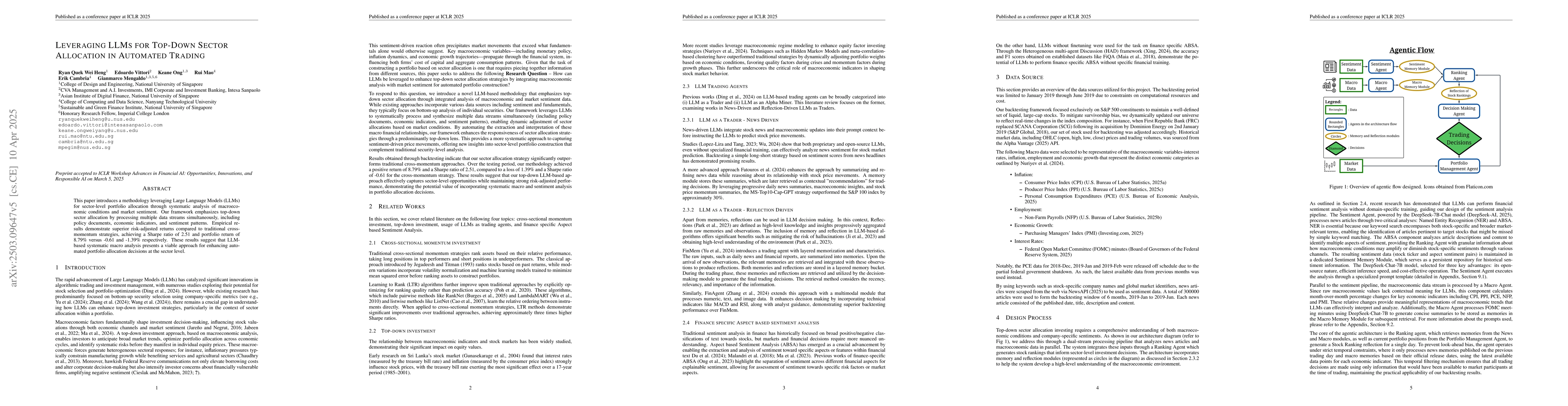

This paper introduces a methodology leveraging Large Language Models (LLMs)

for sector-level portfolio allocation through systematic analysis of

macroeconomic conditions and market sentiment. Our framework emphasizes

top-down sector allocation by processing multiple data streams simultaneously,

including policy documents, economic indicators, and sentiment patterns.

Empirical results demonstrate superior risk-adjusted returns compared to

traditional cross momentum strategies, achieving a Sharpe ratio of 2.51 and

portfolio return of 8.79% versus -0.61 and -1.39% respectively. These results

suggest that LLM-based systematic macro analysis presents a viable approach for

enhancing automated portfolio allocation decisions at the sector level.

Discussion 0