Academic Profile

Statistics

Similar Authors

Papers on arXiv

This work studies the dynamic risk management of the risk-neutral value of the potential credit losses on a portfolio of derivatives. Sensitivities-based hedging of such liability is sub-optimal bec...

In this paper, we focus on finding the optimal hedging strategy of a credit index option using reinforcement learning. We take a practical approach, where the focus is on realism i.e. discrete time,...

In this paper we show how risk-averse reinforcement learning can be used to hedge options. We apply a state-of-the-art risk-averse algorithm: Trust Region Volatility Optimization (TRVO) to a vanilla...

In real-world decision-making problems, for instance in the fields of finance, robotics or autonomous driving, keeping uncertainty under control is as important as maximizing expected returns. Risk ...

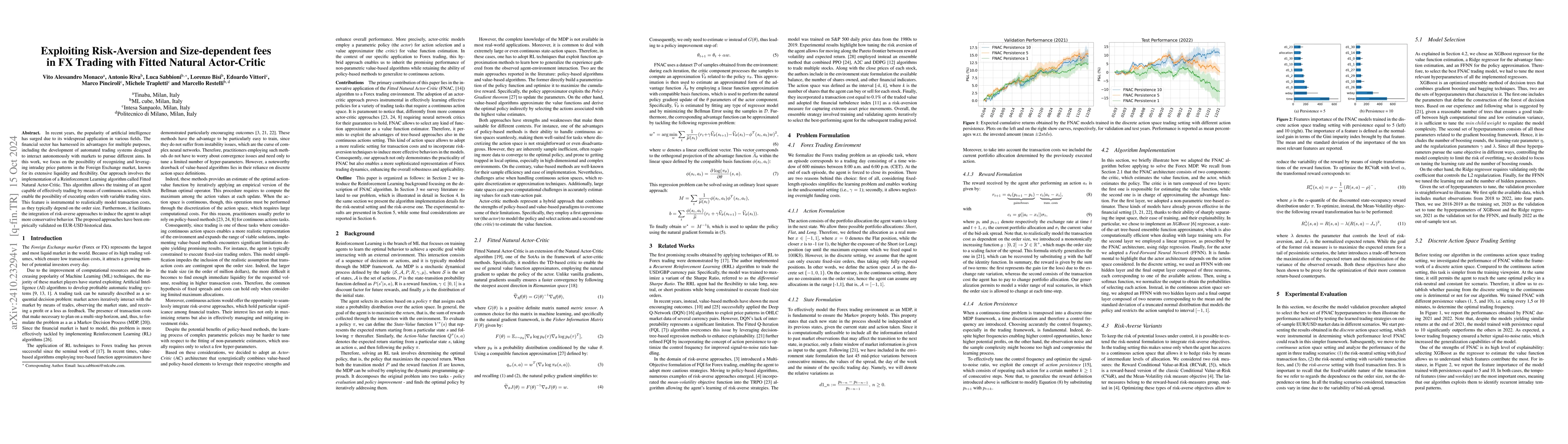

In recent years, the popularity of artificial intelligence has surged due to its widespread application in various fields. The financial sector has harnessed its advantages for multiple purposes, incl...

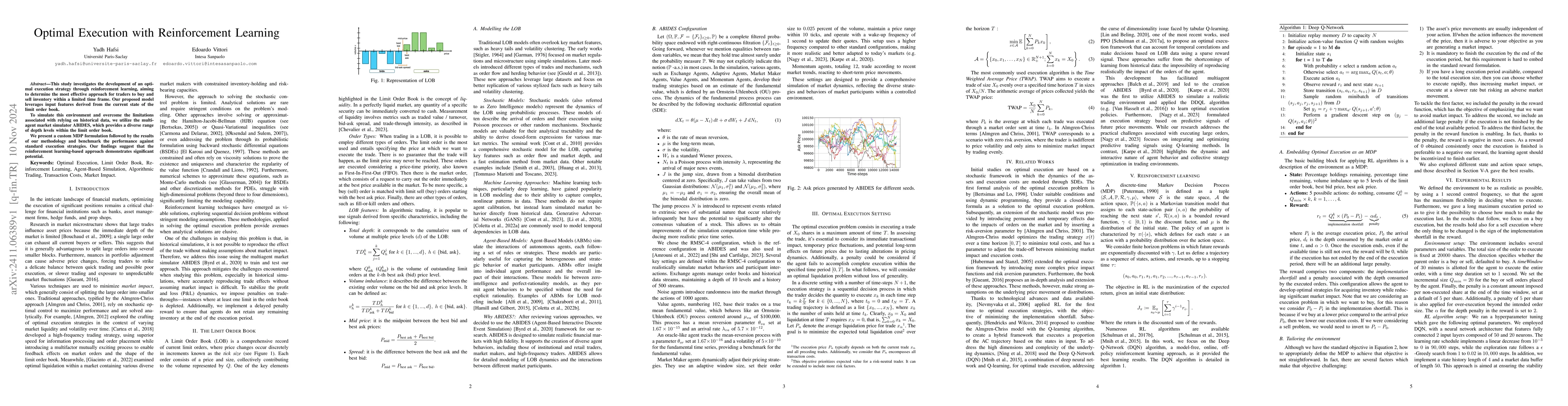

This study investigates the development of an optimal execution strategy through reinforcement learning, aiming to determine the most effective approach for traders to buy and sell inventory within a ...

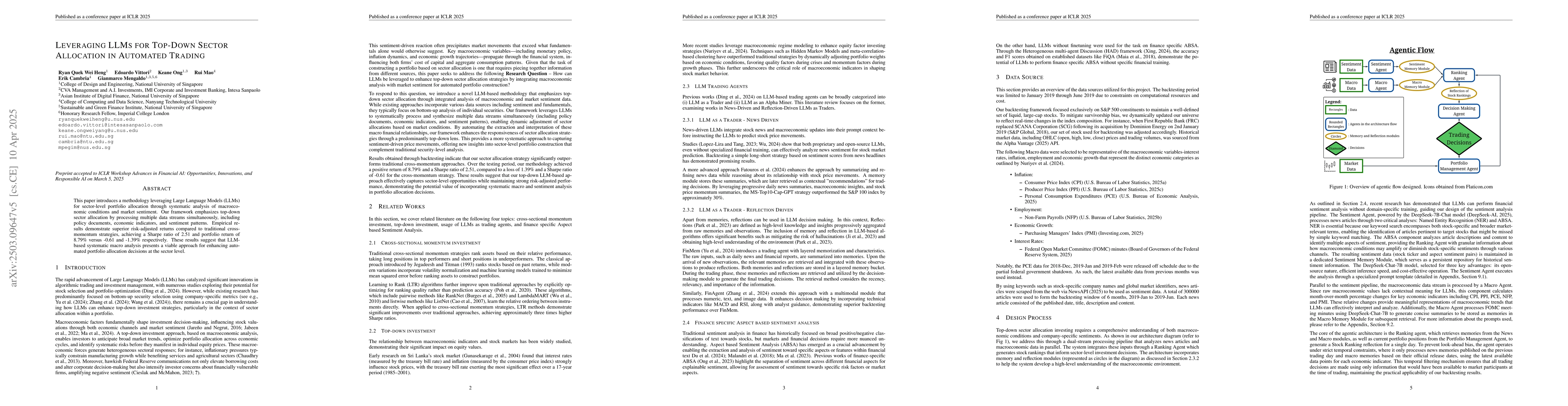

This paper introduces a methodology leveraging Large Language Models (LLMs) for sector-level portfolio allocation through systematic analysis of macroeconomic conditions and market sentiment. Our fram...

We investigate the use of Reinforcement Learning for the optimal execution of meta-orders, where the objective is to execute incrementally large orders while minimizing implementation shortfall and ma...

In finance, sequential decision problems are often faced, for which reinforcement learning (RL) emerges as a promising tool for optimisation without the need of analytical tractability. However, the o...