InvariantStock: Learning Invariant Features for Mastering the Shifting Market

Publication

Metrics

AI Quick Summary

InvariantStock introduces a learning framework to predict stock returns by acquiring invariant features across market environments, addressing distribution shifts for improved robustness. The proposed method consists of an environment-aware prediction module and an environment-agnostic module, outperforming existing methods in both prediction accuracy and handling dynamic market shifts.

Paper Preview

Abstract

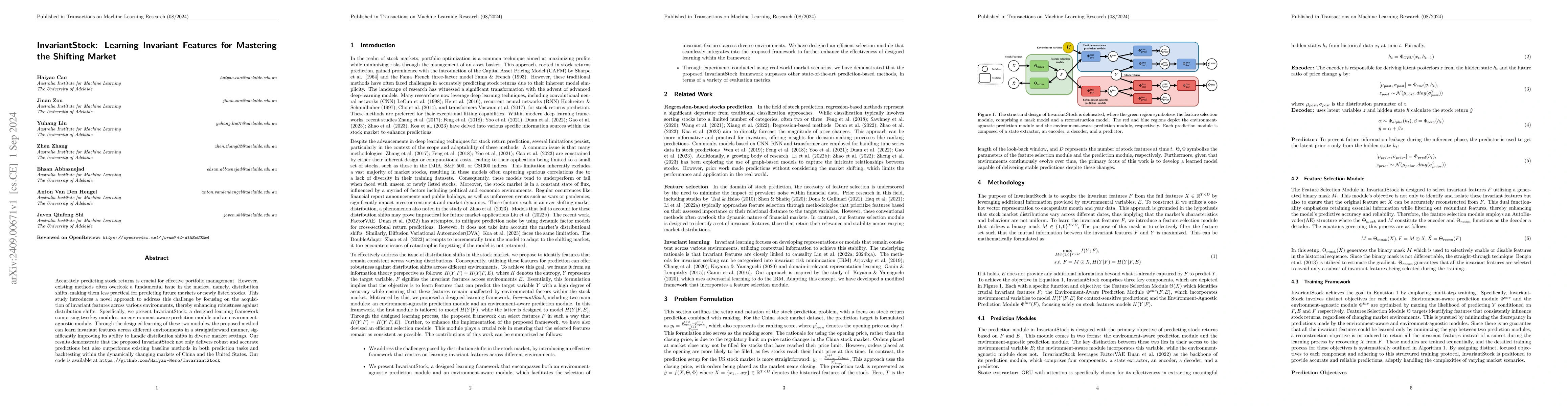

Accurately predicting stock returns is crucial for effective portfolio management. However, existing methods often overlook a fundamental issue in the market, namely, distribution shifts, making them less practical for predicting future markets or newly listed stocks. This study introduces a novel approach to address this challenge by focusing on the acquisition of invariant features across various environments, thereby enhancing robustness against distribution shifts. Specifically, we present InvariantStock, a designed learning framework comprising two key modules: an environment-aware prediction module and an environment-agnostic module. Through the designed learning of these two modules, the proposed method can learn invariant features across different environments in a straightforward manner, significantly improving its ability to handle distribution shifts in diverse market settings. Our results demonstrate that the proposed InvariantStock not only delivers robust and accurate predictions but also outperforms existing baseline methods in both prediction tasks and backtesting within the dynamically changing markets of China and the United States.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0