Accurate prediction of financial market volatility is critical for risk

management, derivatives pricing, and investment strategy. In this study, we

propose a multitude of regime-switching methods to improve the prediction of

S&P 500 volatility by capturing structural changes in the market across time.

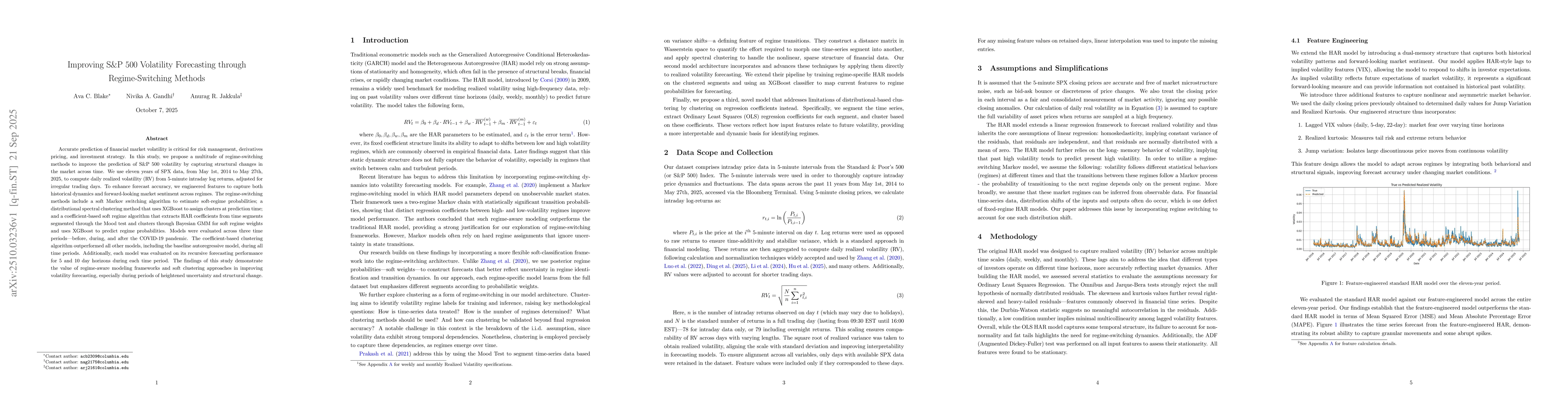

We use eleven years of SPX data, from May 1st, 2014 to May 27th, 2025, to

compute daily realized volatility (RV) from 5-minute intraday log returns,

adjusted for irregular trading days. To enhance forecast accuracy, we

engineered features to capture both historical dynamics and forward-looking

market sentiment across regimes. The regime-switching methods include a soft

Markov switching algorithm to estimate soft-regime probabilities, a

distributional spectral clustering method that uses XGBoost to assign clusters

at prediction time, and a coefficient-based soft regime algorithm that extracts

HAR coefficients from time segments segmented through the Mood test and

clusters through Bayesian GMM for soft regime weights, using XGBoost to predict

regime probabilities. Models were evaluated across three time periods--before,

during, and after the COVID-19 pandemic. The coefficient-based clustering

algorithm outperformed all other models, including the baseline autoregressive

model, during all time periods. Additionally, each model was evaluated on its

recursive forecasting performance for 5- and 10-day horizons during each time

period. The findings of this study demonstrate the value of regime-aware

modeling frameworks and soft clustering approaches in improving volatility

forecasting, especially during periods of heightened uncertainty and structural

change.

Discussion 0