Hindsight Preference Optimization for Financial Time Series Advisory

Publication

Metrics

AI Quick Summary

The paper introduces Hindsight Preference Optimization (HPO), a method that uses past outcomes to rank advisory options generated by language models, aligning recommendations with complex, non-scalar quality criteria. Applying HPO to vision-language model–based forecasts of S&P 500 data, a 4B model outperforms a 235B teacher in both predictive accuracy and the usefulness of its investment advice.

Paper Preview

Abstract

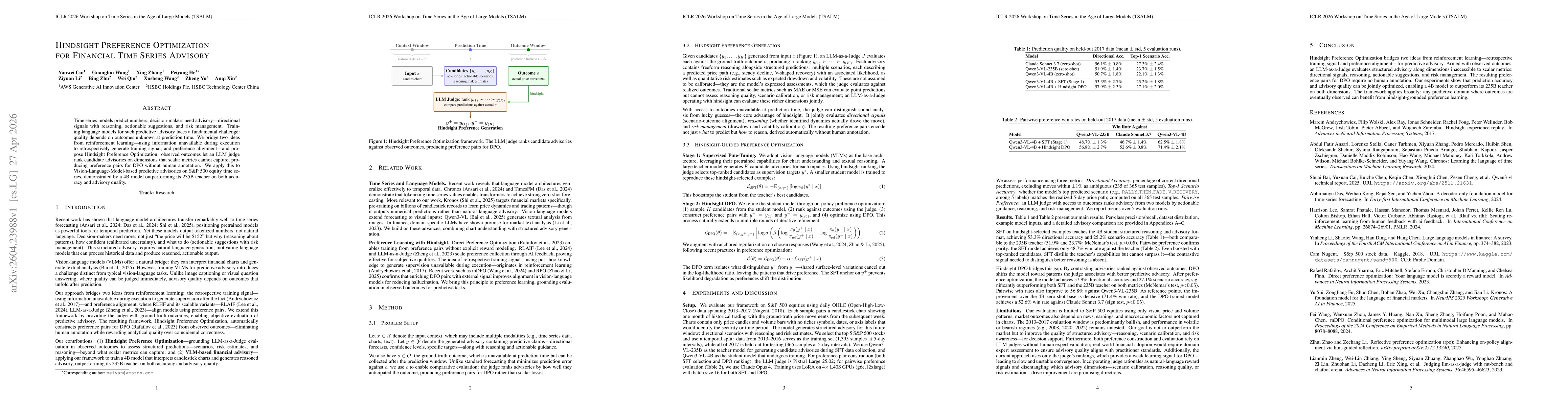

Time series models predict numbers; decision-makers need advisory -- directional signals with reasoning, actionable suggestions, and risk management. Training language models for such predictive advisory faces a fundamental challenge: quality depends on outcomes unknown at prediction time. We bridge two ideas from reinforcement learning -- using information unavailable during execution to retrospectively generate training signal, and preference alignment -- and propose Hindsight Preference Optimization: observed outcomes let an LLM judge rank candidate advisories on dimensions that scalar metrics cannot capture, producing preference pairs for DPO without human annotation. We apply this to Vision-Language-Model-based predictive advisories on S&P 500 equity time series, demonstrated by a 4B model outperforming its 235B teacher on both accuracy and advisory quality.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0