Publication

Metrics

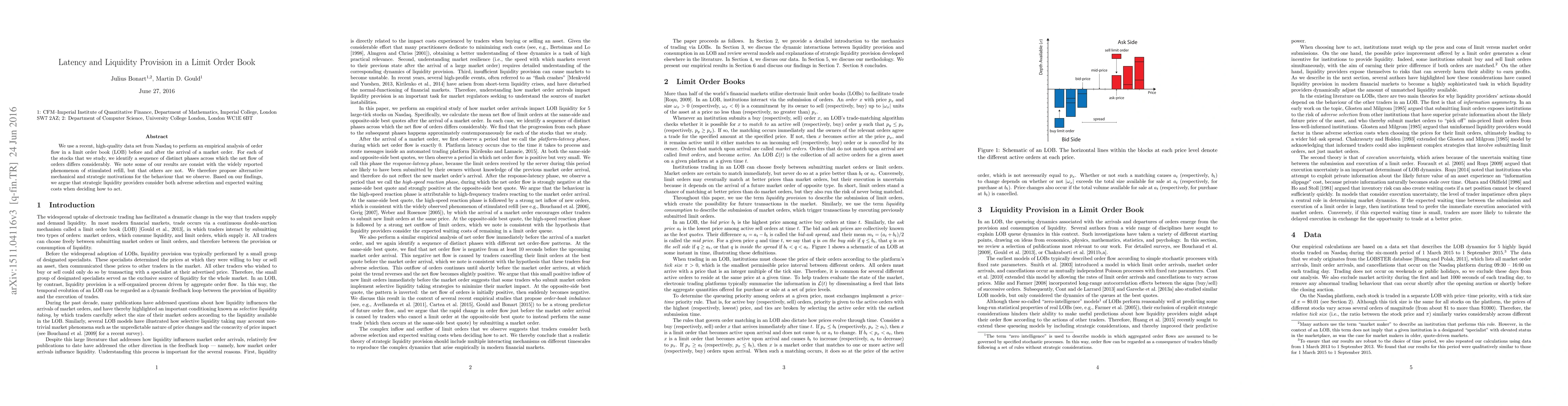

AI Quick Summary

This paper analyzes Nasdaq limit order book data to study order flow dynamics before and after market order arrivals, identifying distinct phases with varying net order flows. It proposes alternative explanations for observed behaviors beyond the traditional stimulated refill phenomenon, suggesting that liquidity providers weigh both adverse selection and waiting costs in their decisions.

Paper Preview

Abstract

We use a recent, high-quality data set from Nasdaq to perform an empirical analysis of order flow in a limit order book (LOB) before and after the arrival of a market order. For each of the stocks that we study, we identify a sequence of distinct phases across which the net flow of orders differs considerably. We note some of our results are consist with the widely reported phenomenon of stimulated refill, but that others are not. We therefore propose alternative mechanical and strategic motivations for the behaviour that we observe. Based on our findings, we argue that strategic liquidity providers consider both adverse selection and expected waiting costs when deciding how to act.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0