Inference for Extremal Conditional Quantile Models, with an Application to Market and Birthweight Risks

Publication

Metrics

AI Quick Summary

This paper develops inference methods for extremal conditional quantile models using extreme value approximations for self-normalized quantile regression statistics. It demonstrates the utility of these methods through empirical analyses of extreme stock return fluctuations and low birthweight percentiles in infants.

Paper Preview

Abstract

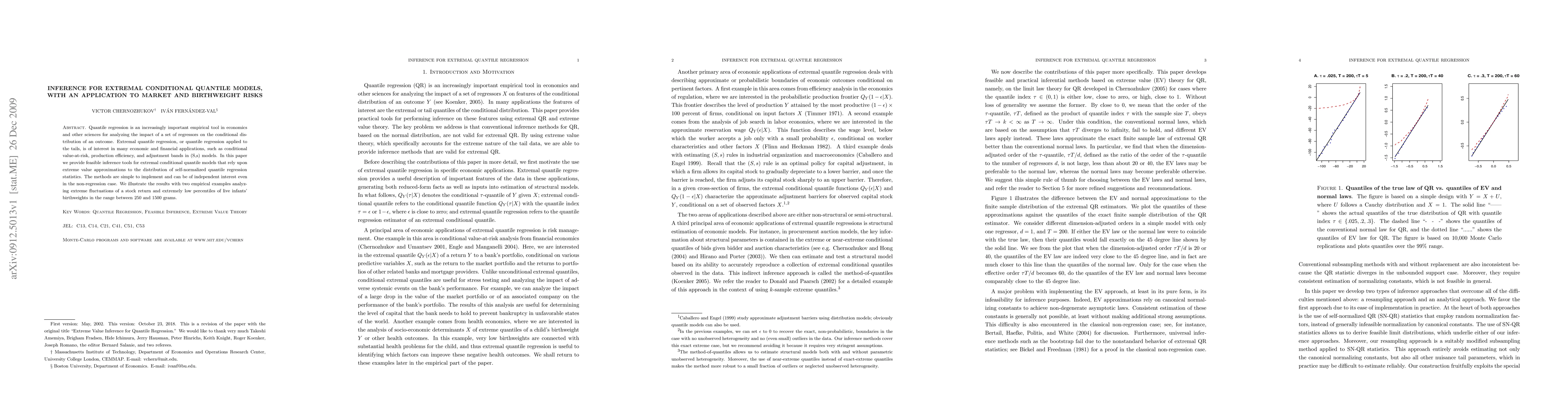

Quantile regression is an increasingly important empirical tool in economics and other sciences for analyzing the impact of a set of regressors on the conditional distribution of an outcome. Extremal quantile regression, or quantile regression applied to the tails, is of interest in many economic and financial applications, such as conditional value-at-risk, production efficiency, and adjustment bands in (S,s) models. In this paper we provide feasible inference tools for extremal conditional quantile models that rely upon extreme value approximations to the distribution of self-normalized quantile regression statistics. The methods are simple to implement and can be of independent interest even in the non-regression case. We illustrate the results with two empirical examples analyzing extreme fluctuations of a stock return and extremely low percentiles of live infants' birthweights in the range between 250 and 1500 grams.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0