Publication

Metrics

Paper Preview

Abstract

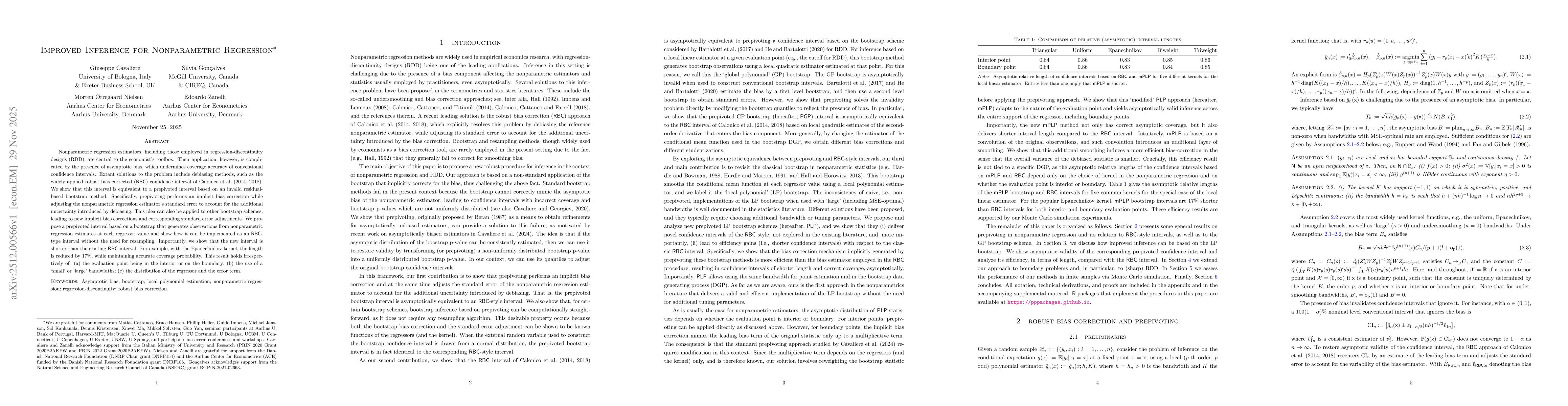

Nonparametric regression estimators, including those employed in regression-discontinuity designs (RDD), are central to the economist's toolbox. Their application, however, is complicated by the presence of asymptotic bias, which undermines coverage accuracy of conventional confidence intervals. Extant solutions to the problem include debiasing methods, such as the widely applied robust bias-corrected (RBC) confidence interval of Calonico et al. (2014, 2018). We show that this interval is equivalent to a prepivoted interval based on an invalid residual-based bootstrap method. Specifically, prepivoting performs an implicit bias correction while adjusting the nonparametric regression estimator's standard error to account for the additional uncertainty introduced by debiasing. This idea can also be applied to other bootstrap schemes, leading to new implicit bias corrections and corresponding standard error adjustments. We propose a prepivoted interval based on a bootstrap that generates observations from nonparametric regression estimates at each regressor value and show how it can be implemented as an RBC-type interval without the need for resampling. Importantly, we show that the new interval is shorter than the existing RBC interval. For example, with the Epanechnikov kernel, the length is reduced by 17%, while maintaining accurate coverage probability. This result holds irrespectively of: (a) the evaluation point being in the interior or on the boundary; (b) the use of a 'small' or 'large' bandwidths; (c) the distribution of the regressor and the error term.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0