Publication

Metrics

AI Quick Summary

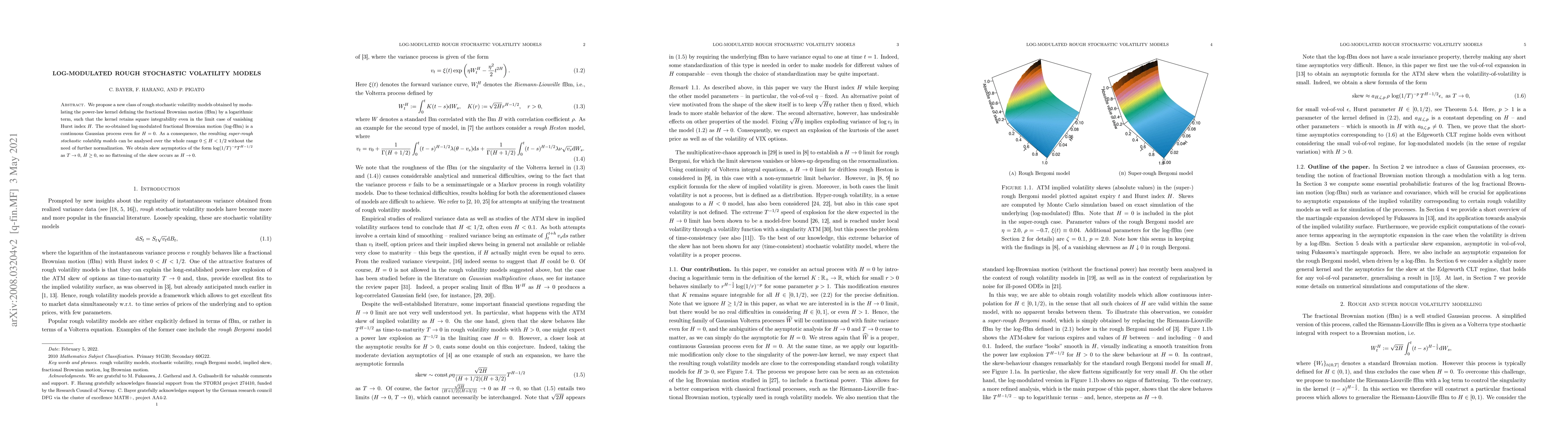

Researchers propose a new class of stochastic volatility models that retain square integrability even at zero Hurst index, enabling analysis without normalization. They also find skew asymptotics that do not flatten as the Hurst index approaches 0.

Paper Preview

Abstract

We propose a new class of rough stochastic volatility models obtained by modulating the power-law kernel defining the fractional Brownian motion (fBm) by a logarithmic term, such that the kernel retains square integrability even in the limit case of vanishing Hurst index $H$. The so-obtained log-modulated fractional Brownian motion (log-fBm) is a continuous Gaussian process even for $H = 0$. As a consequence, the resulting super-rough stochastic volatility models can be analysed over the whole range $0 \le H < 1/2$ without the need of further normalization. We obtain skew asymptotics of the form $\log(1/T)^{-p} T^{H-1/2}$ as $T\to 0$, $H \ge 0$, so no flattening of the skew occurs as $H \to 0$.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0