Improved Churn Causal Analysis Through Restrained High-Dimensional Feature Space Effects in Financial Institutions

Publication

Metrics

AI Quick Summary

This study develops a framework for predicting customer churn in financial institutions using advanced algorithms like ensemble ANN and SMOTE, addressing high-dimensional data challenges. Causal analysis identifies key factors like super guarantee contributions and account balances as significant predictors for customer churn, achieving 86% accuracy.

Paper Preview

Abstract

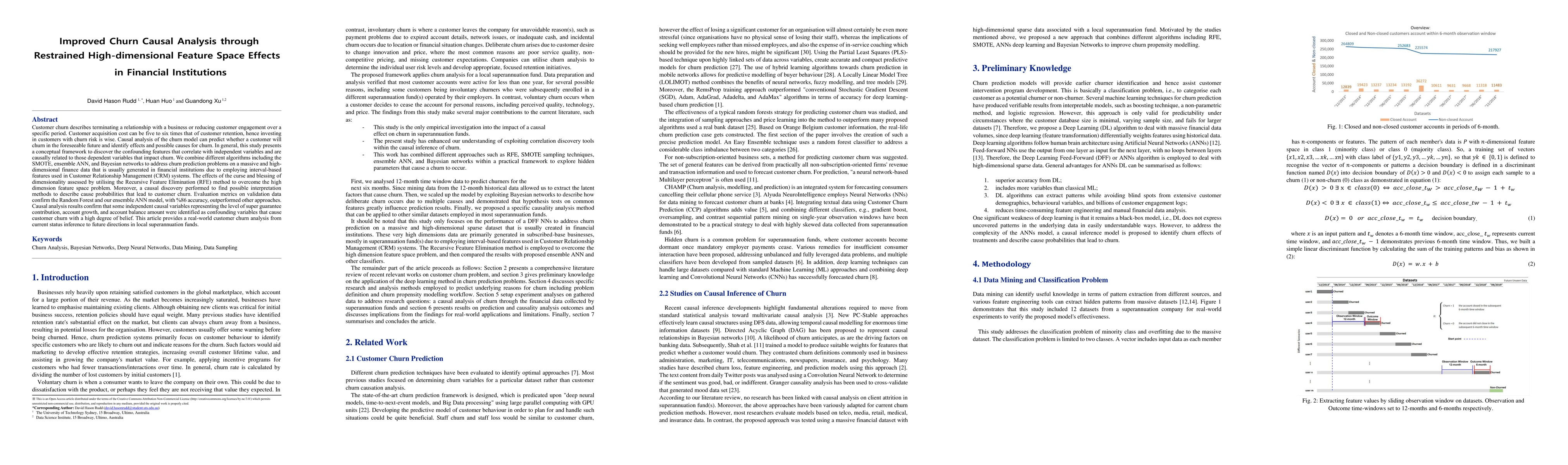

Customer churn describes terminating a relationship with a business or reducing customer engagement over a specific period. Customer acquisition cost can be five to six times that of customer retention, hence investing in customers with churn risk is wise. Causal analysis of the churn model can predict whether a customer will churn in the foreseeable future and identify effects and possible causes for churn. In general, this study presents a conceptual framework to discover the confounding features that correlate with independent variables and are causally related to those dependent variables that impact churn. We combine different algorithms including the SMOTE, ensemble ANN, and Bayesian networks to address churn prediction problems on a massive and high-dimensional finance data that is usually generated in financial institutions due to employing interval-based features used in Customer Relationship Management systems. The effects of the curse and blessing of dimensionality assessed by utilising the Recursive Feature Elimination method to overcome the high dimension feature space problem. Moreover, a causal discovery performed to find possible interpretation methods to describe cause probabilities that lead to customer churn. Evaluation metrics on validation data confirm the random forest and our ensemble ANN model, with %86 accuracy, outperformed other approaches. Causal analysis results confirm that some independent causal variables representing the level of super guarantee contribution, account growth, and account balance amount were identified as confounding variables that cause customer churn with a high degree of belief. This article provides a real-world customer churn analysis from current status inference to future directions in local superannuation funds.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0