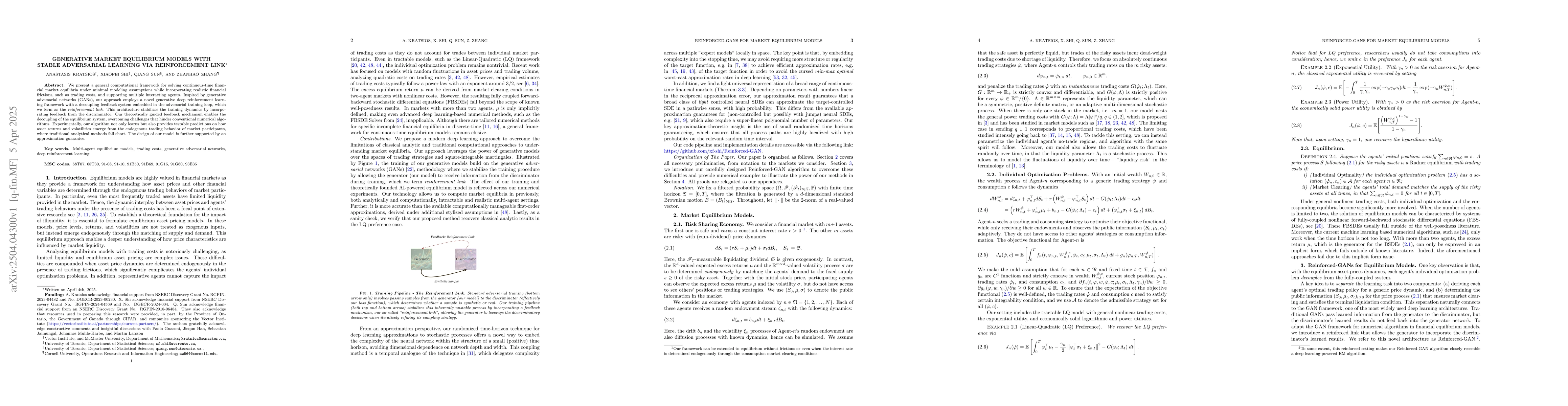

We present a general computational framework for solving continuous-time

financial market equilibria under minimal modeling assumptions while

incorporating realistic financial frictions, such as trading costs, and

supporting multiple interacting agents. Inspired by generative adversarial

networks (GANs), our approach employs a novel generative deep reinforcement

learning framework with a decoupling feedback system embedded in the

adversarial training loop, which we term as the \emph{reinforcement link}. This

architecture stabilizes the training dynamics by incorporating feedback from

the discriminator. Our theoretically guided feedback mechanism enables the

decoupling of the equilibrium system, overcoming challenges that hinder

conventional numerical algorithms. Experimentally, our algorithm not only

learns but also provides testable predictions on how asset returns and

volatilities emerge from the endogenous trading behavior of market

participants, where traditional analytical methods fall short. The design of

our model is further supported by an approximation guarantee.

Discussion 0