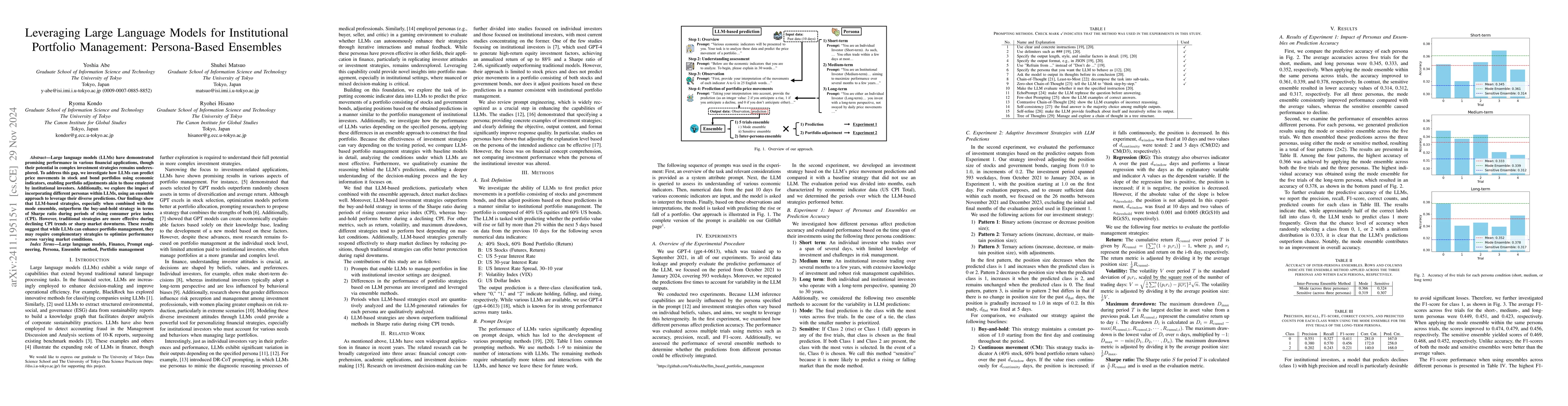

Leveraging Large Language Models for Institutional Portfolio Management: Persona-Based Ensembles

Publication

Metrics

AI Quick Summary

This paper examines the use of large language models (LLMs) for enhancing institutional portfolio management by predicting price movements using economic indicators, with an ensemble of diverse personas outperforming traditional buy-and-hold strategies during rising inflation periods. It highlights the need for hybrid approaches to optimize performance across different market conditions.

Paper Preview

Abstract

Large language models (LLMs) have demonstrated promising performance in various financial applications, though their potential in complex investment strategies remains underexplored. To address this gap, we investigate how LLMs can predict price movements in stock and bond portfolios using economic indicators, enabling portfolio adjustments akin to those employed by institutional investors. Additionally, we explore the impact of incorporating different personas within LLMs, using an ensemble approach to leverage their diverse predictions. Our findings show that LLM-based strategies, especially when combined with the mode ensemble, outperform the buy-and-hold strategy in terms of Sharpe ratio during periods of rising consumer price index (CPI). However, traditional strategies are more effective during declining CPI trends or sharp market downturns. These results suggest that while LLMs can enhance portfolio management, they may require complementary strategies to optimize performance across varying market conditions.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0