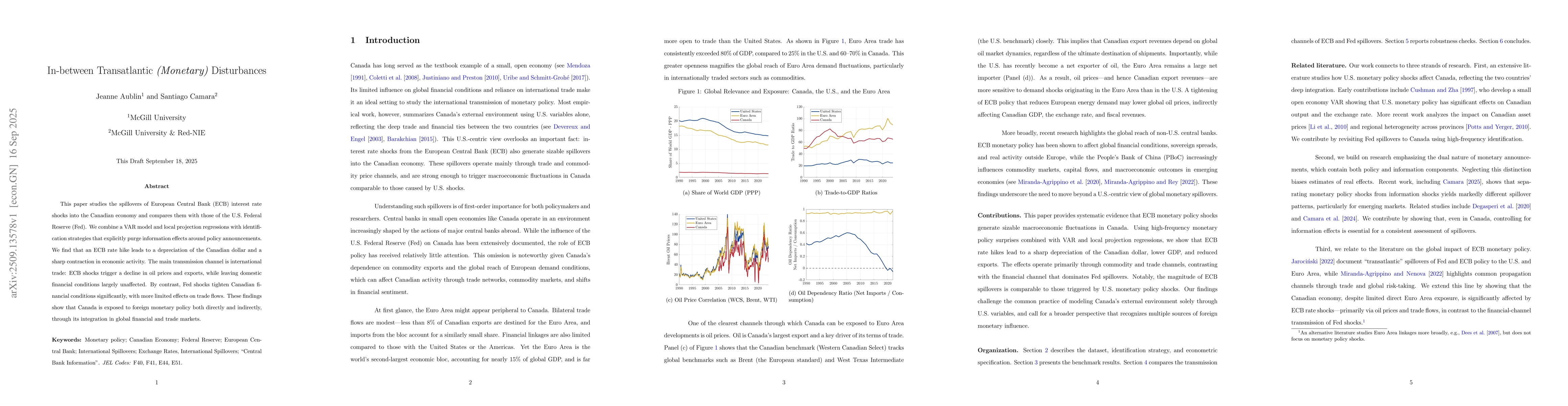

This paper studies the spillovers of European Central Bank (ECB) interest

rate shocks into the Canadian economy and compares them with those of the U.S.

Federal Reserve (Fed). We combine a VAR model and local projection regressions

with identification strategies that explicitly purge information effects around

policy announcements. We find that an ECB rate hike leads to a depreciation of

the Canadian dollar and a sharp contraction in economic activity. The main

transmission channel is international trade: ECB shocks trigger a decline in

oil prices and exports, while leaving domestic financial conditions largely

unaffected. By contrast, Fed shocks tighten Canadian financial conditions

significantly, with more limited effects on trade flows. These findings show

that Canada is exposed to foreign monetary policy both directly and indirectly,

through its integration in global financial and trade markets.

Discussion 0