As markets have digitized, the number of tradable products has skyrocketed.

Algorithmically constructed portfolios of these assets now dominate public and

private markets, resulting in a combinatorial explosion of tradable assets. In

this paper, we provide a simple means to compute market clearing prices for

semi-fungible assets which have a partial ordering between them. Such assets

are increasingly found in traditional markets (bonds, commodities, ETFs),

private markets (private credit, compute markets), and in decentralized

finance. We formulate the market clearing problem as an optimization problem

over a directed acyclic graph that represents participant preferences.

Subsequently, we use convex duality to efficiently estimate market clearing

prices, which correspond to particular dual variables. We then describe

dominant strategy incentive compatible payment and allocation rules for

clearing these markets. We conclude with examples of how this framework can

construct prices for a variety of algorithmically constructed, semi-fungible

portfolios of practical importance.

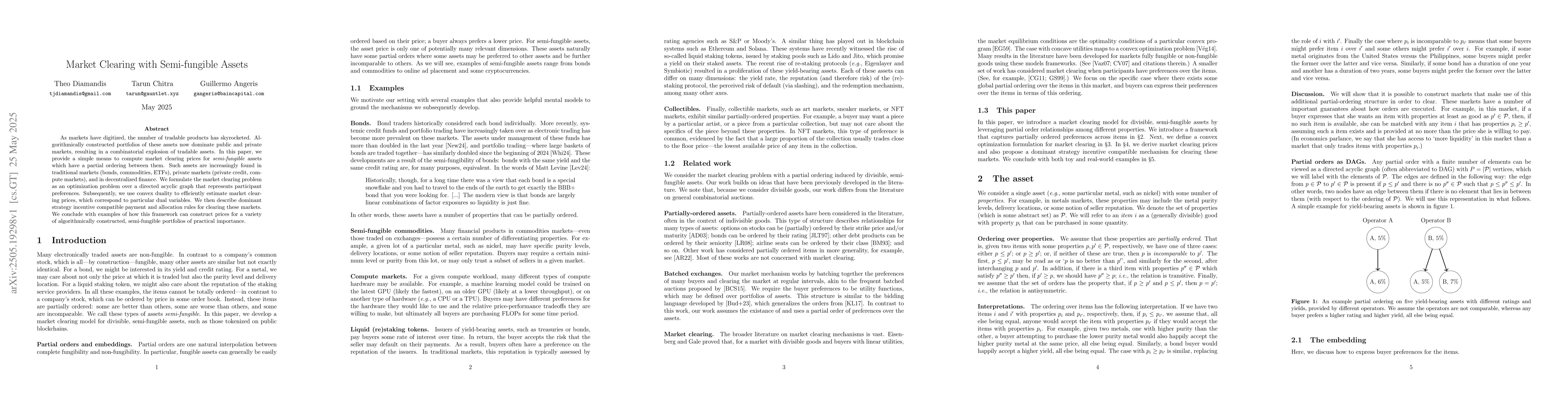

Discussion 0