Academic Profile

Statistics

Similar Authors

Papers on arXiv

Engle and Russell (1998, Econometrica, 66:1127--1162) apply results from the GARCH literature to prove consistency and asymptotic normality of the (exponential) QMLE for the generalized autoregressi...

When proxies (external instruments) used to identify target structural shocks are weak, inference in proxy-SVARs (SVAR-IVs) is nonstandard and the construction of asymptotically valid confidence set...

We propose a factor network autoregressive (FNAR) model for time series with complex network structures. The coefficients of the model reflect many different types of connections between economic ag...

We establish new results for estimation and inference in financial durations models, where events are observed over a given time span, such as a trading day, or a week. For the classical autoregress...

We consider bootstrap inference for estimators which are (asymptotically) biased. We show that, even when the bias term cannot be consistently estimated, valid inference can be obtained by proper im...

In this paper we propose a new time-varying econometric model, called Time-Varying Poisson AutoRegressive with eXogenous covariates (TV-PARX), suited to model and forecast time series of counts. {We...

Standard methods, such as sequential procedures based on Johansen's (pseudo-)likelihood ratio (PLR) test, for determining the co-integration rank of a vector autoregressive (VAR) system of variables...

We study inference on the common stochastic trends in a non-stationary, $N$-variate time series $y_{t}$, in the possible presence of heavy tails. We propose a novel methodology which does not requir...

Score tests have the advantage of requiring estimation alone of the model restricted by the null hypothesis, which often is much simpler than models defined under the alternative hypothesis. This is...

This paper develops tests for the correct specification of the conditional variance function in GARCH models when the true parameter may lie on the boundary of the parameter space. The test statisti...

Inference and testing in general point process models such as the Hawkes model is predominantly based on asymptotic approximations for likelihood-based estimators and tests. As an alternative, and t...

In this paper we investigate how the bootstrap can be applied to time series regressions when the volatility of the innovations is random and non-stationary. The volatility of many economic and fina...

Asymptotic bootstrap validity is usually understood as consistency of the distribution of a bootstrap statistic, conditional on the data, for the unconditional limit distribution of a statistic of i...

We consider bootstrap inference in predictive (or Granger-causality) regressions when the parameter of interest may lie on the boundary of the parameter space, here defined by means of a smooth inequa...

Integrated autoregressive conditional duration (ACD) models serve as natural counterparts to the well-known integrated GARCH models used for financial returns. However, despite their resemblance, asym...

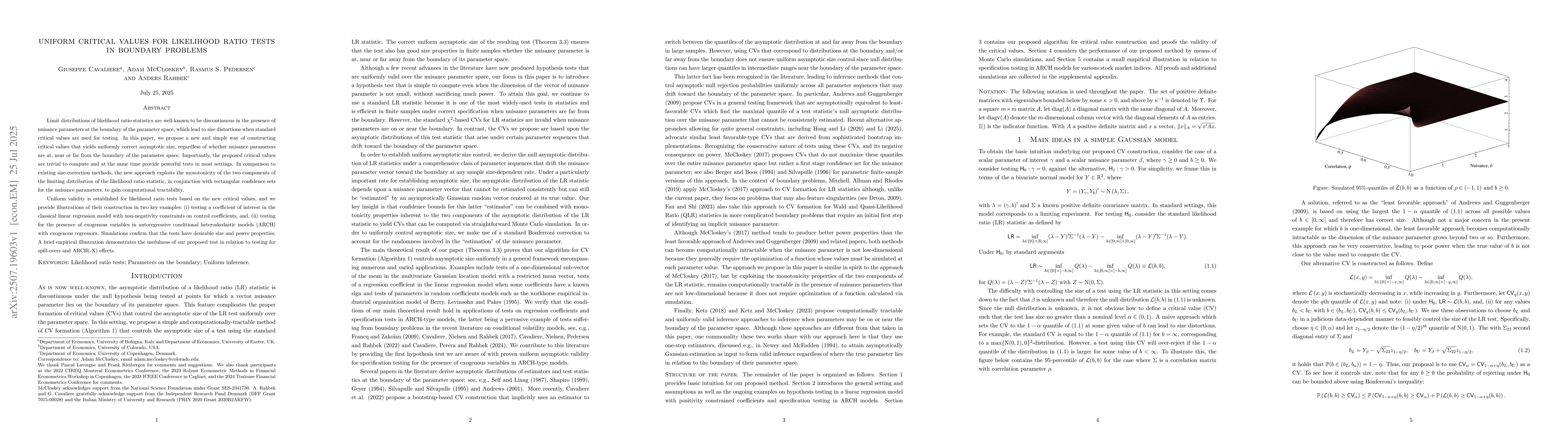

Limit distributions of likelihood ratio statistics are well-known to be discontinuous in the presence of nuisance parameters at the boundary of the parameter space, which lead to size distortions when...

Violation of the assumptions underlying classical (Gaussian) limit theory frequently leads to unreliable statistical inference. This paper shows the novel result that the bootstrap can detect such vio...

Nonparametric regression estimators, including those employed in regression-discontinuity designs (RDD), are central to the economist's toolbox. Their application, however, is complicated by the prese...