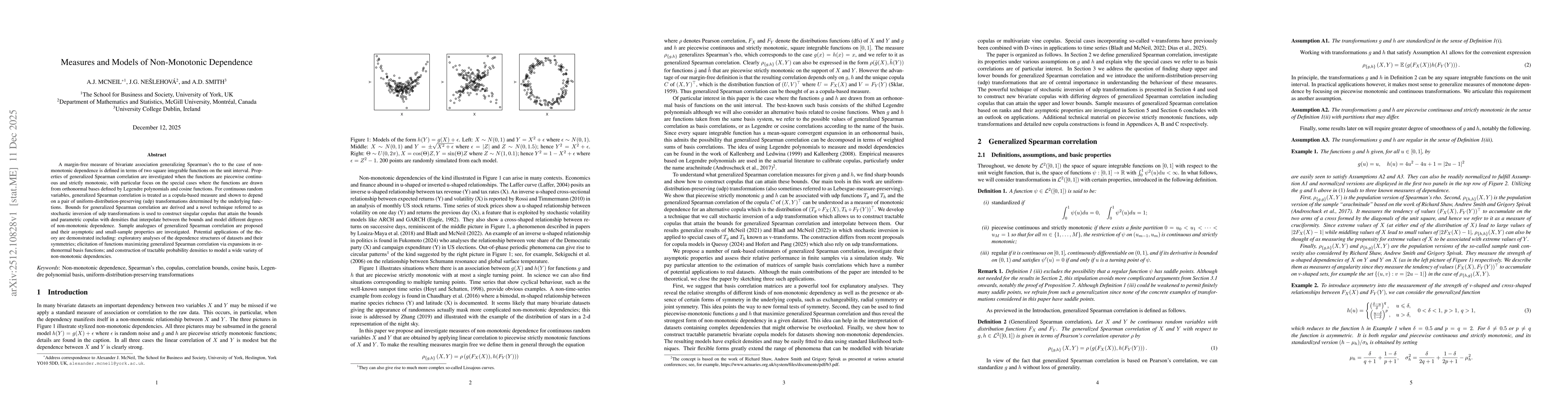

A margin-free measure of bivariate association generalizing Spearman's rho to the case of non-monotonic dependence is defined in terms of two square integrable functions on the unit interval. Properties of generalized Spearman correlation are investigated when the functions are piecewise continuous and strictly monotonic, with particular focus on the special cases where the functions are drawn from orthonormal bases defined by Legendre polynomials and cosine functions. For continuous random variables, generalized Spearman correlation is treated as a copula-based measure and shown to depend on a pair of uniform-distribution-preserving (udp) transformations determined by the underlying functions. Bounds for generalized Spearman correlation are derived and a novel technique referred to as stochastic inversion of udp transformations is used to construct singular copulas that attain the bounds and parametric copulas with densities that interpolate between the bounds and model different degrees of non-monotonic dependence. Sample analogues of generalized Spearman correlation are proposed and their asymptotic and small-sample properties are investigated. Potential applications of the theory are demonstrated including: exploratory analyses of the dependence structures of datasets and their symmetries; elicitation of functions maximizing generalized Spearman correlation via expansions in orthonormal basis functions; and construction of tractable probability densities to model a wide variety of non-monotonic dependencies.

Discussion 0