Insurance Premium Prediction via Gradient Tree-Boosted Tweedie Compound Poisson Models

Publication

Metrics

AI Quick Summary

This paper proposes a gradient tree-boosting algorithm applied to Tweedie compound Poisson models for predicting insurance premiums, offering a flexible nonlinear alternative to traditional Tweedie GLMs. The method demonstrates superior prediction accuracy in simulations and real-world auto insurance data, addressing adverse selection issues.

Paper Preview

Abstract

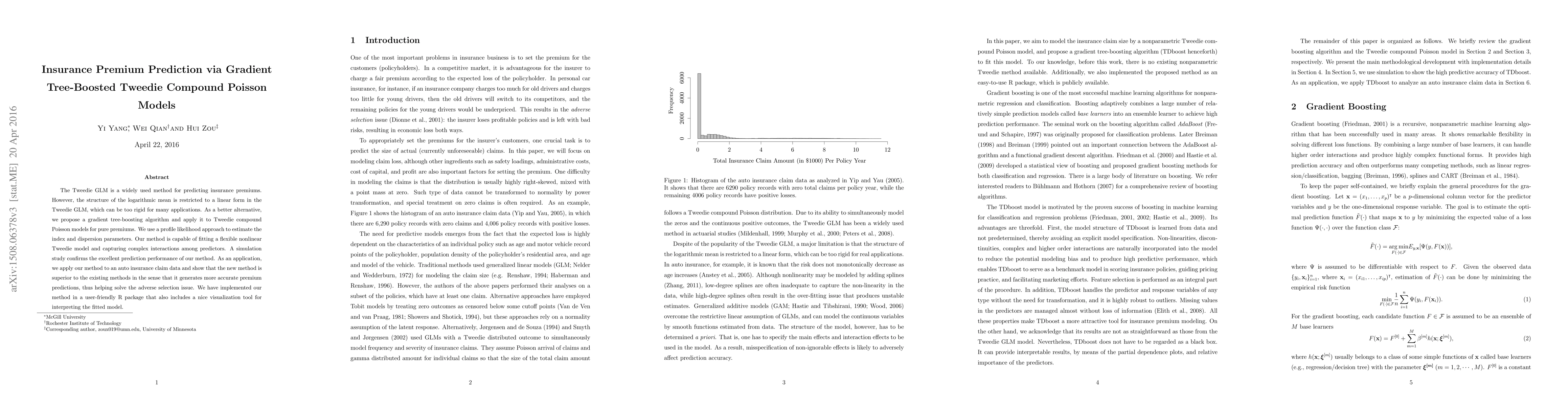

The Tweedie GLM is a widely used method for predicting insurance premiums. However, the structure of the logarithmic mean is restricted to a linear form in the Tweedie GLM, which can be too rigid for many applications. As a better alternative, we propose a gradient tree-boosting algorithm and apply it to Tweedie compound Poisson models for pure premiums. We use a profile likelihood approach to estimate the index and dispersion parameters. Our method is capable of fitting a flexible nonlinear Tweedie model and capturing complex interactions among predictors. A simulation study confirms the excellent prediction performance of our method. As an application, we apply our method to an auto insurance claim data and show that the new method is superior to the existing methods in the sense that it generates more accurate premium predictions, thus helping solve the adverse selection issue. We have implemented our method in a user-friendly R package that also includes a nice visualization tool for interpreting the fitted model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0